Photo AI

Last Updated Sep 13, 2025

Bank reconciliation Simplified Revision Notes for NSC Accounting

Revision notes with simplified explanations to understand Bank reconciliation quickly and effectively.

392+ students studying

Bank reconciliation

Bank Reconciliation is an internal control process that compares the business's bank account in the general ledger to the bank statement from the bank. Any differences between these two records must be investigated and corrected.

Purpose of Bank Reconciliation

- Ensures the cash balance reported in the ledger matches the actual balance at the bank.

- Identifies and resolves discrepancies caused by timing delays, errors, or unrecorded transactions.

- Provides greater control over cash, reducing the risk of fraud or mismanagement.

Common Reasons for Differences

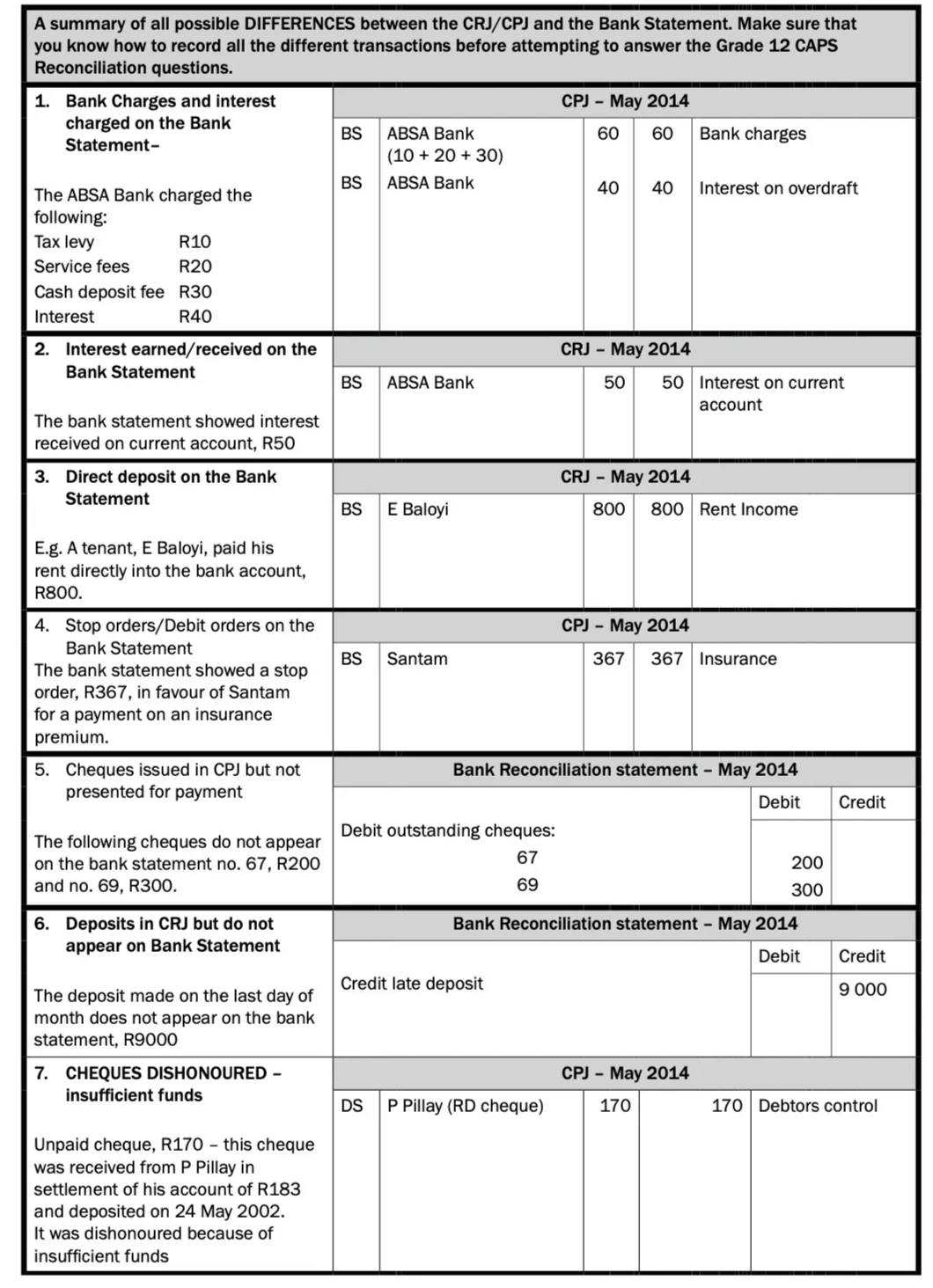

- Bank Charges & Interest: Fees or interest amounts may appear on the bank statement but aren't immediately recorded in the CRJ or CPJ.

- Direct Deposits: Funds paid directly into the bank account by third parties may not be recorded in the business's books yet.

- Stop Orders / Debit Orders: Automatic payments (e.g., insurance premiums) reduce the bank balance before the business records them.

- Cheques Not Yet Presented: The business has issued cheques that haven't been cashed or processed by the bank.

- Deposits Not Yet Credited: Deposits made late in the month may not show on the bank statement until the next period.

- Dishonoured Cheques: Cheques returned unpaid (e.g., insufficient funds) require reversal in the business's records.

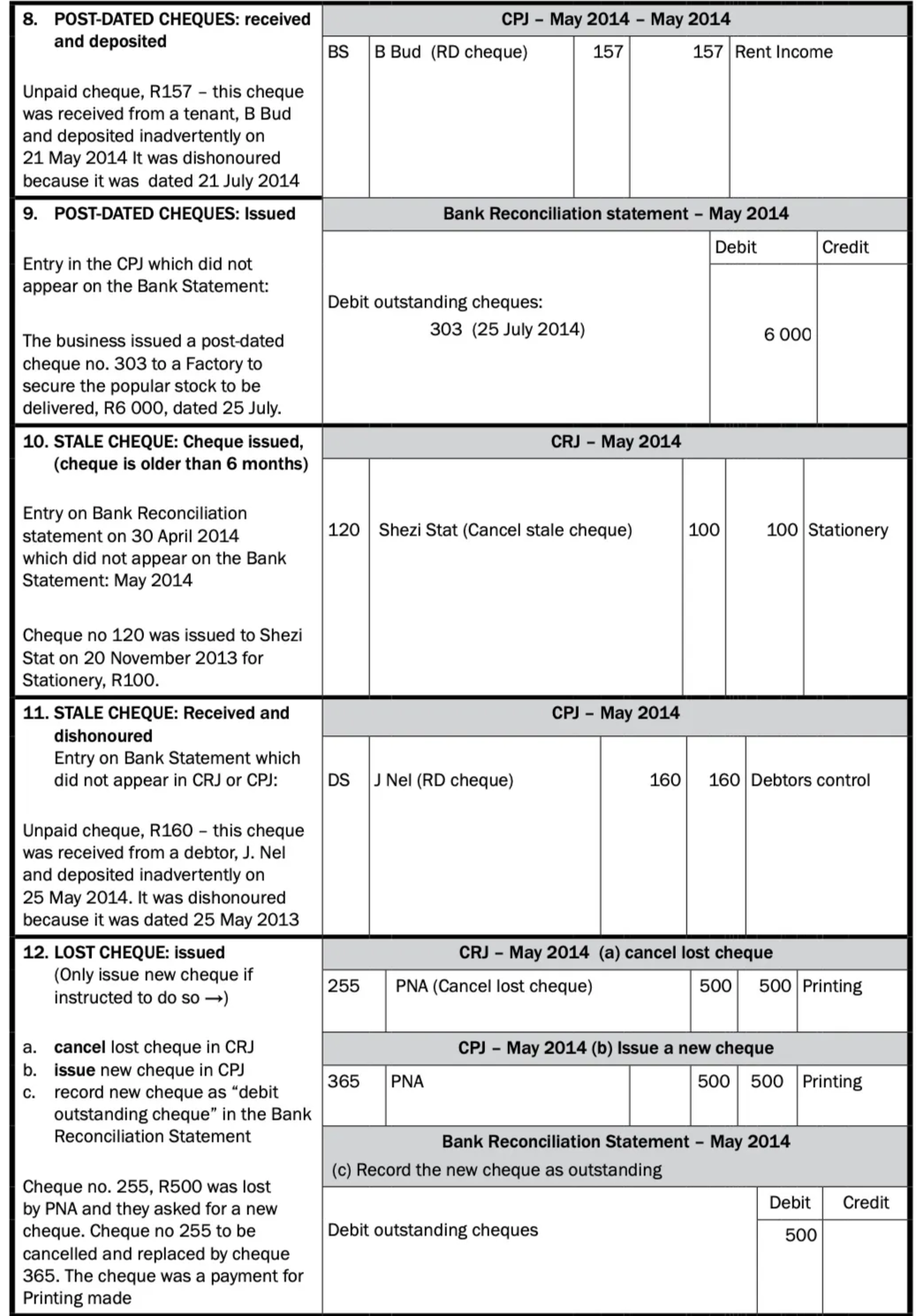

- Post-Dated / Stale Cheques:

- Post-Dated: Dated in the future, so the bank cannot process them before the specified date.

- Stale: Dated too long ago (older than 6 months), so the bank won't honour them.

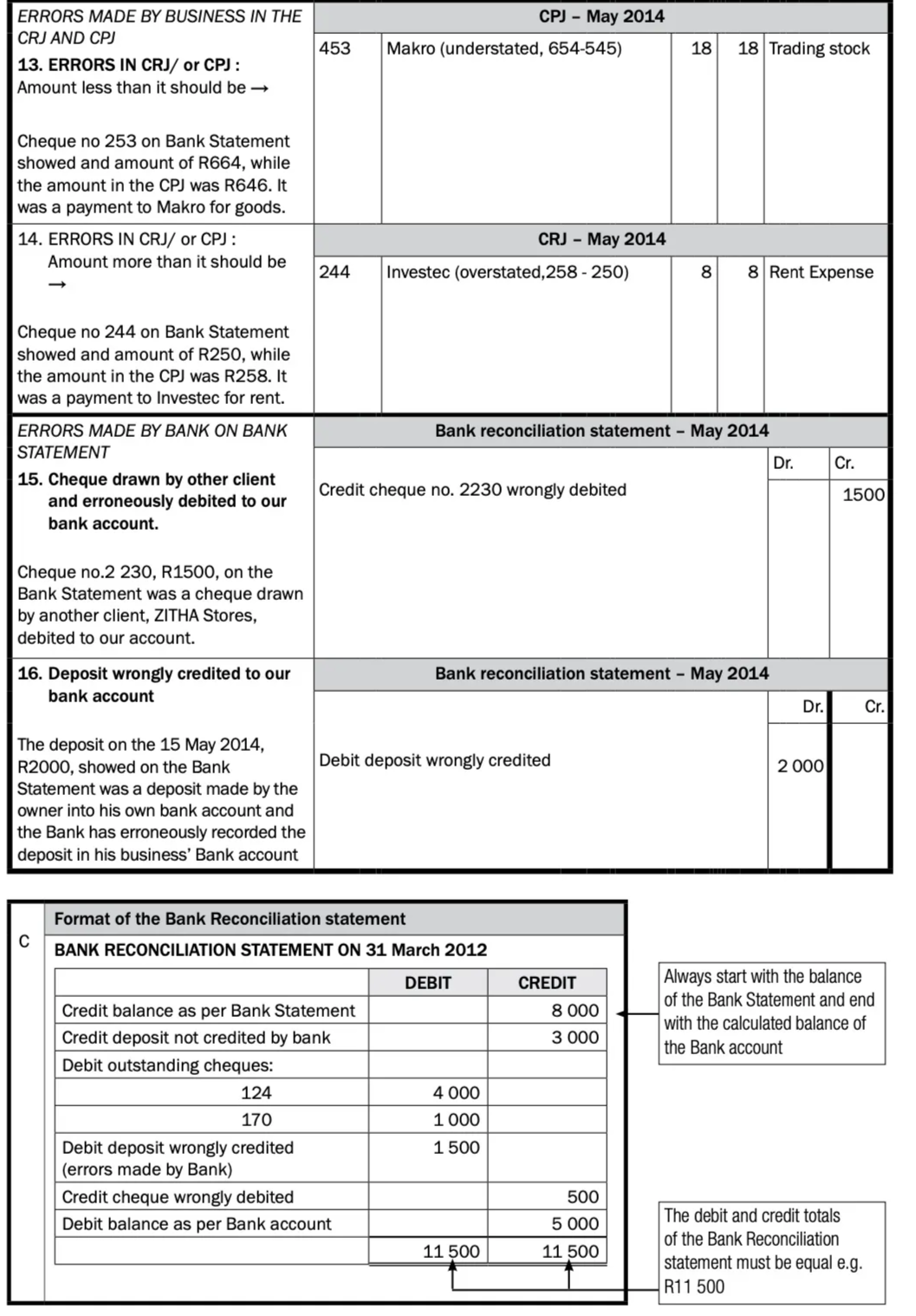

- Errors: Mistakes in either the CRJ/CPJ or the bank statement (e.g., amounts recorded incorrectly).

Steps to Reconcile

- Compare Opening Balances

- Match the bank statement opening balance with the business's ledger.

- Check All Transactions

- Verify deposits and withdrawals against CRJ (Cash Receipts Journal) and CPJ (Cash Payments Journal).

- Identify Unrecorded Items

- Adjust for bank charges, direct deposits, dishonoured cheques, etc.

- List Outstanding Cheques / Deposits

- Make a note of cheques not yet presented or deposits not credited.

- Update the Cash Book

- Record new or missing transactions discovered from the bank statement.

- Prepare Bank Reconciliation Statement

- Show the adjusted balance in the cash book, plus or minus any outstanding entries, to arrive at the correct bank balance.

Final Checks

- After all corrections are made, the ledger balance (cash book) should match the reconciled bank statement balance.

- Keep documentation of each discrepancy and its resolution to maintain an audit trail.

500K+ Students Use These Powerful Tools to Master Bank reconciliation For their NSC Exams.

Enhance your understanding with flashcards, quizzes, and exams—designed to help you grasp key concepts, reinforce learning, and master any topic with confidence!

30 flashcards

Flashcards on Bank reconciliation

Revise key concepts with interactive flashcards.

Try Accounting Flashcards5 quizzes

Quizzes on Bank reconciliation

Test your knowledge with fun and engaging quizzes.

Try Accounting Quizzes40 questions

Exam questions on Bank reconciliation

Boost your confidence with real exam questions.

Try Accounting Questions26 exams created

Exam Builder on Bank reconciliation

Create custom exams across topics for better practice!

Try Accounting exam builder68 papers

Past Papers on Bank reconciliation

Practice past papers to reinforce exam experience.

Try Accounting Past PapersOther Revision Notes related to Bank reconciliation you should explore

Discover More Revision Notes Related to Bank reconciliation to Deepen Your Understanding and Improve Your Mastery

Load more notes