Photo AI

Last Updated Sep 26, 2025

Monopolistic competition Simplified Revision Notes for A-Level Edexcel Economics A

Revision notes with simplified explanations to understand Monopolistic competition quickly and effectively.

419+ students studying

4.3 Monopolistic competition

DEFINITIONS:

Monopolistic Competition: Monopolistic competition is a market structure characterized by many firms selling similar but not identical products, leading to some degree of market power for each firm.

Explain:

4.3.1 The characteristics of monopolistic competition

Monopolistic competition is a market structure characterized by the following features:

- Large Number of Firms: There are many firms in the market, each with a relatively small market share, ensuring no single firm has significant market power.

- Product Differentiation: Firms sell products that are similar but not identical. Each firm offers a slightly different product, which can be based on quality, features, branding, or other attributes.

- Freedom of Entry and Exit: There are low barriers to entry and exit in the market, allowing firms to enter and leave the industry with relative ease. This ensures that profits in the long run are normal (zero economic profit).

- Independent Decision-Making: Each firm acts independently and makes its own pricing and output decisions, considering the potential reactions of competitors.

- Non-Price Competition: Firms compete on factors other than price, such as product quality, customer service, advertising, and other marketing efforts.

- Some Market Power: Due to product differentiation, each firm has some degree of market power, allowing them to influence the price of their own product to a certain extent.

- Downward Sloping Demand Curve: Each firm faces a downward sloping demand curve, meaning that they can increase sales by lowering prices, but to sell additional units, they must reduce the price.

Explain with the aid of a diagram

4.3.2 Explanation of Short Run Monopolistic Competition: Supernormal Profit/Loss

Monopolistic Competition:

- A market structure characterized by many firms selling differentiated products.

- Firms have some degree of market power due to product differentiation.

- There is freedom of entry and exit in the market.

Short Run Equilibrium:

In the short run, firms in monopolistic competition can earn supernormal (abnormal) profit or incur losses. The key elements to consider are the Average Total Cost (ATC), Marginal Cost (MC), and Marginal Revenue (MR).

Supernormal Profit:

- Occurs when total revenue (TR) exceeds total cost (TC).

- On the diagram, the price (P) set by the firm is above the average total cost (ATC) at the profit-maximizing output level.

Loss:

- Occurs when total cost (TC) exceeds total revenue (TR).

- On the diagram, the price (P) set by the firm is below the average total cost (ATC) at the profit-maximizing output level.

Diagram for Supernormal Profit:

- Demand Curve (D): Downward sloping, representing the price the firm can charge at each quantity.

- Marginal Revenue Curve (MR): Downward sloping and below the demand curve due to the law of diminishing marginal returns.

- Marginal Cost Curve (MC): Upward sloping.

- Average Total Cost Curve (ATC): U-shaped.

Supernormal Profit Diagram:

Explanation:

- Profit Maximizing Output (Q): Where MR = MC.

- Price (P): Determined from the demand curve at quantity Q*.

- ATC at Q: The ATC is below the price P at Q*, indicating supernormal profit.

- Supernormal Profit Area: The area between price P and ATC, up to the quantity Q*.

Diagram for Loss:

Explanation:

- Profit Maximizing Output (Q): Where MR = MC.

- Price (P): Determined from the demand curve at quantity Q*.

- ATC at Q: The ATC is above the price P at Q*, indicating a loss.

- Loss Area: The area between ATC and price P, up to the quantity Q*.

Conclusion:

In the short run, firms in monopolistic competition can earn supernormal profits if the price exceeds ATC at the profit-maximizing output level or incur losses if the price is below ATC. These outcomes are temporary as the market adjusts in the long run, leading to normal profits due to the entry and exit of firms.

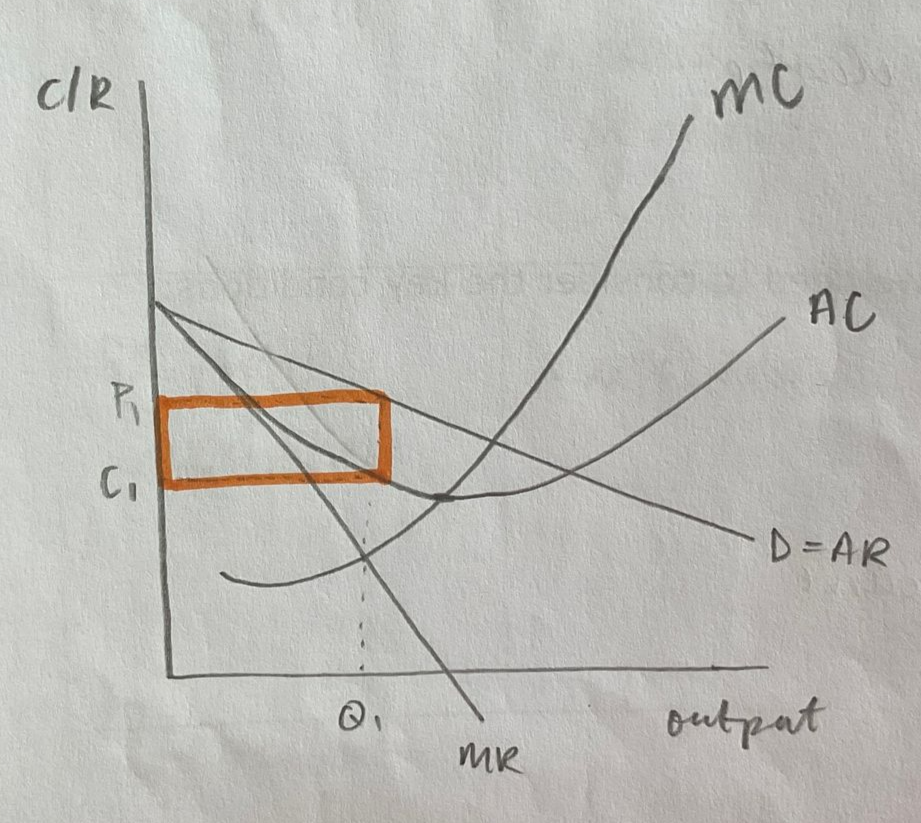

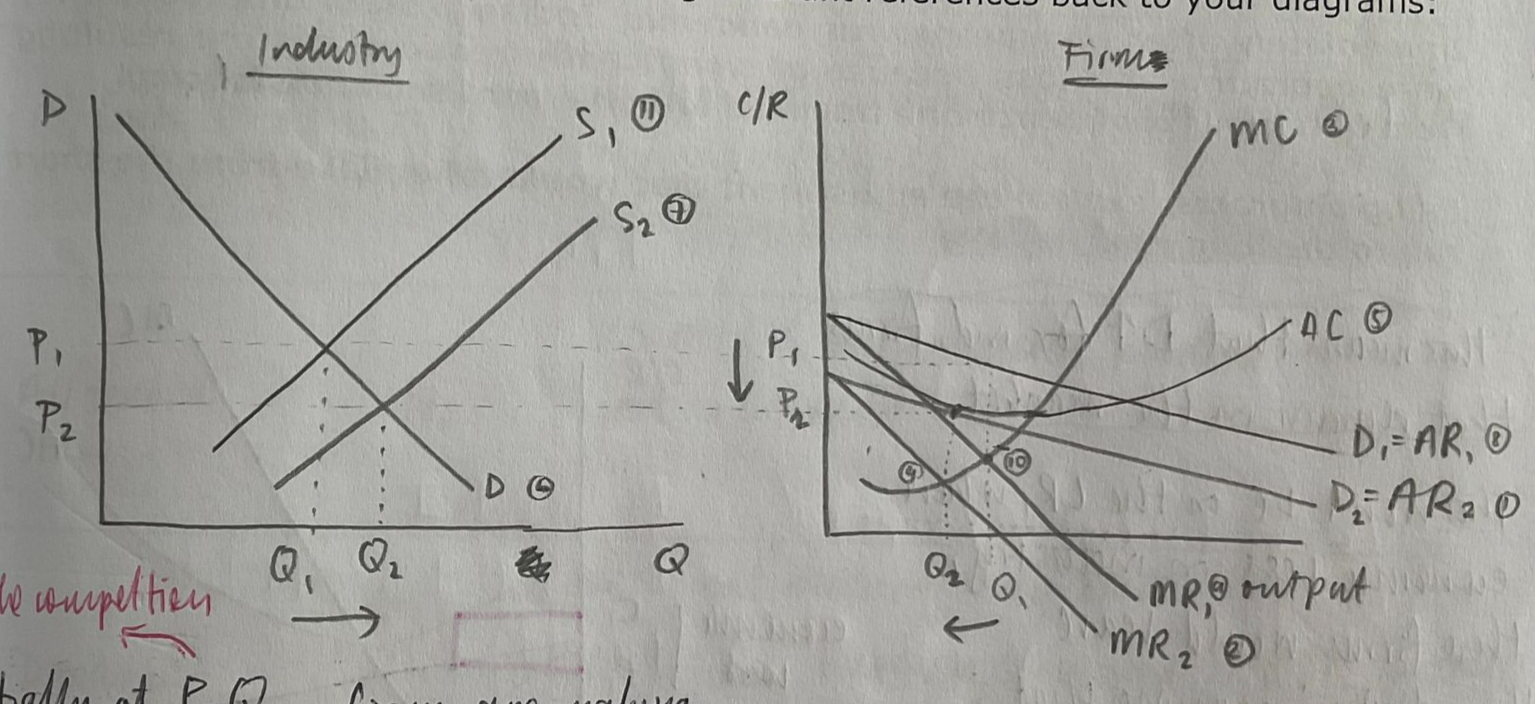

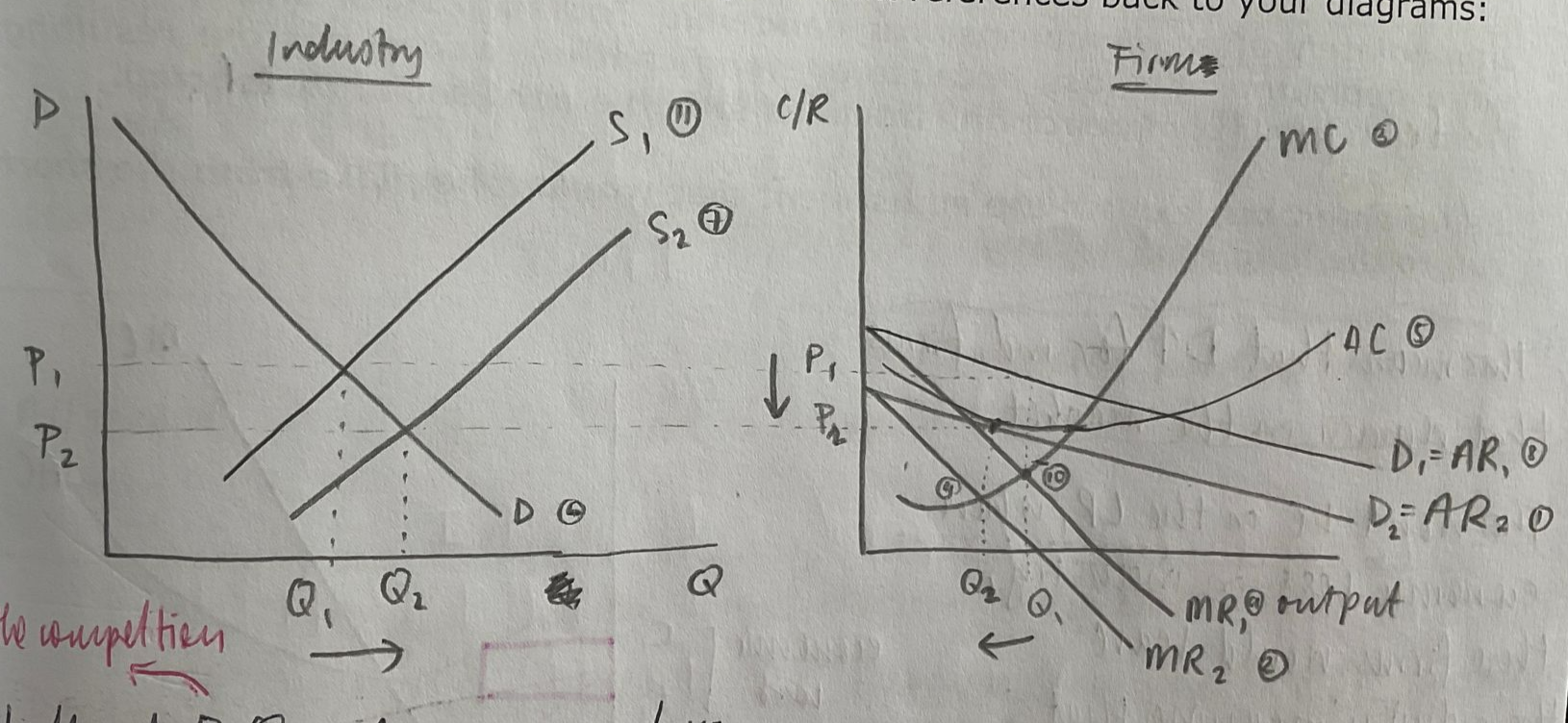

4.3.3 Explanation of Long Run Monopolistic Competition and Normal Profits

In the long run, firms in a monopolistically competitive market will earn normal profits due to the entry and exit of firms. Monopolistic competition is characterized by many firms, differentiated products, and free entry and exit in the market. In the long run, any economic profits made by firms will attract new entrants, increasing the competition and reducing the demand for each individual firm's product until only normal profits are made.

Key Features:

- Many Firms: Numerous firms in the market.

- Product Differentiation: Each firm sells a slightly different product.

- Free Entry and Exit: Firms can enter or leave the market easily.

Long Run Equilibrium:

In the long run, firms will produce at a point where:

- Price (P) equals Average Cost (AC): Firms earn normal profits (zero economic profit).

- Marginal Cost (MC) equals Marginal Revenue (MR): Profit maximization condition.

- Demand Curve (AR) is Tangent to AC Curve: The firm's demand curve (AR) is tangent to its average cost curve at the profit-maximizing output level.

Diagram:

Below is a diagram illustrating long-run equilibrium in monopolistic competition:

Explanation of the Diagram:

- Demand Curve (AR): The downward-sloping average revenue (demand) curve represents the demand for the firm's product.

- Marginal Cost Curve (MC): The upward-sloping marginal cost curve represents the cost of producing an additional unit of output.

- Average Cost Curve (AC): The U-shaped average cost curve represents the average cost per unit of output.

- Equilibrium Point (Q*): The point where the firm's marginal cost (MC) equals marginal revenue (MR), which is also where the demand curve (AR) is tangent to the average cost curve (AC). At this point, the firm is making normal profits since price (P) equals average cost (AC).

In the long run, firms in monopolistic competition adjust their production and pricing until they reach a point where they earn normal profits, with no incentive for new firms to enter or existing firms to exit the market. This leads to an equilibrium where each firm produces at a level where its average cost is minimized and equal to the price consumers are willing to pay.

4.3.4 Equilibrium Price and Output for a Firm in Monopolistic Competition

Monopolistic Competition: Monopolistic competition is a market structure characterized by many firms selling differentiated products. Each firm has some degree of market power, allowing them to set prices above marginal cost. However, the presence of close substitutes means that the demand curve for each firm is relatively elastic.

Explanation:

In monopolistic competition, firms maximize profit by producing at the quantity where marginal cost (MC) equals marginal revenue (MR). The price is then determined by the demand curve at that quantity.

- Demand Curve (D): Downward-sloping, indicating that higher prices lead to lower quantities demanded.

- Marginal Revenue Curve (MR): Downward-sloping and lies below the demand curve because the firm must lower its price to sell additional units.

- Marginal Cost Curve (MC): Typically upward-sloping due to increasing marginal costs.

- Average Total Cost Curve (ATC): U-shaped, reflecting economies and diseconomies of scale.

Diagram:

Below is a diagram illustrating equilibrium price and output for a firm in monopolistic competition:

Key Points in the Diagram:

- Demand Curve (D or AR): Shows the relationship between price and quantity demanded.

- Marginal Revenue Curve (MR): Lies below the demand curve due to the downward-sloping nature of the demand curve.

- Marginal Cost Curve (MC): Intersects the MR curve to determine the profit-maximizing output (Q*).

- Average Total Cost Curve (ATC): U-shaped curve; at Q*, ATC intersects the demand curve to determine the price (P*).

Equilibrium Conditions:

- Profit Maximization: The firm maximizes profit where MR = MC. At this quantity (Q*), the firm produces the level of output where its marginal revenue equals its marginal cost.

- _Equilibrium Price (P):_Once the equilibrium quantity is determined, the price is found by projecting Q* up to the demand curve. This gives the equilibrium price P*.

- Normal Profit: In the long run, firms in monopolistic competition will earn only normal profits due to the entry and exit of firms. This means that in the long run, P = ATC at the equilibrium quantity.

Conclusion:

In monopolistic competition, the equilibrium price and output are determined by the intersection of the MR and MC curves for a firm, with the price set according to the demand curve. This results in firms earning normal profit in the long run, as new entrants drive profits down to a normal level.

500K+ Students Use These Powerful Tools to Master Monopolistic competition For their A-Level Exams.

Enhance your understanding with flashcards, quizzes, and exams—designed to help you grasp key concepts, reinforce learning, and master any topic with confidence!

50 flashcards

Flashcards on Monopolistic competition

Revise key concepts with interactive flashcards.

Try Economics A Flashcards5 quizzes

Quizzes on Monopolistic competition

Test your knowledge with fun and engaging quizzes.

Try Economics A Quizzes29 questions

Exam questions on Monopolistic competition

Boost your confidence with real exam questions.

Try Economics A Questions27 exams created

Exam Builder on Monopolistic competition

Create custom exams across topics for better practice!

Try Economics A exam builder21 papers

Past Papers on Monopolistic competition

Practice past papers to reinforce exam experience.

Try Economics A Past PapersOther Revision Notes related to Monopolistic competition you should explore

Discover More Revision Notes Related to Monopolistic competition to Deepen Your Understanding and Improve Your Mastery