Photo AI

Marginal Costing Agnew Ltd manufactures a single product - Leaving Cert Accounting - Question 8 - 2010

Question 8

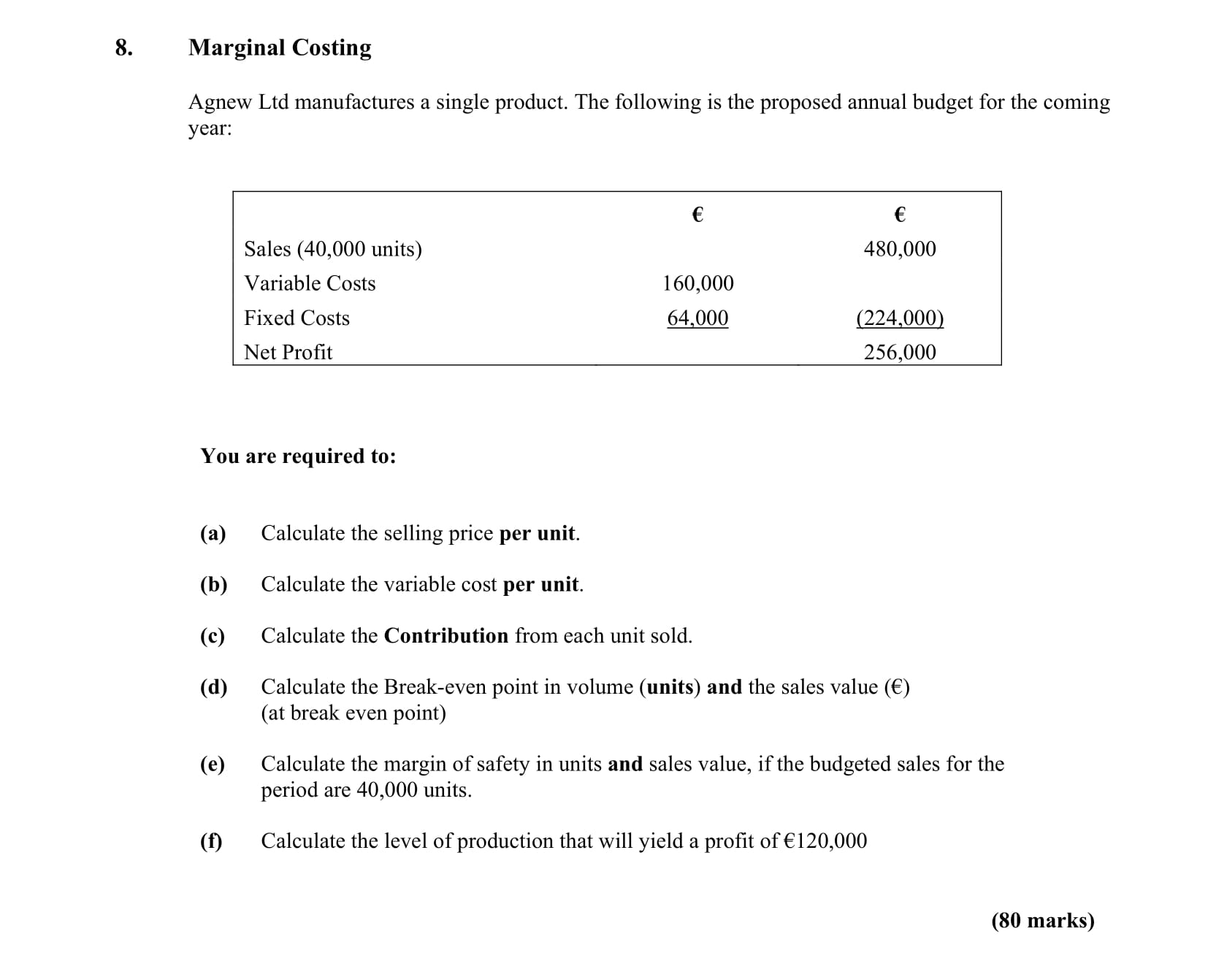

Marginal Costing Agnew Ltd manufactures a single product. The following is the proposed annual budget for the coming year: Sales (40,000 units) ... show full transcript

Worked Solution & Example Answer:Marginal Costing Agnew Ltd manufactures a single product - Leaving Cert Accounting - Question 8 - 2010

Step 1

Step 2

Step 3

Step 4

Step 5

Step 6