Banking, Interest, and Taxation (Grade 11 NSC Matric Mathematical Literacy): Revision Notes

Interest

Understanding interest types

When you put money in a bank account or make an investment, the money grows over time through interest. There are two main ways that interest can be calculated: simple interest and compound interest. Understanding the difference between these two methods is crucial for making smart financial decisions.

The type of interest calculation method used can dramatically affect how much your money grows over time. This knowledge is essential for making informed financial decisions about savings, investments, and loans.

Simple interest

Simple interest is always calculated using the original amount of money you invested (called the principal). This means that no matter how long your money stays invested, the interest calculation always uses the same starting amount.

Key characteristics of simple interest:

- The interest amount added each period stays exactly the same

- Interest is calculated only on the original principal amount

- Creates a steady, predictable growth pattern

- Results in linear growth when shown on a graph

How simple interest works

When you invest money using simple interest, the same amount of interest gets added to your account each time period. For example, if you invest R500 at 10% simple interest per year, you will earn R50 interest every single year, regardless of how much money has accumulated in your account.

Simple interest is like receiving the same bonus amount every year - it never changes based on how much you've already earned.

Compound interest

Compound interest works differently because it is calculated on a changing value. This value includes your original investment plus any interest that has already been earned and added to your account.

Key characteristics of compound interest:

- The interest amount changes (increases) each period

- Interest is calculated on the growing total balance

- Creates accelerating growth over time

- Results in exponential growth when shown on a graph

How compound interest works

With compound interest, each time interest is calculated, it gets added to your account balance. The next time interest is calculated, it's based on this new, larger amount. This means your money grows faster and faster over time.

Worked example: comparing both methods

Worked Example: Comparing Simple vs Compound Interest

Let's compare what happens when R500 grows at 10% interest for 3 years:

Simple interest calculation:

- Year 1: Interest = 10% × R500 = R50

- Year 2: Interest = 10% × R500 = R50

- Year 3: Interest = 10% × R500 = R50

- Total after 3 years: R500 + R150 = R650

Compound interest calculation:

- Year 1: Money = R500 + (10% × R500) = R550

- Year 2: Money = R550 + (10% × R550) = R605

- Year 3: Money = R605 + (10% × R605) = R665.50

- Total after 3 years: R665.50

Notice how compound interest gives you an extra R15.50 over the same period!

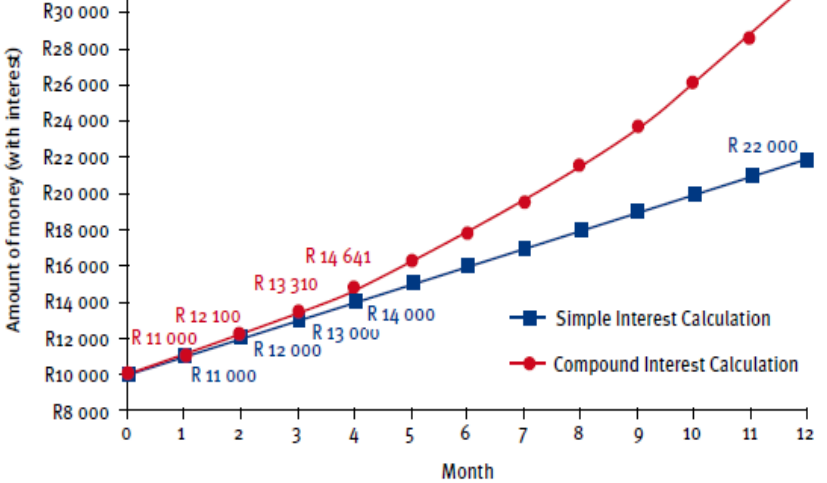

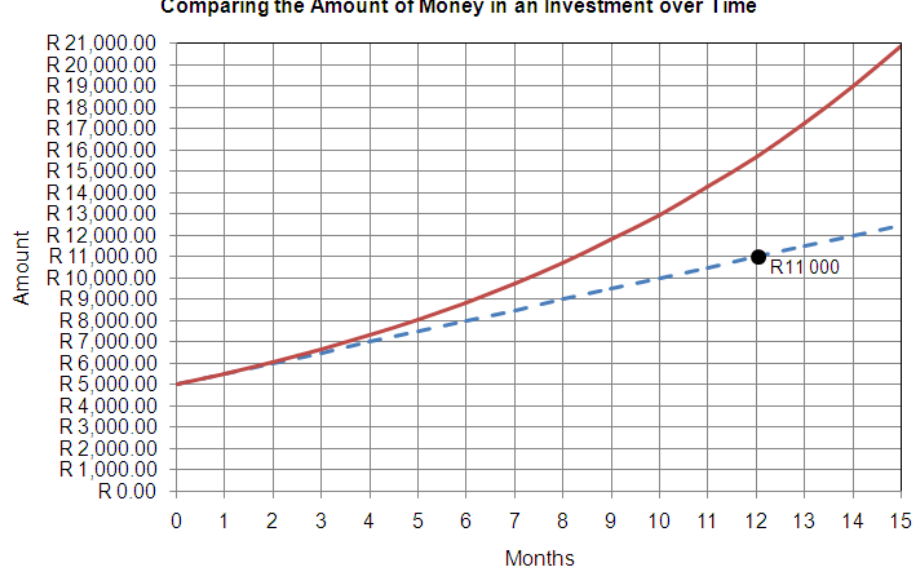

Graphical representation

When you plot simple interest and compound interest on a graph, you can clearly see the difference:

Visual Patterns on Graphs:

- Simple interest creates a straight line because the same amount is added each period

- Compound interest creates a curved line that gets steeper over time because the interest amounts keep increasing

The longer the investment period, the bigger the difference becomes between simple and compound interest. This is why understanding compound interest is so important for long-term financial planning.

The compound interest formula

For compound interest calculations, you can use this formula:

Where:

- A = final amount of money in the account

- P = initial amount invested (principal)

- i = interest rate per period (as a decimal)

- n = number of times interest is calculated

Worked Example: Using the Compound Interest Formula

If you invest R3,500 at 7.5% per year, compounded monthly for 2 years:

- P = R3,500

- i = 7.5% ÷ 12 = 0.625% per month = 0.00625

- n = 2 years × 12 months = 24 times

Why banks prefer compound interest

Banks and financial institutions almost always use compound interest rather than simple interest. This is because compound interest generates significantly more money over time, especially for longer investment periods. From the bank's perspective, this means higher profits when they lend money or invest funds.

Critical for Borrowers and Savers:

- For borrowers: loans with compound interest become more expensive over time

- For savers and investors: money can grow much faster with compound interest accounts

Exam tips

Exam Success Strategies:

- Graph identification: Simple interest = straight line, Compound interest = curved line

- Always check whether you're asked to calculate with or without using formulas

- Remember that compound interest calculations get more complex each period because you're working with changing amounts

- Time matters: The longer the period, the bigger the advantage of compound interest becomes

- Monthly rates: When interest is compounded monthly, divide the annual rate by 12

Key Points to Remember:

- Simple interest is calculated on the original amount only and creates steady, linear growth

- Compound interest is calculated on the growing balance and creates accelerating, exponential growth

- Compound interest always grows faster than simple interest over the same time period

- The difference becomes dramatic over longer time periods

- Banks prefer compound interest because it generates more profit for them