Banking (Grade 11 NSC Matric Mathematical Literacy): Revision Notes

Banking

Banking is a fundamental part of managing your money and making financial decisions. Understanding how banks work, how they calculate interest, and how they charge fees will help you make better choices about your finances. This section covers the essential banking concepts you need to know for your NSC Mathematical Literacy exam.

Types of bank accounts and interest calculation

Banks offer different types of accounts for different purposes. The two main types you need to understand are transactional accounts and fixed deposit accounts. Each type calculates interest differently based on how the account is used.

Transactional accounts

A transactional account is designed for everyday banking activities. You use this type of account to make regular deposits, withdrawals, and payments. The key feature of transactional accounts is that your account balance changes frequently throughout the month as you conduct various transactions.

Because your balance changes regularly, banks calculate interest differently for these accounts. Interest is calculated at the end of every day based on the balance in your account on that specific day. This daily calculation ensures that you earn interest on whatever money you have in your account, even if the amount changes from day to day.

For example, if you have R1000 on Monday, R1500 on Tuesday (after a deposit), and R800 on Wednesday (after a withdrawal), the bank calculates interest separately for each day based on the actual balance on that day.

Fixed deposit accounts

A fixed deposit account is an investment account where you deposit money and leave it to grow with interest over a specific period. The main characteristic of this account type is that the balance remains stable throughout the month because you don't make regular transactions.

Since the balance doesn't change during the month, banks use a simpler interest calculation method. Interest is calculated on the balance at the beginning of the month, multiplied by the number of days in that month. This gives you the total monthly interest, which is then added to your account at the end of the month.

This method works because there's no need to track daily balance changes - the amount stays the same throughout the investment period.

Hire purchase and loan agreements

When you need to buy something expensive or need money for a specific purpose, you have two main options: hire purchase agreements or loan agreements. Both involve borrowing money and paying it back with interest, but they work in different ways.

Key terminology

Before comparing these two options, you need to understand the important terms:

- Buying on credit: Purchasing an item through monthly payments instead of paying the full amount upfront

- Deposit: A percentage of the purchase price or loan amount that you pay upfront as a "promise" to complete the payments

- Monthly payment or monthly repayment: The regular amount you pay each month until the debt is fully paid

- Interest: The extra cost of borrowing money, calculated as the difference between what you borrowed and what you pay back

- Total cost: The complete amount you will pay, including the deposit, all monthly payments, and any fees

- Length or life of the agreement: The time period over which you will make payments

Hire purchase agreements

With a hire purchase agreement, you are buying a specific item (like a car, furniture, or appliance) and paying for it through monthly payments rather than paying the full amount immediately. This is sometimes called "buying on credit" or making a "credit purchase."

The important thing to remember is that you are purchasing an actual item. You typically need to pay a deposit upfront, then make monthly payments until the item is fully paid off. The final amount you pay will always be higher than the original purchase price because of interest charges.

Loan agreements

With a loan agreement, you are borrowing a specific amount of money from the bank or lender. You then use this money for whatever purpose you need (which could include buying an item). You repay the borrowed amount plus interest through monthly payments.

The key difference is that you're borrowing money, not buying a specific item. The final amount you pay back will always be higher than the original loan amount because of interest charges.

Important concepts

The deposit applies to both hire purchase and loan agreements. It represents your commitment to the agreement and reduces the amount you need to finance.

The total cost includes everything you pay: the deposit, all monthly payments, and any administration or service fees. This gives you the true cost of your purchase or loan.

The interest is calculated as the difference between the total amount you pay and the original price (for hire purchase) or original loan amount (for loans).

Bank fee structures and charges

Banks charge fees for various services and transactions. Understanding these fee structures helps you choose the most cost-effective banking options and avoid unnecessary charges. There are three common fee structures that banks use.

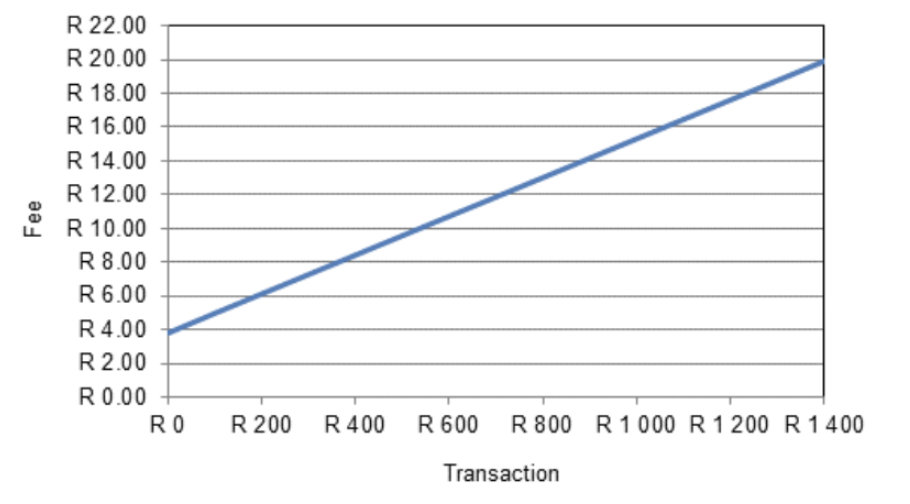

Structure 1: Fixed cost plus percentage

This structure combines a fixed fee with a percentage-based fee. You pay a set amount (the fixed cost) plus an additional amount calculated as a percentage of your transaction value.

Formula:

Example: Structure 1 Calculation

Formula: Fee = R3,90 + 1,15% of deposit value

For a R500,00 deposit:

- Calculation: Fee = R3,90 + (1,15% × R500,00)

- Fee = R3,90 + (0,0115 × R500,00)

- Fee = R3,90 + R5,75 = R9,65

This structure means you always pay the base fee, and larger transactions cost proportionally more.

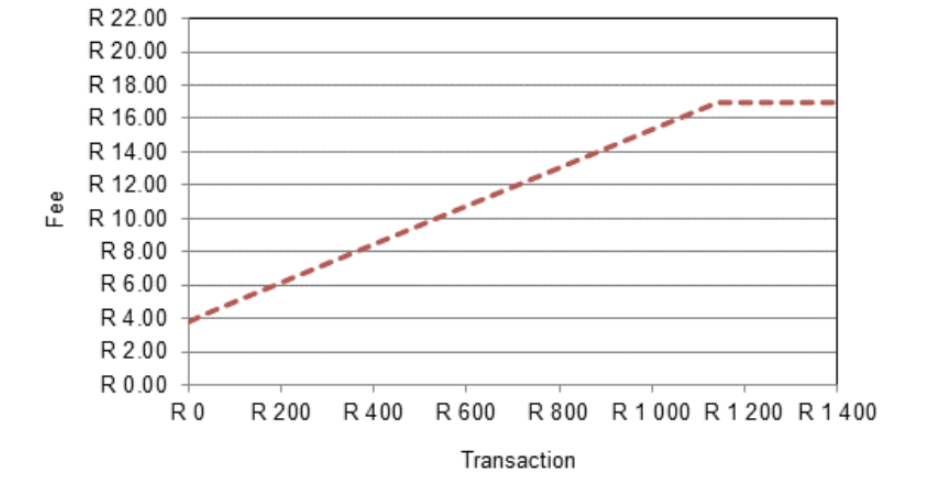

Structure 2: Capped percentage structure

This structure works like Structure 1 but includes a maximum fee limit. You pay the fixed amount plus a percentage, but if the calculated fee exceeds the maximum, you only pay the maximum amount.

Formula: , but never more than the maximum fee

Example: Structure 2 with Fee Cap

Formula: Fee = R3,75 + 0,75% of transaction value (maximum fee R17,00)

Small transaction (R500,00):

- Calculation: Fee = R3,75 + (0,75% × R500,00)

- Fee = R3,75 + R3,75 = R7,50

- Since R7,50 < R17,00, you pay R7,50

Large transaction (R20 000,00):

- Calculation: Fee = R3,75 + (0,75% × R20 000,00)

- Fee = R3,75 + R150,00 = R153,75

- Since R153,75 > R17,00, you pay the maximum of R17,00

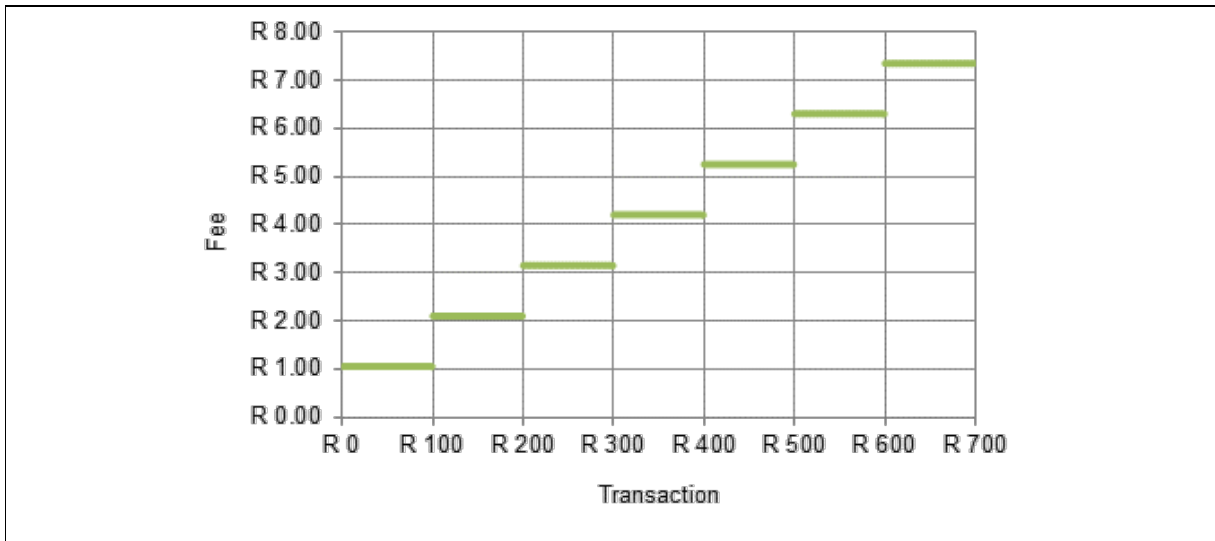

Structure 3: Variable fee per R100

This structure charges a set fee for every R100,00 (or part thereof) of the transaction value. This creates a step function where the fee increases in jumps rather than smoothly.

Formula:

Example: Structure 3 Step Calculation

Formula: Fee = R1,05 per R100,00

For a R2 350,00 deposit:

- Number of R100,00 portions = R2 350,00 ÷ R100,00 = 23,5

- Since we count partial portions as full portions, we use 24

- Fee = 24 × R1,05 = R25,20

Comparing fee structures

Different fee structures are better for different transaction sizes:

- Structure 1 increases steadily with transaction size

- Structure 2 is the same as Structure 1 for small transactions but becomes more affordable for large transactions due to the cap

- Structure 3 creates a stepped pattern and can be cost-effective for certain transaction ranges

When choosing a bank account, consider which fee structure works best for your typical transaction patterns.

Worked examples

Worked Example: Interest Calculation Comparison

Transactional account: If you have R1 000 on day 1, deposit R500 on day 10, and withdraw R300 on day 20 in a 30-day month, the bank calculates interest daily:

- Days 1-9: Interest on R1 000

- Days 10-19: Interest on R1 500

- Days 20-30: Interest on R1 200

Fixed deposit account: If you invest R1 000 for a 30-day month at the same interest rate, the bank calculates: Interest = R1 000 × interest rate × 30 days

Worked Example: Fee Structure Comparison

For a R800,00 transaction:

Structure 1:

Structure 2: (under the R17,00 cap)

Structure 3: R800 ÷ R100 = 8 portions, so

In this case, Structure 3 is the cheapest option.

Worked Example: Hire Purchase vs Loan

Hire purchase: You want to buy a R10 000 couch. You pay a 10% deposit (R1 000) and finance R9 000 over 24 months at R450 per month.

- Total cost = R1 000 + (24 × R450) = R1 000 + R10 800 = R11 800

- Interest = R11 800 - R10 000 = R1 800

Loan: You borrow R9 000 to buy the same couch, paying R450 per month for 24 months.

- Total repayment = 24 × R450 = R10 800

- Interest = R10 800 - R9 000 = R1 800

- Total cost = R1 000 (cash for deposit) + R10 800 = R11 800

Both options cost the same in this example, but the structures are different.

Key Points to Remember:

- Transactional accounts calculate interest daily because balances change frequently, while fixed deposit accounts calculate interest monthly on stable balances

- Hire purchase means buying a specific item on credit, while a loan means borrowing money that you can use for any purpose

- The total cost of any credit agreement includes the deposit, all payments, and fees - always calculate this to understand the true cost

- Different bank fee structures favour different transaction sizes - Structure 1 increases steadily, Structure 2 has a cap for large transactions, and Structure 3 uses steps

- Always compare the total costs when choosing between different banking options or credit agreements