Bank Statements (Grade 12 NSC Matric Mathematical Literacy): Revision Notes

Bank Statements

What is a bank statement?

A bank statement is a document that banks send to account holders, usually monthly. It provides a complete record of all financial activity in your account during a specific period. Bank statements are essential tools for tracking your money and managing your finances effectively.

Bank statements serve as official records of your financial transactions and are often required for loan applications, budgeting, and tax purposes.

Key information shown on bank statements

Every bank statement contains four main pieces of information for each transaction:

- The date when the transaction occurred

- A description of what the transaction was for (salary, rent, groceries, etc.)

- The amount of money involved, shown as either a debit or credit

- The balance remaining in your account after each transaction

Essential bank statement terms

Understanding the terminology used in bank statements is crucial for effective financial management. Here are the key terms you'll encounter:

Account holder: The person whose name the account is registered under. This is the legal owner of the account.

Opening balance: The amount of money in your account at the start of the statement period.

Closing balance: The amount of money remaining in your account at the end of the statement period.

Transaction: Any movement of money into or out of your account. This includes deposits, withdrawals, payments, and purchases.

Debit transaction: Money that leaves your account. This reduces your balance and includes payments for bills, purchases, and cash withdrawals.

Credit transaction: Money that enters your account. This increases your balance and includes salary deposits, interest payments, and money transfers received.

The terms "debit" and "credit" can be confusing at first, but remember: from your perspective as the account holder, credits are good (money coming in) and debits reduce your balance (money going out).

Understanding debits and credits

The key to reading bank statements successfully is understanding the difference between debits and credits:

Critical Concept: Debits vs Credits

- Credits appear as positive amounts and increase your account balance

- Debits appear as negative amounts or in a separate column and decrease your account balance

- Your running balance changes after each transaction, showing exactly how much money you have at any point

How to read a bank statement step by step

Follow these systematic steps to read any bank statement accurately:

- Start with the opening balance - this shows how much money was in your account at the beginning

- Follow each transaction chronologically - they are listed in date order

- Check if each transaction is a debit or credit - look at which column the amount appears in

- Track the running balance - this updates after each transaction

- Verify the closing balance - this should match your final amount

Worked example analysis

Let's examine how to interpret a real bank statement to understand the flow of transactions and balance changes.

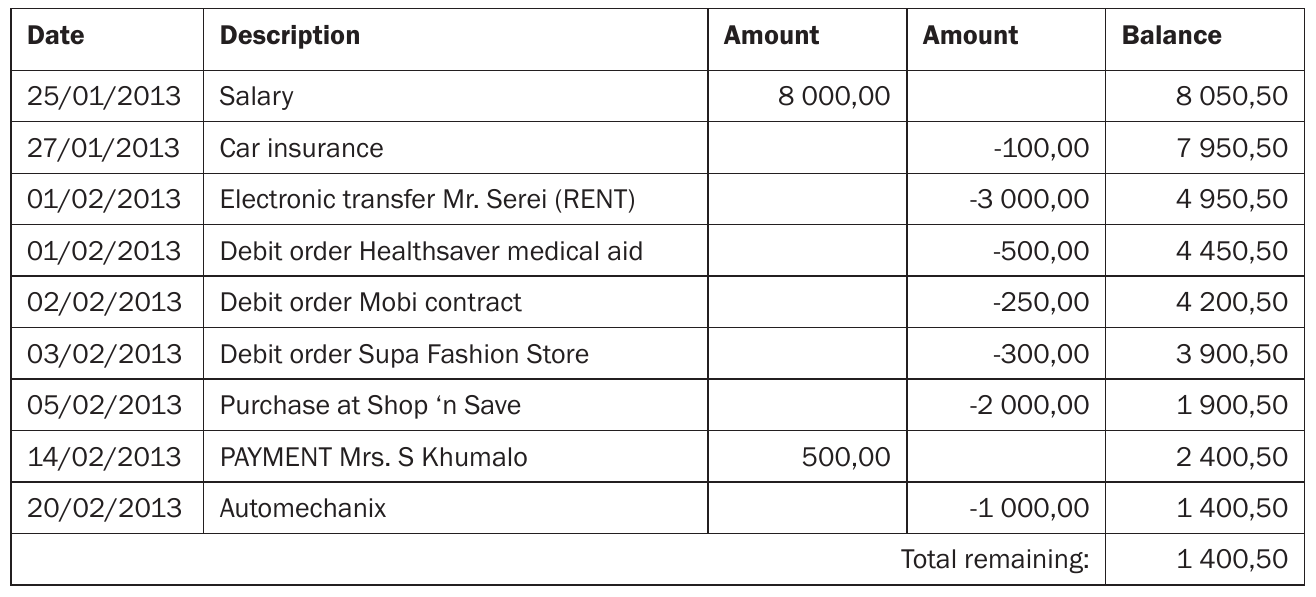

Worked Example: Analysing Monthly Bank Statement

In the example above, we can see:

- The account started with a balance of R8,050.50 on 25/01/2013

- A salary of R8,000.00 was deposited (credit transaction)

- Various expenses were paid throughout the month (debit transactions):

- Car insurance: R100.00

- Rent payment: R3,000.00

- Medical aid: R500.00

- Mobile contract: R250.00

- Fashion store purchase: R300.00

- Shop purchase: R2,000.00

- Car repairs: R1,000.00

- One additional deposit of R500.00 was received

- The final balance was R1,400.50

Calculating account balances

To find any balance during the month, you can use this fundamental formula:

Worked Example: Balance Calculation

For example, after the salary was paid:

- Previous balance: R8,050.50

- Credit (salary): R8,000.00

- New balance: R8,050.50 + R8,000.00 = R16,050.50

Common exam tips for bank statements

When working with bank statements in examinations or real-life situations, these strategies will help ensure accuracy:

Essential Exam Tips:

- Always check your arithmetic - make sure debits reduce the balance and credits increase it

- Look carefully at the column headings - payments and deposits are usually in separate columns

- Remember the running balance - it should update correctly after each transaction

- Pay attention to dates - transactions are processed in chronological order

- Distinguish between different types of transactions - ATM withdrawals, debit card purchases, salary deposits, and interest payments are all different

Typical bank statement transactions you might see

Understanding common transaction types helps you interpret bank statements more effectively:

Credit transactions (money coming in):

- Salary or wage payments

- Interest earned on your balance

- Money transfers from other people

- Deposits made at ATMs or branches

Debit transactions (money going out):

- ATM cash withdrawals

- Debit card purchases at shops

- Automatic debit orders (insurance, cell phone contracts)

- Electronic transfers for rent or other payments

- Bank fees and charges

Most people have more debit transactions than credit transactions, which is why monitoring your spending through bank statements is so important for budgeting.

Key Points to Remember:

- Bank statements track all money movements in your account over a monthly period

- Credits increase your balance (money coming in), debits decrease your balance (money going out)

- The running balance shows exactly how much money you have after each transaction

- Always verify that the mathematics is correct when reading bank statements

- Understanding bank statements is essential for managing your personal finances effectively