Medicare (VCE SSCE Health and Human Development): Revision Notes

Medicare

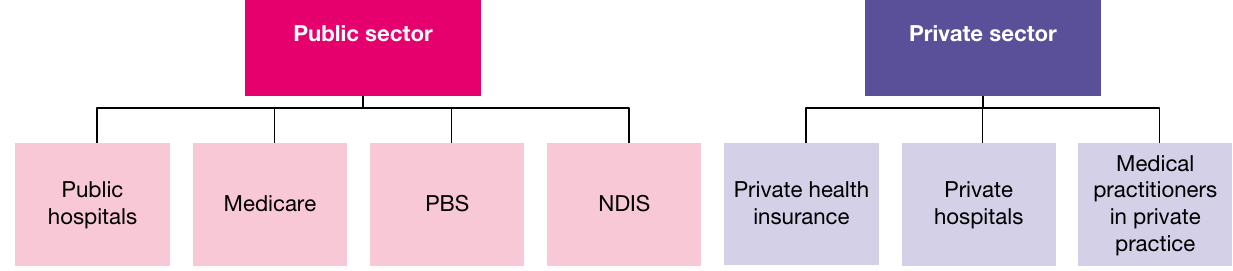

Understanding Australia's health system

According to the World Health Organization, a health system includes all activities designed to promote, restore, or maintain health. Australia's health system has two main parts: the public sector and the private sector.

The public sector includes services funded and provided by Australian governments (federal, state, territory, and local). This includes:

- Public hospitals

- Medicare

- Pharmaceutical Benefits Scheme (PBS)

- National Disability Insurance Scheme (NDIS)

The private sector includes:

- Private health insurance companies

- Private hospitals

- Medical practitioners working in private practice

Both sectors work together to provide healthcare to Australians, with governments also funding population health programs, medical research, and Aboriginal and Torres Strait Islander health services. This dual-sector approach ensures Australians have options for how they access healthcare.

What is Medicare?

Medicare is Australia's universal health insurance scheme. This means it provides healthcare access to all eligible Australians, regardless of their income or health status.

Key facts about Medicare:

- Established in 1984

- Administered by the Federal Government

- Available to all Australian citizens and permanent residents

- Also available to people from countries with reciprocal healthcare agreements (including New Zealand, United Kingdom, Ireland, Belgium, Sweden, Netherlands, Finland, Italy, Malta, Slovenia, and Norway)

Medicare gives eligible people access to subsidised healthcare services. This means the government helps pay for medical costs, making healthcare more affordable.

What does Medicare cover?

Medicare covers a wide range of essential healthcare services. Understanding what's covered helps you know when you can access subsidised care.

Out-of-hospital expenses

Medicare pays all or part of the costs for many medical services outside of hospital. These include:

- Doctor consultations: Visits to general practitioners (GPs) and specialists

- Medical tests: X-rays, pathology tests (like blood tests), and eye tests by optometrists

- Surgical procedures: Most surgical and therapeutic procedures performed by GPs

Understanding the Medicare Benefits Schedule

The Medicare Benefits Schedule is an official document listing all covered services and how much Medicare contributes to each. The amount Medicare pays is called the schedule fee.

The government sets schedule fees based on what they consider a reasonable cost for each service. For example, in January 2021, the schedule fee for a standard GP visit was $38.75. This means Medicare contributes $38.75 every time you visit the doctor for a standard consultation.

Bulk billing vs patient co-payments

However, doctors can charge more than the schedule fee if they choose. This creates two possible scenarios:

Scenario 1: Bulk billing

- The doctor charges exactly the schedule fee

- Medicare pays the doctor directly

- You pay nothing out of pocket

- This is called bulk billing

Scenario 2: Patient co-payment

- The doctor charges more than the schedule fee

- Medicare still only pays the schedule fee

- You must pay the difference (called a patient co-payment)

- This creates an out-of-pocket expense for you

Worked Example: Understanding Patient Co-payments

If your doctor charges $50 for a consultation but the schedule fee is $38.75:

- Medicare pays: $38.75

- You pay: $11.25 (the gap between what the doctor charges and what Medicare pays)

This $11.25 is your out-of-pocket expense or patient co-payment.

Specialist services

When you visit a specialist (like a dermatologist for skin conditions, cardiologist for heart problems, or obstetrician during pregnancy), Medicare covers 85% of the schedule fee. This means:

- You will usually need to pay at least 15% of the schedule fee

- The specialist may charge more than the schedule fee, creating a larger gap

- Private health insurance may cover some or all of this gap

Dental services

Medicare generally doesn't cover dental care, but there's an important exception:

Child Dental Benefits Scheme

Available for children aged 2-17, this scheme provides up to $1000 of dental treatment over two years. The child must be eligible for Medicare and their family must receive certain government benefits (like Family Tax Benefit Part A or Youth Allowance).

Some surgical dental procedures performed by approved dentists may also be covered by Medicare.

In-hospital expenses

Medicare's coverage differs depending on whether you're a public or private patient.

As a public patient in a public hospital:

- Medicare covers all costs

- This includes accommodation, treatment by doctors and specialists, initial treatment, and aftercare

- You cannot choose your doctor

- You may need to wait for non-urgent treatment

As a private patient:

- Medicare pays 75% of the schedule fee for doctor and specialist treatment

- Medicare doesn't cover accommodation or other costs (like theatre fees or medication)

- This applies whether you're in a private hospital or a private patient in a public hospital

- Private health insurance may cover the remaining costs

Medicare Safety Net

The Medicare Safety Net provides extra financial help for people who spend a lot on medical services in one year.

How the Safety Net Works:

Once you've paid a certain amount in out-of-pocket costs for Medicare services in a calendar year, the government provides additional support. In 2019, this threshold was $470. After reaching this amount, Medicare provides higher rebates for the rest of that year, making medical services cheaper for you.

The Safety Net protects families and individuals from high medical costs, especially those with chronic conditions requiring frequent medical care.

What is not covered by Medicare?

Understanding what Medicare doesn't cover is just as important as knowing what it does cover. Medicare only covers "clinically necessary" services, meaning cosmetic or unnecessary procedures aren't included.

Services Not Covered by Medicare:

Medicare does NOT cover the following services and costs. Being aware of these exclusions helps you plan for additional healthcare expenses or consider private health insurance options.

Services not covered by Medicare:

Private hospital costs

- Medicare pays 75% of the schedule fee for doctor and specialist treatment in private hospitals

- It doesn't cover accommodation, theatre fees, medication, or other hospital costs

- Private health insurance can cover these gaps

Dental care

- Most dental examinations and treatments aren't covered

- You're responsible for paying your own dental costs

- Exception: Child Dental Benefits Scheme (as mentioned earlier)

Home nursing care and ambulance services

- Medicare doesn't cover nursing care or treatment at home

- Ambulance transportation is not covered (though some state governments or private insurance may cover this)

Allied health services

Allied health services are health services provided by trained professionals who aren't doctors, dentists, or nurses. Examples include physiotherapists, psychologists, and occupational therapists.

Medicare may contribute if these services are referred by a GP or provided in a public hospital. Otherwise, you pay the full cost.

Alternative therapies

Many treatments outside traditional medicine aren't covered by Medicare.

These include:

- Chiropractic services

- Acupuncture

- Remedial massage

- Naturopathy

- Aromatherapy

Medicare may contribute to these services if they're carried out or referred by a GP, but generally you'll need to pay for them yourself.

Health-related aids

Medicare doesn't cover the cost of:

- Glasses and contact lenses

- Hearing aids

- Artificial limbs (prostheses)

Pharmaceuticals

Prescription medicines aren't covered by Medicare, but they may be subsidised under the Pharmaceutical Benefits Scheme (PBS), which is a separate government program.

Compensation cases

If someone else is responsible for your medical costs (like a compensation insurer, employer, or government authority), Medicare won't contribute because that person or organization should pay.

You can purchase private health insurance to cover many services not included in Medicare. This is particularly useful for services like dental care, allied health services, and private hospital accommodation.

Advantages and disadvantages of Medicare

Like any health system, Medicare has both strengths and limitations. Understanding these helps you make informed decisions about your healthcare.

| Advantages | Disadvantages |

|---|---|

| You can choose your own doctor for out-of-hospital services | You cannot choose your doctor for in-hospital treatments as a public patient |

| Available to all Australian citizens, promoting equality | Waiting lists exist for many treatments, especially non-urgent procedures |

| Reciprocal agreements allow Australians to access free healthcare in selected countries | Does not cover alternative therapies like acupuncture or chiropractic |

| Covers essential tests, examinations, doctors' and specialists' fees (at schedule fee level), and procedures like X-rays and eye tests | Often doesn't cover the full amount of a doctor's visit if they charge above the schedule fee |

| The Medicare Safety Net provides extra financial support once you've reached a certain level of out-of-pocket expenses |

Exam Tip:

When discussing advantages, focus on universal access, affordability, and comprehensive basic coverage. When discussing disadvantages, emphasise waiting times, gaps in coverage, and limited choice in public hospitals.

How is Medicare funded?

Medicare requires significant funding to operate. The government uses three main sources to pay for Medicare services:

1. The Medicare levy

The Medicare levy is an additional tax on most taxpayers' income.

- Rate: 2% of taxable income

- Applied to most Australian taxpayers

- Some people with low incomes or specific circumstances may be exempt

Worked Example: Calculating the Medicare Levy

If you earn $50,000 per year, you pay $1,000 in Medicare levy.

Calculation:

This $1,000 is automatically deducted from your tax throughout the year.

2. The Medicare levy surcharge

This is an extra tax for high-income earners who don't have private health insurance.

Who pays:

- Individuals earning more than $90,000 per year (2020-21)

- Families earning more than $180,000 per year (2020-21)

How much: The surcharge increases with income:

- Income above $90,000: extra 1% surcharge

- Income above $140,001: extra 1.5% surcharge

Purpose of the Surcharge:

This encourages high-income earners to take out private health insurance, which reduces demand on the Medicare-funded public system. By incentivising private insurance, the government helps manage the workload on public hospitals and services.

3. General taxation

The Medicare levy and surcharge don't generate enough money to cover all of Medicare's costs. The government uses revenue from general taxation (income from all taxes) to make up the difference.

This three-part funding model ensures Medicare can continue providing services to all Australians. The combination of the levy (from most taxpayers), the surcharge (from high-income earners), and general taxation creates a sustainable funding base for universal healthcare.

Medicare usage and costs

Medicare usage has grown steadily over the past decade. Understanding these trends shows the increasing demand for healthcare services.

| Year | Total services provided (million) | Average services per person | Total cost ($ million) | Average cost per person ($) |

|---|---|---|---|---|

| 2009-10 | 308.0 | 14.2 | 15,413.7 | 710.6 |

| 2010-11 | 318.8 | 14.5 | 16,317.6 | 740.6 |

| 2011-12 | 332.2 | 14.9 | 17,639.2 | 789.6 |

| 2012-13 | 343.6 | 15.1 | 18,565.6 | 816.7 |

| 2013-14 | 356.1 | 15.4 | 19,122.6 | 826.8 |

| 2014-15 | 368.5 | 15.7 | 20,188.9 | 860.0 |

| 2015-16 | 384.0 | 16.1 | 21,107.8 | 866.3 |

| 2016-17 | 394.3 | 16.3 | 22,002.6 | 909.5 |

| 2017-18 | 414.3 | 16.8 | 23,196.3 | 943.0 |

| 2018-19 | 424.2 | 17.0 | 24,071.4 | 963.5 |

| 2019-20 | 428.3 | 16.9 | 24,689.2 | 973.6 |

Key Trends from the Data:

- The number of Medicare services provided increased by 39% between 2009-10 and 2019-20

- Average services per person grew from 14.2 to 16.9 per year

- Total costs increased by 60%, from $15.4 billion to $24.7 billion

- Average cost per person rose from $710.60 to $973.60

These increases reflect Australia's growing and ageing population, as well as advances in medical technology and treatments.

Remember!

Key Points to Remember:

-

Medicare is Australia's universal health insurance scheme, established in 1984, providing subsidised healthcare to all eligible Australians and permanent residents.

-

Medicare covers essential services including GP and specialist consultations (at schedule fee rates), medical tests like X-rays and pathology, eye tests, and free treatment as a public patient in public hospitals.

-

Bulk billing means no out-of-pocket costs because the doctor charges only the schedule fee, while patient co-payments occur when doctors charge above the schedule fee.

-

Medicare doesn't cover most dental care (except Child Dental Benefits Scheme), ambulance services, alternative therapies, health aids, or private hospital accommodation costs.

-

Medicare is funded through three sources: the Medicare levy (2% of taxable income), the Medicare levy surcharge (for high-income earners without private insurance), and general taxation.