Private Health Insurance – Further Exploration (VCE SSCE Health and Human Development): Revision Notes

Private Health Insurance – Further Exploration

What is private health insurance?

Private health insurance is voluntary insurance that you can purchase alongside Medicare. When you have private health insurance, you pay a regular fee called a premium in exchange for coverage of health-related costs that Medicare doesn't cover.

Key Definition

A premium is the amount you pay regularly for your insurance coverage – think of it as your insurance subscription fee.

This type of insurance plays an important role in Australia's health system. Private health insurance:

- Provides significant funding for healthcare services

- Gives Australians more choice about the type of care they receive

- Supports private hospitals, which provide approximately one-third of all hospital beds in Australia

- Accounts for about 40% of hospital separations (episodes of hospital care)

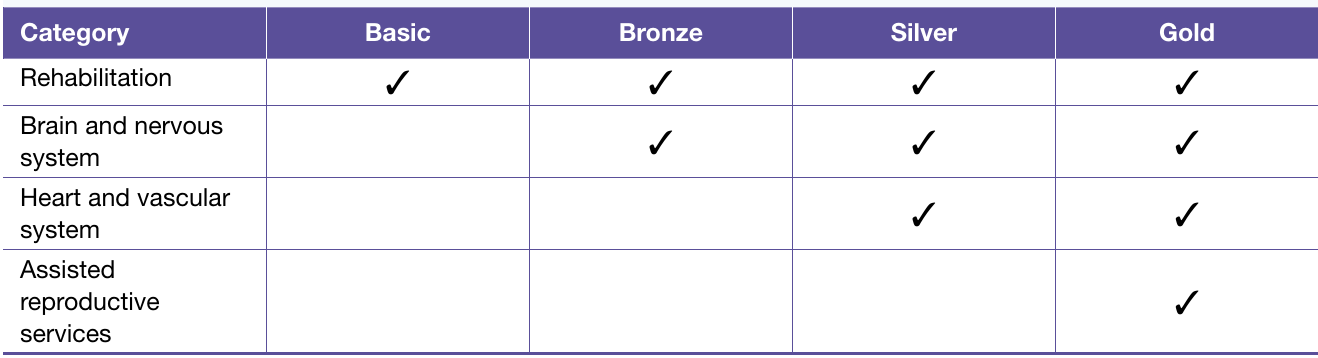

Hospital cover tiers

In 2020, the Australian government introduced a requirement for all insurers to classify their hospital policies into one of four tiers. These tiers make it easier to compare policies and choose the right level of coverage.

The four tiers are:

- Gold – provides the most comprehensive hospital treatment coverage

- Silver – covers the second-highest number of treatment categories

- Bronze – covers the second-lowest number of treatment categories

- Basic – offers the minimum level of hospital treatment coverage

Understanding Tier Selection

Each tier must meet minimum coverage requirements set by the government. Think of it like star ratings at hotels – more stars mean more services, but all must meet basic standards.

The table below shows selected services covered by each tier:

As you can see, all tiers cover rehabilitation services, but more specialised treatments like assisted reproductive services are only covered under Gold policies. When choosing hospital cover, you need to consider which services are most important for your circumstances.

Types of private health insurance cover

Private health insurance offers three main types of coverage options:

1. Private hospital cover – Covers costs associated with private hospital treatment. This allows you to be treated as a private patient in either public or private hospitals.

2. General treatment cover (also called "extras") – Covers services that Medicare doesn't typically cover, such as:

- Dental care

- Physiotherapy

- Chiropractic treatment

- Optometry

- Dietetics

You can choose which extras to include in your policy, but your premium increases with each service you add.

3. Combined cover – Provides both hospital and general treatment coverage in one policy. This option gives you the most comprehensive coverage but typically costs more than single-type policies.

Understanding how private health insurance works

Like all insurance, private health insurance operates on a premium-based system. Your premium amount varies depending on:

- How many people the policy covers

- Which type of cover you choose

- What services are included

Benefits of private health insurance

The main benefit of most hospital policies is the right to be admitted as a private patient. This applies to both public and private hospitals, and comes with several advantages:

When you're a private patient, you typically receive:

- Choice of doctor – You can select which doctor treats you

- Private room – You may have your own hospital room

- Reduced waiting times – You generally don't have to wait as long for elective (non-emergency) surgery, which can be a significant issue in the public system

How the costs break down

When you use private hospital services, the costs are shared between Medicare, your insurance company, and potentially yourself:

How Payment Works: Breaking Down the Costs

When you receive private hospital treatment, here's how the fees are divided:

Step 1: Medicare contributes 75% of the schedule fee (the government-determined fee for medical services)

Step 2: Your private health insurance covers most of the remaining costs

Step 3: You may need to pay "the gap" – any difference between what Medicare and your insurer pay and the total fee charged

Understanding "The Gap"

The gap occurs because private hospitals usually charge more than the schedule fee. While insurance companies cover most of these additional costs, sometimes the total bill exceeds what Medicare and your insurer contribute combined. In these situations, you must pay the difference out of your own pocket.

Many insurance companies have partnership arrangements with hospitals to minimize gap payments for their members.

Government incentives for private health insurance

When Medicare was introduced, many Australians cancelled their private health insurance because they could access essential treatments without paying expensive premiums. This created pressure on the public health system as fewer people used private hospitals.

To encourage more Australians to maintain private health insurance, the government has introduced four main incentives:

Private health insurance rebate

Originally introduced in 1999 as a flat 30% rebate, this incentive now operates on an income-tested basis since 2012.

For individuals under 65 years:

| Annual income | Rebate percentage |

|---|---|

| Under $90,000 | 25% |

| $90,001 - $105,000 | 17% |

| $105,001 - $140,000 | 8% |

| Over $140,000 | 0% |

For families:

The income thresholds are higher for families to reflect their additional expenses:

| Annual income | Rebate percentage |

|---|---|

| Under $180,000 | 25% |

| $180,001 - $210,000 | 17% |

| $210,001 - $280,000 | 8% |

| Over $280,000 | 0% |

Age-Based Rebate Increases

Older Australians receive higher rebate percentages:

- People aged 65-70 receive approximately an extra 4% rebate

- People aged over 70 receive approximately an extra 8% rebate

How to claim the rebate:

Eligible policyholders have two options:

- Pay a reduced premium, with the government contributing the rebate amount directly to the insurer

- Pay the full premium and claim the rebate back through their tax return

This incentive makes private health insurance more affordable and encourages more people to use private hospitals, which reduces pressure on the public system, particularly for elective surgery.

Lifetime Health Cover

This incentive encourages younger Australians to take up private health insurance and maintain it throughout their lives.

How it works:

If you first take out private hospital insurance after age 31, you pay an additional 2% on your premiums for every year you're over 30.

Loading Calculation Example

Someone who first takes out private health insurance at age 40 will pay 20% more for their premiums than someone who took out hospital cover at age 30.

Calculation: 10 years × 2% = 20% loading

Key Features of Lifetime Health Cover

- The maximum loading is 70%, which applies if you first take out cover at age 65

- Having more young people with private health insurance helps offset the costs of providing care for older Australians, who use healthcare services more frequently

- If you maintain continuous coverage for 10 years, the loading is removed and you'll pay the same as someone who joined at age 30

Medicare levy surcharge

This incentive specifically targets high-income earners who can afford private health insurance.

How it works:

If you earn above certain thresholds and don't have private hospital insurance, you must pay an extra tax called the Medicare levy surcharge:

- Individual threshold: $90,000 per year

- Family threshold: $180,000 per year

The surcharge is calculated as a percentage of your taxable income and ranges from 1% to 1.5%, depending on your income level.

This incentive encourages wealthy Australians to purchase private health insurance, taking pressure off the public system.

Age-based discount

Introduced in 2019, this is the newest government incentive. It gives insurers the option to offer discounts to young people aged 18-29 for hospital cover.

The discount provides up to 10% reduction in premiums, calculated at 2% for each year the person is under 30:

| Age when insured | Discount percentage |

|---|---|

| 18-25 | 10% |

| 26 | 8% |

| 27 | 6% |

| 28 | 4% |

| 29 | 2% |

| 30 | 0% |

How the discount changes over time:

Eligible policyholders keep their initial discount rate until age 41, then it decreases by 2% each year until reaching 0%.

Age-Based Discount: How It Changes Over Time

Example 1: Someone who joins at age 25 with a 10% discount:

- Receives 10% discount from age 25-40

- At age 41, discount reduces to 8%

- Discount continues decreasing by 2% each year

- At age 45, discount reaches 0%

Example 2: Someone who joins at age 28 with a 4% discount:

- Receives 4% discount from age 28-40

- At age 41, discount reduces to 2%

- At age 42, discount reaches 0%

Like all the incentives, the age-based discount aims to encourage more Australians to take out private health insurance and maintain it for life.

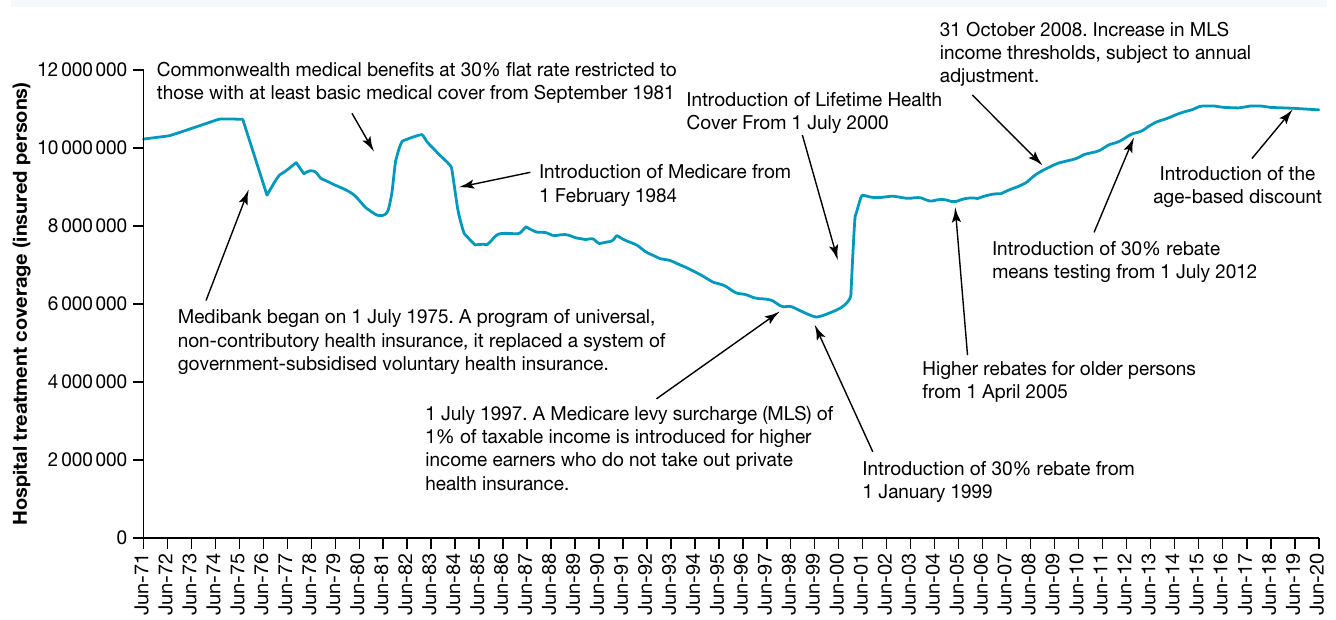

Historical trends in private health insurance

The number of Australians with private health insurance has changed significantly over time, responding to major policy interventions:

Key Observations from Historical Trends

- 1975 (Medibank introduction): Membership declined as Australians gained access to universal healthcare without needing private insurance

- 1984 (Medicare introduction): Further decline in private health insurance membership

- 1997 (Medicare levy surcharge introduced): Beginning of efforts to encourage private insurance uptake

- 1999 (30% rebate introduction): Sharp increase in membership as insurance became more affordable

- 2000 (Lifetime Health Cover): Dramatic spike in membership as people rushed to avoid premium loadings

- 2012 (Means testing of rebate): Slight decline as rebate reduced for high earners

- Recent years show relatively stable membership levels around 11-12 million people

These trends demonstrate how government policies significantly influence Australians' decisions about private health insurance.

Weighing up private health insurance

When deciding whether to purchase private health insurance, it's important to consider both the benefits and drawbacks.

Key Advantages and Disadvantages

Advantages:

- Access to private hospital care – You can be treated in private facilities with typically higher levels of comfort and service

- Choice of doctor – You can select which doctor treats you in both public and private hospitals

- Shorter waiting times – Significantly reduced wait times for elective surgery compared to the public system

- Coverage for additional services – Depending on your policy level, you can receive cover for dental, chiropractic, physiotherapy, optometry, and dietetics services

- Reduces Medicare costs – By using private hospitals, you help keep Medicare expenses under control

- Tax benefits – High income earners avoid paying the Medicare levy surcharge

- Government rebate – Eligible policyholders receive financial assistance with premiums

- Lifetime Health Cover benefit – Taking out cover early avoids premium loadings

- Age-based discount – Young people aged 18-29 may receive discounted premiums

Disadvantages:

- Expensive premiums – Regular payments can be substantial, particularly for comprehensive coverage

- Gap payments – Insurance may not cover the entire fee, leaving you to pay the difference

- Waiting periods – Some conditions (such as pregnancy-related services) require you to hold insurance for a specified time before you can claim

- Policy complexity – Understanding different policies and what they cover can be confusing and overwhelming for consumers

Remember: Key Takeaways

- Private health insurance is optional insurance that supplements Medicare by covering costs Medicare doesn't pay for

- Hospital policies are classified into four tiers (Gold, Silver, Bronze, Basic) with Gold offering the most comprehensive coverage

- You can choose hospital cover only, general treatment (extras) only, or combined cover

- The government has introduced four incentives to encourage private health insurance uptake: the rebate, Lifetime Health Cover, Medicare levy surcharge, and age-based discount

- While private health insurance offers benefits like choice and reduced wait times, it also comes with significant costs including premiums and potential gap payments