Production, Consumption and trade (AQA A-Level Geography): Revision Notes

Production, Consumption and trade

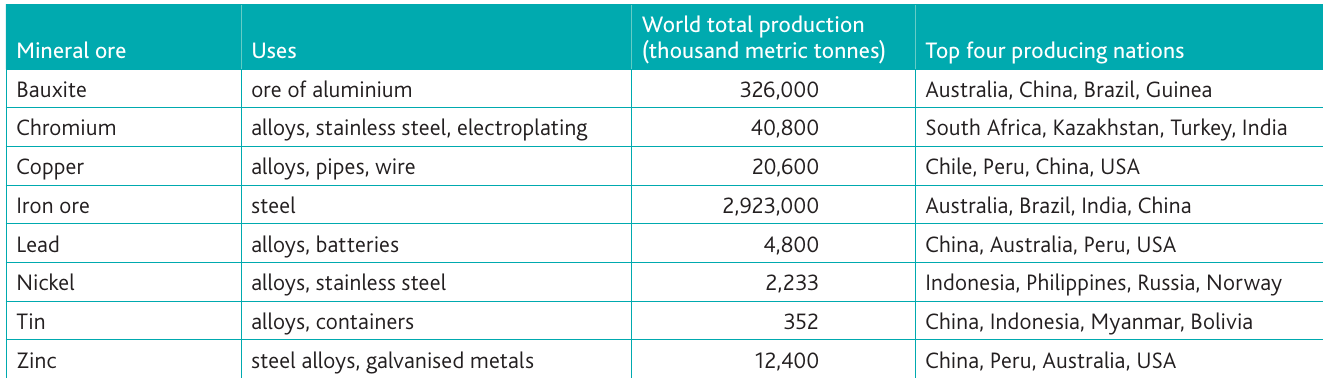

Introduction to mineral ores and global patterns

The geographical distribution of mineral deposits across the world creates uneven patterns of production and consumption. This mismatch between where minerals are extracted and where they are used has significant economic and geopolitical implications.

Understanding these patterns requires examining three key aspects:

- Where mineral ores are extracted (production)

- Where they are used in manufacturing and industry (consumption)

- How they move between countries (trade)

The Resource Curse

The resource curse (also called the 'paradox of plenty' or 'resource trap') describes how some countries with abundant natural resources fail to benefit from this wealth. Instead of experiencing economic growth, they may face minimal development. This paradox affects many mineral-rich developing nations.

Global patterns of mineral ore production

Geographical shifts in production

Over the last five decades, there has been a major geographical shift in where mineral ores are extracted from the earth. Historically, developed nations like the UK and USA extracted ores from their own reserves. However, these countries have now largely depleted their domestic resources.

This has led to a fundamental change in the global mining industry:

- Developed countries in North America, Europe and Oceania reduced their extraction activities

- Developing regions expanded their mining operations significantly

- Several emerging economies transformed into important mineral exporters

- Middle-income countries established themselves as key players in global mining

Major producing regions

Different regions specialise in producing particular types of mineral ores based on their geological endowments:

South America has emerged as a leading producer across multiple minerals:

- Brazil, Chile, Bolivia and Peru dominate production of various ores

- Brazil ranks as the world's second-largest iron ore producer (490 million metric tonnes)

- Chile leads in copper extraction

- The region benefits from extensive mining investment

South and South-east Asia plays an increasingly important role:

- India, Indonesia, Myanmar and the Philippines extract significant quantities

- These countries produce iron, chromium, nickel and tin

- The region combines geological advantages with growing technical capacity

Africa's Mineral Wealth

Africa contains vast mineral wealth across the continent, with six African nations ranking among the top global producers. Guinea dominates global bauxite production, while South Africa produces chromium and iron ore. The Democratic Republic of Congo extracts cobalt, and Zambia mines copper.

Developed nations maintain production despite depleted reserves:

- Australia continues as the world's largest iron ore producer (901 million metric tonnes in 2018)

- Canada remains a major producer of various metals

- Both countries host large transnational mining corporations

- They have extended operations overseas to developing countries

The production-consumption gap

A significant imbalance exists between extraction and use of mineral ores. Developing regions produce far more mineral resources than they consume domestically. This surplus results from foreign investment in their mining industries, with resources extracted primarily for export to industrial nations.

The gap between production and consumption can create 'mineral booms' that may or may not benefit local economies long-term. These booms are characterized by rapid expansion of mining activities, influx of foreign capital, and increased export revenues, but the lasting developmental benefits remain uncertain.

Global patterns of mineral ore consumption

Historical consumption patterns

Traditionally, developed industrial nations dominated the consumption of mineral ores. Countries in North America, Europe, Japan and South Korea used vast quantities of iron, steel, aluminium, copper and other metals in their manufacturing sectors.

These regions consumed more metals than they extracted because:

- They possessed large manufacturing industries producing cars, appliances and machinery

- Infrastructure development required substantial amounts of steel and other metals

- Service sectors needed materials for construction and utilities

- High living standards created demand for metal-intensive products

The rise of emerging economies

Patterns of consumption have shifted dramatically, particularly in the past two decades. China's rapid industrialisation has fundamentally altered global demand for mineral ores.

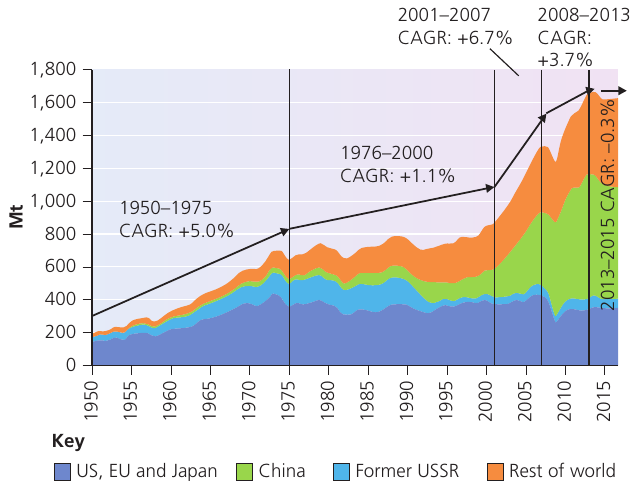

The Evolution of Global Steel Demand (1950-2015)

Between 1950 and 2015, global steel demand increased from approximately 300 megatonnes to nearly 1,700 megatonnes. Different periods show varying growth rates:

- 1950-1975: +5.0% CAGR (compound annual growth rate)

- 1976-2000: +1.1% CAGR (slowdown in developed economies)

- 2001-2007: +6.7% CAGR (China's rapid expansion)

- 2008-2013: +3.7% CAGR (post-financial crisis adjustment)

- 2013-2015: -0.3% CAGR (Chinese economic slowdown)

This transformation clearly demonstrates China's impact on global mineral consumption patterns.

De-industrialisation in developed countries

Consumption in more developed regions has slowed or declined due to several factors:

- Manufacturing industries relocated to countries with lower labour costs

- De-industrialisation reduced demand for industrial metals

- Mature infrastructure requires less new construction

- Service-based economies use fewer physical materials than manufacturing economies

China's dominant role in consumption

China has become the world's largest consumer of most mineral ores. This dominance stems from several interconnected factors:

Infrastructure development drove massive demand:

- Major construction programmes in urban areas required enormous quantities of steel

- Projects like the Three Gorges Dam used iron and steel extensively

- Development of national grid infrastructure increased copper consumption to 11 million metric tonnes

China's Industrialisation and Energy Infrastructure

Reliable energy supplies for factories necessitated extensive electrical infrastructure, which created ongoing demand for copper and other conductive metals. Manufacturing sectors expanded rapidly across multiple industries, and production of goods for both domestic and export markets consumed vast material quantities.

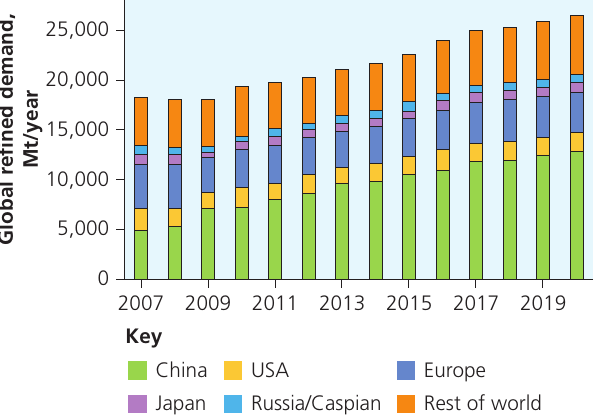

Copper demand patterns from 2007 to 2019 illustrate China's dominance:

- China (green) represents the largest single segment in every year

- Global refined copper demand grew from approximately 18,000 to 26,000 megatonnes per year

- China's share expanded significantly whilst other regions remained relatively stable

- Europe, USA, Japan and Russia/Caspian region maintained steady but smaller consumption levels

Manufacturing powerhouse status explains high consumption:

- China produces goods sold worldwide, requiring raw materials

- Aluminium consumption is particularly high for electronics and vehicles

- Rare earth metals (REEs) are essential for hi-tech products manufactured in China

China's Strategic Shift in Copper Processing

In 2019, China reduced imports of refined copper and instead purchased copper concentrate or partially processed ore. This shift occurred as China developed its own smelting capacity, demonstrating a strategic move up the value chain. The economic slowdown since 2014 also curbed demand for some metals, with reduced consumption of aluminium and steel causing global trade repercussions.

Consumption in other emerging economies

South Korea and India also demonstrate high growth in mineral consumption. When measured per capita (per person), South Korea actually surpasses all other countries in steel and copper consumption, reflecting its advanced industrial economy.

Global patterns of mineral ore trade

Understanding trade flows

The mismatch between production and consumption locations creates substantial international trade in mineral ores. Resources flow predominantly from developing to developed countries, though China's emergence has complicated this simple pattern.

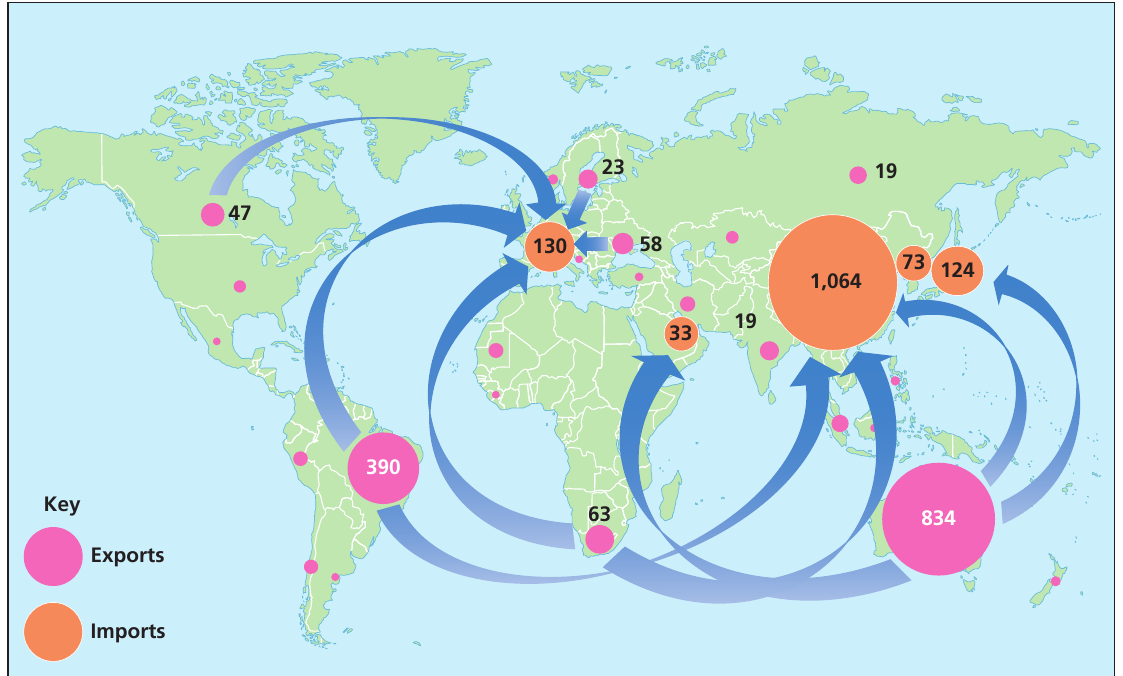

Global Iron Ore Trade Flows (2018)

The iron ore trade in 2018 demonstrates global patterns clearly:

Major Exporters:

- Australia: 834 million metric tonnes (largest global exporter)

- Brazil: 390 million metric tonnes (second-largest exporter)

- Africa: 63 million metric tonnes (emerging export hub)

Major Importer:

- China: 1,064 million metric tonnes (dominant global importer)

Blue arrows on the map show the direction and volume of trade flows, with trade moving primarily across the Pacific and Indian Oceans towards China. Iron ore exports correlate directly with steel production capacity.

Characteristics of mineral ore trade

Processing and transportation logistics shape trade patterns:

- Mineral ores undergo semi-processing in producing countries to discard waste material

- This concentrates the valuable mineral content before transport

- Large ocean-going vessels (ore-carriers) transport bulk commodities like iron ore and bauxite

- Ports near manufacturing centres receive shipments for final processing

- Ores are refined into finished metals at their destination

Market Volatility in Mineral Trade

Mineral commodity markets fluctuate more than fossil fuel markets. Energy demand remains relatively consistent whilst manufacturing cycles vary significantly. Economic recessions reduce demand for metals substantially, and price changes influence both production decisions and trade volumes.

Factors affecting mineral ore trade

Several interconnected factors determine how mineral ores are traded globally:

Demand inelasticity influences market dynamics:

- Specific minerals are needed for particular industrial uses

- Availability of substitute materials largely determines demand flexibility

- When alternatives exist, demand falls if prices rise

- Without substitutes, industries must pay higher prices

Global economic conditions drive trade patterns:

- Recessions and manufacturing declines reduce mineral ore demand

- Economic booms increase consumption and trade volumes

- The 2008 global financial crisis demonstrated this effect dramatically

Mining company investment decisions respond to prices:

- Falling demand and prices discourage investment in new mines

- Companies become reluctant to expand production when profitability declines

- This can lead to future supply shortages when demand recovers

Technological Changes and Supply Dynamics

Innovations can reduce production costs, increasing supply, while new extraction methods make previously inaccessible deposits viable. These changes can shift competitive advantages between producing regions and alter the global landscape of mineral production.

Environmental considerations increasingly affect trade:

- Concerns about mining impacts discourage new exploration in some regions

- Stricter regulations can reduce production in developed countries

- However, environmental awareness also encourages recycling

- Increased use of secondary materials (recycled metals) reduces demand for newly mined ores

- Alternative materials (such as silicon optical fibre replacing copper in telecommunications) reduce primary ore demand

China's impact on global trade patterns

China's role in mineral ore trade has transformed global patterns fundamentally:

Geographical reorientation of trade:

- Trade flows shifted from the Atlantic towards Asia and the Pacific

- China and South Korea became the primary destinations for mineral ores

- Australia and Brazil emerged as dominant exporters supplying Asian demand

- African mines increasingly export to China rather than European markets

China's Extreme Supply-Demand Imbalances

China consumes far more minerals than it produces domestically. Despite having significant mineral reserves, rapid consumption exceeds extraction. Imports from around the world fill the gap between production and consumption, creating one of the most significant trade relationships in the global mineral market.

Specific trade relationships developed:

- Australia supplies the majority of China's iron ore imports

- Brazil provides substantial iron ore quantities

- African nations export copper and other metals to Chinese manufacturers

China's Strategic Import Increases During the 2009 Recession

Despite the global economic slowdown in 2009, China significantly increased its mineral ore imports to fill resource shortage gaps:

- Iron ore imports: +33%

- Copper imports: +14%

- Aluminium imports: +800% (eight times increase)

These increases occurred despite slowing economic growth, demonstrating China's strategic approach to securing mineral resources during periods of lower global competition.

China's changing role has evolved over time:

- By 2014, Chinese economic growth began slowing

- Demand for mineral ores and metals declined as a result

- Some metals became stockpiled in China as production exceeded immediate needs

- China transformed into a net exporter of iron and steel

- Despite exporting steel, China still produced more than needed domestically

- This shift created downward pressure on global mineral prices

Impact of economic cycles on trade

The 2008 global financial crisis and subsequent recession revealed how economic conditions affect mineral ore trade:

Immediate crisis effects:

- Weakening of global mineral ore markets occurred generally

- Reduced trade volumes reflected falling manufacturing output

- Metals like steel and aluminium faced decreased demand

- Recycling of existing metals increased as primary ore prices fell

Material substitution accelerated during the downturn:

- Silicon optical fibre replaced copper in telecommunications applications

- This reduced copper demand in this sector permanently

- Lower ore prices made some alternative materials more attractive cost-wise

Production Responses to Falling Demand

Mining TNCs that dominate global trade reduced extraction to help prevent price collapse. Lower production helped stabilize markets, though some mineral prices (particularly copper) still fell substantially by 2018/19.

Recovery prospects remain uncertain:

- Further global economic recession (such as from the COVID-19 pandemic of 2020) could counter any recovery

- Long-term demand patterns may shift as economies restructure

- Alternative materials and recycling may permanently reduce demand for some ores

Geopolitics of mineral ores

Key geopolitical issues

The global trade in mineral ores creates various political and economic tensions between nations. Several fundamental issues arise:

International trade interdependency:

- Producing countries depend on export revenues from mineral sales

- Consuming countries rely on imports to supply their industries

- This mutual dependence creates complex political relationships

- Disruptions to supply chains affect both parties negatively

Trade conflict potential:

- Fluctuating prices for different minerals can spark disputes

- Producing countries may restrict exports to increase prices

- Consuming countries may seek alternative suppliers to reduce dependence

- Competition between major consumers (such as China and developed nations) can drive prices up

Access to Common Resources

Some mineral deposits exist in contested territories or international waters, raising complex questions about resource rights and access. Future conflicts may arise over access to these resources, and deep-sea mining introduces new legal and political challenges.

Environmental and socio-economic impacts:

- Mining developments create substantial environmental damage in producing regions

- Local communities often bear environmental costs whilst profits go elsewhere

- Social disruption, habitat destruction and pollution affect mine host communities

- These issues can cause political instability in producing countries

Transnational mining corporation dominance:

- Large TNCs control much of the global mining industry

- Their power exceeds that of some host governments

- Decisions made by corporations affect entire national economies

Joint Ventures in Mining

A joint venture is a commercial enterprise undertaken by two or more parties who agree to pool their resources and share ownership, risks and returns. In mining, agreements are often between two or more large TNCs or between a large corporation and the government of the host country. This arrangement allows governments to maintain some control over resource extraction whilst accessing technical expertise and capital.

Trade and development management

The expansion of mineral extraction in Africa, Latin America and parts of Asia has occurred because of several enabling factors:

Technological advances opened new possibilities:

- Innovations made mining in remote, less developed regions economically viable

- Previously inaccessible deposits became exploitable

- Improved transportation infrastructure connected mines to ports

Large ocean-going vessels facilitated bulk transport:

- Development of massive ore-carriers enabled cost-effective long-distance shipping

- These ships transport commodities like iron ore and bauxite in huge quantities

- Efficient bulk transport made distant mines competitive with closer sources

Development benefits and the resource curse

Trade in mineral ores presents a paradox for developing countries. Theoretically, foreign investment should bring economic and social benefits through resource exports. When managed well by a developing country's government, mineral wealth can create greater prosperity.

However, many resource-rich, low-income countries do not maximise their mineral wealth benefits. They experience the resource curse (sometimes called the 'paradox of plenty'), where natural resource abundance fails to generate expected development.

Why the Resource Curse Occurs

Several interconnected factors explain why resource-rich countries often fail to develop:

- Export revenues may not reach the general population

- Wealth concentrates in hands of elites or foreign corporations

- Corruption diverts funds from development projects

- Economic dependence on single commodities creates vulnerability

- Price fluctuations cause economic instability

- Environmental costs reduce quality of life

- Social disruption from mining undermines traditional livelihoods

Responses to overcome the curse:

Some developing countries have introduced policies to expand income from mineral deposits and ensure fairer benefits.

Indonesia's Policy to Add Value to Mineral Exports

Indonesia provides an example of government intervention to capture more value from mineral resources:

The Policy:

- The government prohibited export of unprocessed bauxite and nickel

- Mining TNCs must negotiate licences requiring ore processing in Indonesia

- This ensures jobs in higher-value processing industries

- It retains a greater share of the 'higher value' exports within the country

The Impact:

- The ban initially reduced global supplies of nickel and bauxite

- Reduced supply caused price rises for these minerals worldwide

- Indonesia captured more economic value from its resources

- Local employment in processing industries increased

China's geopolitical impact on mineral ores

China's role in the global mineral trade carries significant geopolitical implications for other countries. China's actions to secure access to reserves affect both low-income producing countries and TNCs from countries competing with China for similar resources.

For producing countries:

- China's large-scale purchasing provides guaranteed markets

- However, dependence on Chinese demand creates vulnerability

- Chinese state-owned enterprises invest heavily in foreign mines

- These investments may come with political strings attached

- Infrastructure development deals often accompany mineral purchase agreements

For competing consumers:

- Developed countries find themselves in competition with China for supplies

- This applies especially to iron/steel and copper industries

- TNCs from Europe, North America and Australia must compete with Chinese firms

- Higher prices result from increased competition for limited resources

China's Mineral Endowment and Strategy

China possesses substantial mineral resources including iron ore and copper. However, rapid industrial growth meant domestic production could not meet demand. China pursued a dual strategy: continued increasing domestic production whilst simultaneously importing huge quantities from overseas. This approach secured supply whilst maintaining price competition.

Three main global geopolitical effects resulted:

- Reshaping of global trade flows towards Asia

- Increased investment by Chinese companies in foreign mines

- Growing political influence in mineral-producing regions

- Competition with traditional mining powers for resources and markets

- Price volatility affecting global mineral ore markets

The combination of China's resource wealth, geographical position, large population and manufacturing growth established it as the global leader in mineral ore trade. This dominance creates both opportunities and challenges for other participants in the global mining industry.

Key Points to Remember:

-

Global production has shifted from developed to developing countries over the past 50 years, with regions like South America, Africa and South-east Asia now dominating extraction whilst developed nations have depleted their reserves.

-

China consumes more mineral ores than any other country, driving global demand especially for iron, steel, copper and aluminium. However, since 2014, Chinese economic slowdown has reduced this demand, affecting global trade patterns and prices.

-

Mineral ore trade flows predominantly from developing to developed nations, with Australia and Brazil as major exporters and China as the dominant importer. Trade has shifted geographically from the Atlantic towards Asia and the Pacific.

-

The resource curse affects many mineral-rich developing countries, where natural resource abundance fails to generate expected economic development due to corruption, poor governance, and exploitation by foreign companies.

-

Geopolitical tensions arise from mineral ore trade due to interdependency, price fluctuations, competition for resources, and the dominance of large transnational corporations and China in the global mining industry.