Economic Growth (Edexcel A-Level Economics A): Revision Notes

Economic Growth

Introduction to economic growth

Economic growth is a fundamental objective for any society. Governments have a key responsibility to ensure that citizens enjoy adequate standards of living and experience improvements in their well-being. To achieve this, the economy needs to expand the resources available to produce goods and services. Economic growth enables societies to provide better living conditions for their populations and create opportunities for future prosperity. However, pursuing growth involves important considerations about its costs and potential trade-offs with other economic objectives.

Defining economic growth

Economic growth can be understood in two distinct ways, each offering a different perspective on how an economy expands.

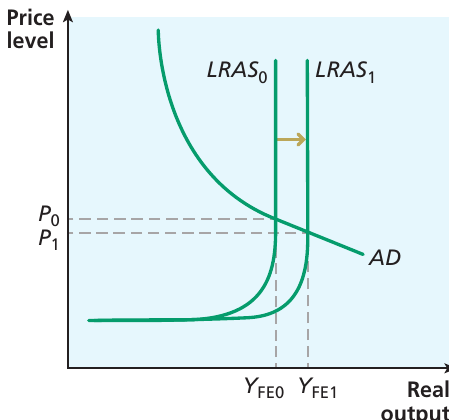

Potential economic growth refers to an increase in the economy's productive capacity. This represents the maximum amount of goods and services an economy could produce if all its resources were being used fully and efficiently. From a theoretical perspective, potential growth occurs when the economy's ability to produce expands over time.

This can be illustrated using the aggregate demand and aggregate supply (AD/AS) model. When the skills of the workforce improve, for example, firms become capable of producing greater output at any given price level. This causes the long-run aggregate supply (LRAS) curve to shift rightwards, moving from LRAS₀ to LRAS₁. The shift demonstrates an increase in full employment output, from Y_FE0 to Y_FE1, representing growth in the economy's productive capacity. The price level may fall from P₀ to P₁ as a result of this expansion.

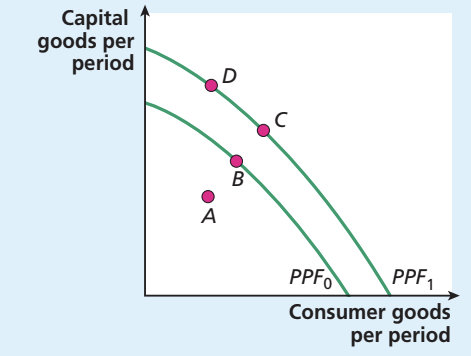

Potential growth can also be illustrated using a production possibility frontier (PPF). The PPF shows the maximum combinations of goods and services an economy can produce when using all its resources efficiently. Economic growth is represented by an outward shift of the entire PPF. For instance, the movement from the lower frontier to the upper frontier shows an expansion in productive capacity. Point A lies inside the frontier, indicating the economy is not using all its resources efficiently. Points B, C, and D represent different production combinations, with B on the original frontier and C and D on the new, expanded frontier following economic growth.

Understanding the PPF and Economic Growth

When the PPF shifts outward, it demonstrates that the economy can now produce more of both types of goods. Any point inside the PPF (like point A) represents inefficient production with unused resources, while points on the frontier represent efficient production at full capacity.

Actual economic growth refers to the rate of increase in real GDP over a period of time. This measures the actual change in the value of goods and services produced in the economy, calculated as the percentage change in the level of real GDP. Actual growth may occur when an economy moves closer to using its full productive potential, such as when recovering from a recession. For example, if an economy is operating below full capacity with unemployed resources, an increase in aggregate demand can lead to higher real output without necessarily expanding the economy's overall productive capacity.

Critical Distinction: Level versus Rate

Students must clearly distinguish between the level of real GDP and the rate of economic growth:

- The level refers to the total value of output at a point in time

- The rate of growth measures the percentage change in this level over time

This distinction is crucial for understanding economic data and trends. For example, an economy can have a high level of GDP but a low growth rate, or vice versa.

The output gap

The output gap represents the difference between actual real GDP and the maximum potential real GDP that could be achieved if the economy were operating at full capacity. Understanding this concept helps economists assess whether an economy is performing at, above, or below its sustainable level.

Negative output gap

When the economy operates below its full employment level, the output gap is negative. In this situation, there exists unused capacity within the economy. This might manifest as unemployment, where workers cannot find jobs, or as capital equipment sitting idle in factories. The economy is producing less than it could if all resources were being utilised efficiently.

Understanding Negative Output Gaps

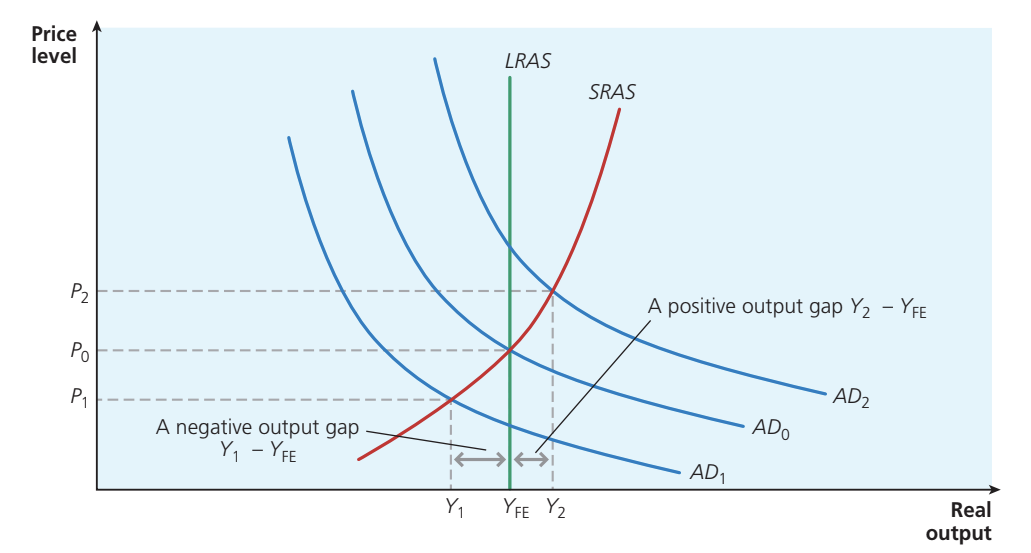

Under Keynesian analysis, if the economy is at equilibrium below full capacity, aggregate demand is insufficient to generate full employment. For instance, when aggregate demand is at AD₁, actual output is Y₁, which falls short of the full employment level Y_FE. The gap between Y₁ and Y_FE represents the negative output gap. Such situations can persist over extended periods, particularly following economic recessions.

Positive output gap

It is possible, though only temporarily sustainable, for an economy to experience a positive output gap, where actual real GDP exceeds the economy's normal capacity level. This might occur if firms respond to a surge in aggregate demand by asking workers to work overtime, or by operating machinery beyond its normal capacity. For example, in response to increased demand (shown as a shift to AD₂), actual output Y₂ might exceed the full employment level Y_FE.

However, this situation cannot be maintained in the long run. Operating beyond normal capacity creates inflationary pressures as firms compete for limited resources, and it places unsustainable strain on workers and capital equipment. Eventually, the economy must return to a more sustainable level of production.

Measuring the output gap

The Challenge of Measurement

A significant challenge for policymakers is that measuring the output gap proves difficult in practice. While economists can observe and measure actual real GDP, potential GDP cannot be directly observed. It must be estimated using statistical techniques that identify the underlying trend rate of growth. Determining exactly when an economy is operating at full capacity remains inherently uncertain, making policy decisions more challenging.

Sources of economic growth

Economic growth fundamentally arises from the use of factors of production: capital, labour, enterprise, and land. When all factors are being utilised fully and efficiently, this determines capacity output. An increase in capacity output can occur through two main routes: either by increasing the quantity of factors of production available, or by improving the efficiency with which these factors are used (productivity improvements).

Capital

Capital plays a critical role in the production process. When capital input increases, it provides an important source of economic growth. For capital to accumulate and expand the economy's productive capacity, investment needs to take place. Investment refers to expenditure undertaken by firms when they purchase capital goods such as machinery, equipment, and buildings.

In the national accounts, economists measure investment using gross fixed capital formation. This covers net additions to the capital stock, though it also includes depreciation (the wearing out of existing capital over time). Without sufficient investment to replace depreciating capital, the capital stock would gradually decline.

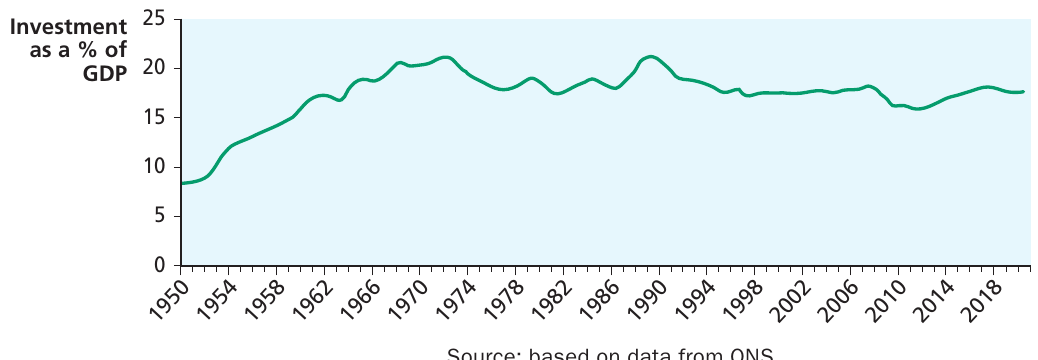

The UK's investment history shows interesting patterns. Investment as a percentage of GDP rose dramatically from around 8% in 1950 to peak levels of approximately 20-21% in the early 1970s. Following this peak, investment fluctuated between 17-21% through the 1980s and 1990s. More recently, there has been a gradual declining trend, with investment settling at around 17-18% by 2018. The chart clearly shows the dip that occurred during the recession of the late 2000s, followed by a period of recovery.

The Investment-Consumption Trade-off

Any society faces an important choice between using resources for current consumption versus allocating them to investment. Investment requires sacrificing present consumption to make more resources available in the future. This represents a fundamental trade-off that economies must navigate.

The contribution of capital to growth is reinforced by technological progress. New capital equipment typically embodies more advanced technology than older capital being replaced. For example, the speed and power of computers has increased enormously over recent years, having a significant impact on productivity. This means that technology enhances the contribution that investment makes towards enlarging capacity output in an economy. The productivity of new capital exceeds that of old capital being phased out, amplifying the growth effects of investment.

Innovation also contributes to economic growth. Through the invention of new forms of capital equipment and new ways of using existing capital more effectively, both technological progress and innovation can support economic expansion.

Labour

While capital is sometimes seen as the primary driver of growth, labour also makes a key contribution. However, there is relatively limited scope for increasing the size of the labour force within a country, except through international migration. (Encouraging population growth represents a rather long-term policy option with many other implications.) Nonetheless, the size of the workforce does contribute to determining the level of capacity output.

For example, the establishment of the European Single Market in 1993 allowed increased migration to the UK. Many economists view this as having enabled economic growth by expanding the available workforce. Conversely, the size of the workforce can also decline, with serious consequences for economic growth.

Real-World Impact: The HIV/AIDS Epidemic in Sub-Saharan Africa

A striking example of workforce decline occurred in several sub-Saharan African countries during the HIV/AIDS epidemic. The spread of this epidemic had a devastating impact in numerous countries across the region. The disease disproportionately affected people of working age, diminishing both the size of the workforce and the productivity of workers. These effects persisted even after the epidemic passed its peak, creating long-lasting damage to these economies' productive capacity.

Human capital

The quality of labour input proves more responsive to policy interventions than simply expanding workforce numbers. Education and training can improve worker productivity, and this can be regarded as a form of investment in human capital. Human capital represents the stock of skills and expertise that contribute to a worker's productivity, and it can be enhanced through education and training programmes.

For many developing countries, the provision of healthcare and improved nutrition can be seen as additional forms of investment in human capital. Such investments can lead to future improvements in productivity. The image shows a mobile clinic operating in the Central African Republic, where a healthcare worker is consulting with a patient and distributing medical supplies. This type of healthcare provision helps improve the health and productivity of the population, contributing to long-term economic growth potential.

Education and healthcare represent important areas where governments can intervene to support human capital development, addressing potential market failures in these sectors.

Productivity

Productivity measures the efficiency of a factor of production. Different types of productivity can be measured:

- Labour productivity measures output per worker, or more helpfully, output per hour worked. This latter measure is more useful because total output is clearly affected by the number of hours worked, which varies considerably across countries.

- Capital productivity measures output per unit of capital employed.

- Total factor productivity refers to the average productivity of all factors combined, measured as the total output divided by the total amount of inputs used.

When productivity increases, it raises aggregate supply and expands the potential capacity output of an economy, thus contributing to economic growth. Productivity improvements mean that the same quantity of inputs can produce more output, or equivalently, that less input is required to produce the same output.

International trade

International trade can contribute significantly to economic growth. Indeed, for many relatively small countries, international trade forms a key part of achieving economic growth. If a country's domestic market is not sufficiently large, effective demand may not allow economies of scale to be fully exploited. By engaging in international trade, a country gains the ability to specialise in producing goods more efficiently, reaping the gains from large-scale production.

For developing countries, this is especially important. Not only is access to large markets crucial, but it is also important to be able to earn the foreign exchange needed to import physical capital that cannot be produced domestically. Countries that have been most successful in achieving economic growth over recent decades have relied heavily on their ability to expand rapidly through promoting exports.

This strategy is known as export-led growth. Examples include the east Asian 'Tiger' economies that enjoyed rapid growth from the 1960s onwards, such as South Korea, Singapore, Hong Kong, and Taiwan. More recently, China has experienced unprecedented success in economic growth, founded upon the rapid expansion of exports. The export-led growth China achieved has created one of the most dramatic examples of sustained economic growth in history.

China's Export-Led Growth Strategy

China's growth could not have been based on the domestic market alone. The high level of investment, combined with rightward shifts in both aggregate demand and aggregate supply, drove this remarkable expansion. China's growth did falter when the COVID-19 pandemic struck, with GNI growth falling to just 1.9% even in 2020.

Understanding Opportunity Costs: China's Trade-off

China's economic growth has been enabled by exceptionally high investment and exports. Students should consider what opportunity cost this might involve. The high investment rate implies that resources have been diverted away from current consumption, meaning that while China has grown rapidly, consumption levels have remained relatively lower than they might otherwise have been. This represents a trade-off between present and future consumption.

Growth and aggregate demand

The discussion of growth sources has focused primarily on potential economic growth and the factors affecting aggregate supply. This is because the productive capacity of the economy can only increase when the LRAS curve shifts to the right. But how does aggregate demand fit into the picture?

An increase in aggregate demand can lead to higher real output in the economy if the initial equilibrium occurs below full capacity output. However, this is equivalent to a movement towards the PPF rather than a shift of it. In other words, an increase in aggregate demand represents actual economic growth that does not affect the overall productive capacity of the economy.

The Investment Exception

There is one important exception to this principle. If the increase in aggregate demand results from an increase in investment expenditure, this will later enable an increase in productive capacity. Higher investment today adds to the capital stock, which subsequently expands the economy's ability to produce goods and services in the future. This connection between aggregate demand and long-run supply explains why investment is so crucial for sustained economic growth.

The trade (business) cycle

The process of actual economic growth is not always smooth. Real GDP tends to fluctuate over time rather than growing at a constant, steady rate. The pattern of real GDP varying around its underlying trend is known as the trade cycle or business cycle. At any point in time, GDP may be below or above its trend value.

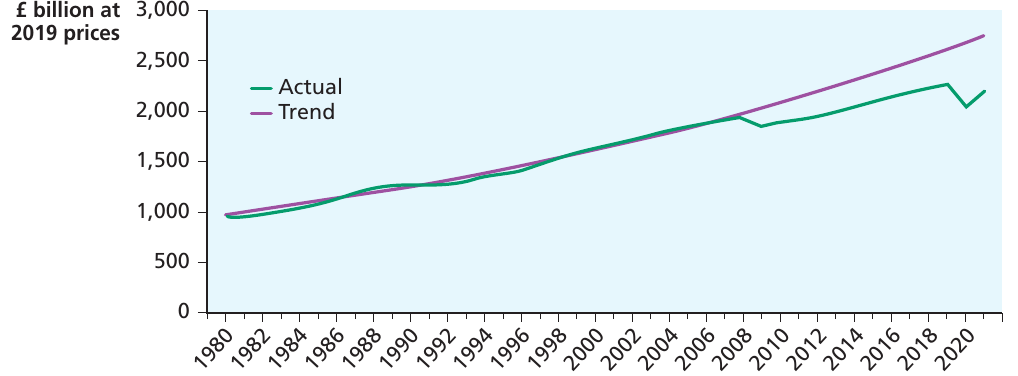

This diagram shows the actual path of real GDP in the UK from 1980 to 2020, measured in billions of pounds at 2019 prices, alongside its underlying trend. The trend line is calculated based on the average growth rate between 1980 and 2007. Although the two series track fairly closely for much of the period, you can see how the actual path of real GDP fluctuates around the trend, especially in the middle part of the period. The recession that started in 2008 is particularly apparent, when GDP dropped significantly below its trend value. By 2021, the economy was still operating at an appreciably lower level than if the pre-2007 trend rate of growth had continued. Furthermore, real GDP saw a further dip during the COVID-19 pandemic, and remained lower than it had been before the pandemic struck.

Phases of the trade cycle

The trade cycle displays a characteristic pattern with several identifiable phases. Consider an economy at the beginning of a recessionary period, where GDP is falling. This continues until the economy reaches the trough of the cycle, at which point GDP stops falling and begins to grow again. At this stage, the economy shows growth in actual GDP, but output still remains below its trend value. Recovery has set in. Only when the economy reaches its trend level does the output gap become zero.

Beyond this point, the economy moves into a boom period, where GDP grows more rapidly than its trend value, and the level of GDP rises above its trend value. At some stage, the cycle reaches its peak and stops increasing. Beyond this point, actual GDP again begins to fall as the economy enters the slowdown phase, and then the cycle repeats itself.

Macroeconomic indicators through the cycle

The stages of the cycle can be identified through macroeconomic indicators. During recession, unemployment is likely to be relatively high, but inflation may be lower. During recovery, unemployment may begin to fall as the economy expands, but once the economy enters the boom stage and approaches full employment, pressure on prices will increase and inflation will tend to rise.

Policy Implications Throughout the Cycle

As the economy nears its full capacity, firms will experience labour shortages and rising costs. This may cause them to slow their expansion, leading to a slowdown in the economy. This slowdown may at some point develop into a recession. From a policy perspective, it is important to understand what stage of the trade cycle the economy is experiencing.

When the output gap is negative, with output below trend, policymakers might be tempted to try to 'fill the gap' by stimulating aggregate demand. However, this approach would be dangerous when the output gap is positive, as it would put upward pressure on the price level and generate inflation.

Defining Recession Accurately

It is important to note that recession is defined as occurring when GDP falls for two or more consecutive quarters. Looking at quarterly growth data helps identify when an economy has entered recession. Notice that it is negative growth that defines a recession – that is, when the growth rate falls below zero. In the 2007-10 data, the UK did not officially enter recession until the last quarter of 2008, which was the second successive quarter in which growth had been negative.

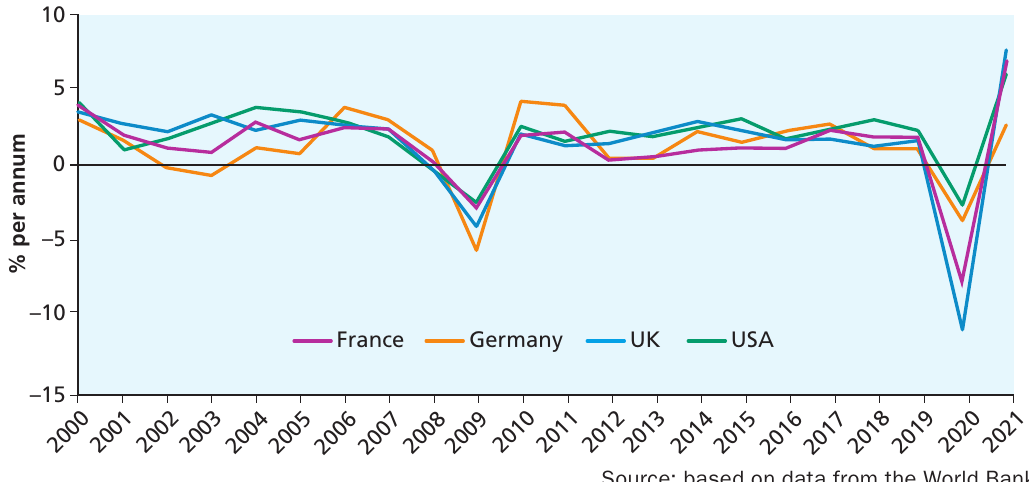

Real GDP in the UK and elsewhere

Examining the actual time path of real GDP provides valuable evidence about how economies experience growth and fluctuations. This chart shows annual growth rates for four major economies – France, Germany, the UK, and the USA – from 2000 to 2021. The data, sourced from the World Bank, reveals several important patterns.

Although the graph appears somewhat congested with multiple lines, it usefully demonstrates that there are periods when fluctuations occur simultaneously across countries. Most clearly shown is how all of these economies experienced negative growth in 2009 as the financial crisis affected the global economy. The chart also clearly reveals the impact of the COVID-19 pandemic in 2020, when growth rates plummeted dramatically for all four countries, with declines ranging from approximately -5% to -11%. This was followed by a sharp recovery spike in 2021, with growth rates reaching up to 7%.

The visualization highlights the extent to which modern economies are interconnected and experience common external shocks. When a major global event occurs, such as a financial crisis or pandemic, its effects spread across countries rather than remaining isolated.

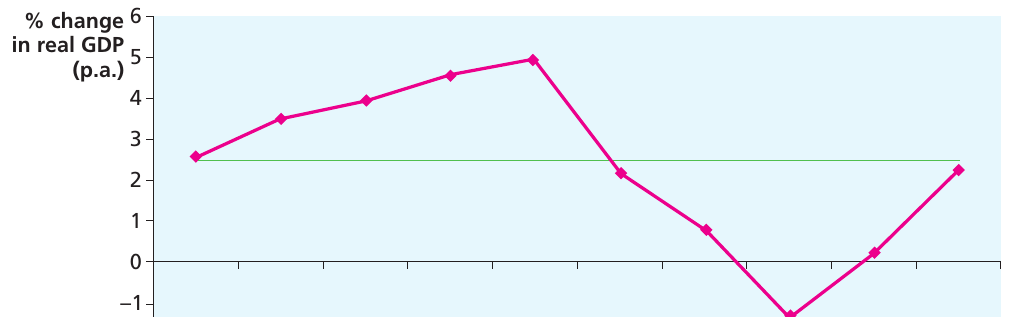

The 1984-1993 business cycle

Classic Business Cycle: UK 1984-1993

A classic example of the business cycle occurred in the UK from 1984 to 1993. GDP was above its trend value from 1985 to 1988, but then GDP fell below the trend as the economy went into recession. The term recession is only used when GDP falls for two or more consecutive quarters. This pattern clearly illustrates the characteristic phases of the business cycle, with a boom period followed by contraction and recession.

The 2008 financial crisis

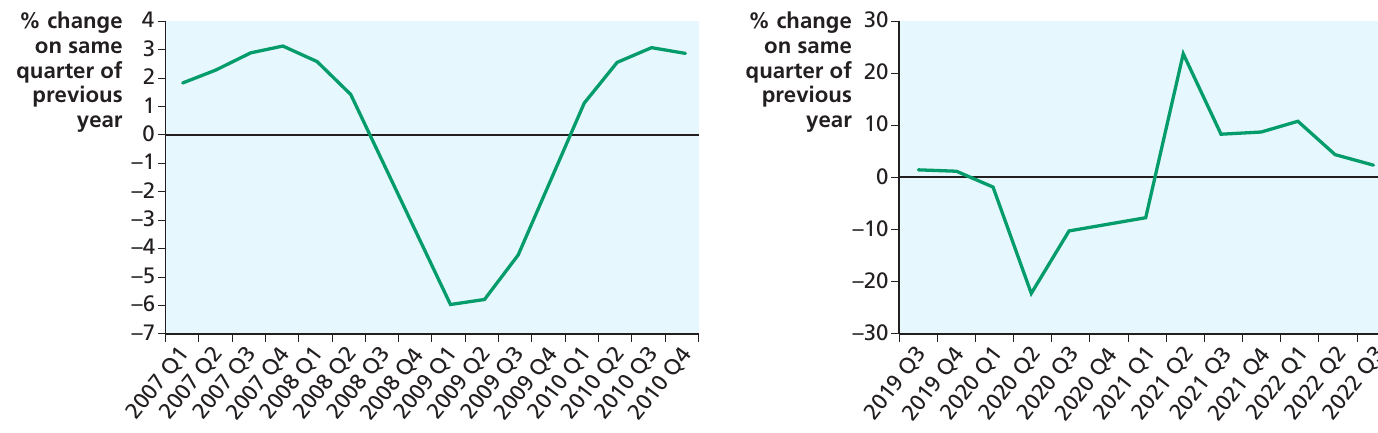

In mid-2008, the Chancellor of the Exchequer took the unprecedented step of publicly stating that the UK was heading for its biggest recession since the Second World War. This was unprecedented because most chancellors typically avoid saying anything that might damage expectations about the economy. The data for the period 2003 to 2008 shows the information that was available to the chancellor when he made this claim. He was correct – as subsequent data confirmed, though the further recession caused by the COVID-19 pandemic was to eclipse the impact of the financial crisis.

These two panels provide a stark comparison between two major economic crises. The left panel shows quarterly percentage changes during 2007-10, displaying the V-shaped pattern of the financial crisis, where growth fell from around +3% to approximately -6% before recovering. The right panel shows 2019-23, highlighting the much more severe but shorter-lived impact of COVID-19, with growth plummeting to about -23% in Q2 2020, followed by a dramatic rebound spike to approximately +25% in Q2 2021. The scale and speed of the pandemic's economic impact clearly exceeded that of the financial crisis.

The benefits of economic growth

Expanding the availability of resources in an economy enables the standard of living within a country to increase. In industrial economies, populations have come to expect steady improvements in incomes and available resources over time.

For households, economic growth may bring higher incomes and more employment opportunities. When the economy is growing, firms require more workers, creating job opportunities and potentially raising wages. This improves household living standards and provides greater economic security.

For firms, economic growth may bring higher profits. When aggregate demand is rising alongside productive capacity, businesses can sell more output, potentially at better prices. This improves profitability and provides resources for further investment.

For governments, economic growth may bring higher tax revenue and improved capacity to provide public goods. As incomes rise, tax revenues automatically increase (assuming tax rates remain constant). This gives governments more fiscal space to fund public services, infrastructure, and welfare programmes.

If the economy is buoyant and growing, this is likely to be accompanied by an increase in confidence among consumers and businesses. Higher confidence may encourage further investment spending, creating a virtuous circle of growth. Consumer confidence affects spending patterns, while business confidence influences investment decisions.

For developing countries, economic growth may facilitate the easing of poverty and allow investment in human capital that will improve standards of living further in the future. Growth provides resources that can be directed towards education, healthcare, and infrastructure that support long-term development. However, it is important to note that the benefits from growth may be concentrated in certain groups within a society rather than being spread widely, raising concerns about inequality and the distribution of growth benefits.

The Primacy of Economic Growth

Thus, for any society, economic growth is likely to be seen as a fundamental objective, perhaps even the most important one. Some economists argue that other policy objectives should be regarded as subsidiary to the growth target. In other words, achieving control of inflation, maintaining full employment, and ensuring stability in the current account of the balance of payments are seen as important short-run objectives primarily because their achievement facilitates long-run economic growth.

Extension: Growth versus basic needs

In some developing countries, perspectives may differ. There has been a long-running debate about whether society, in its early stages of development, should devote its resources to achieving the growth objective or to catering for basic needs. By making economic growth the prime target of policy, it may be necessary in the short run to allow inequality of incomes to continue. This would provide incentives for entrepreneurs to pursue growth.

With such a 'growth-first' approach, it is argued that eventually, as growth takes place, benefits will trickle down. In other words, growth is seen as necessary to tackle poverty and provide for basic needs. However, others have argued that the first priority should be to deal with basic needs immediately, so that people gain in human capital and become better able to contribute to the growth process.

It is also important to realise that economic growth does not necessarily translate into improvements in living standards across the board. For example, where the benefits from growth are concentrated in certain groups within a society, rather than being spread widely, the majority of the population may see little improvement in their circumstances.

Growth and recession in the early twenty-first century

For industrial countries, the importance of economic growth has been brought into sharp focus through crises. Two critical periods illustrate this particularly well.

The first major crisis was the financial crisis that affected the UK and other economies in the late 2000s. Growth became negative in the second half of 2008 and remained negative for six consecutive quarters. The UK was not the only economy affected by recession at this time – many advanced countries followed a similar pattern. Indeed, countries like Greece were more severely affected during this period.

The Consequences of Recession

When output is falling and firms are reducing their production, they are likely to lay off workers, so unemployment rises. This then leads to falling incomes, which reduce aggregate demand and may lead to further drops in output, prolonging the recession. Looking back at the trend data, it is clear that the time path of real GDP has remained well below what might have been achieved had the recession not occurred.

The second major crisis was the COVID-19 pandemic. When the pandemic struck in early 2020, the impact on real GDP was dramatic. The quarterly percentage change in real GDP fell strongly and quickly, demonstrating the severe economic shock caused by lockdowns and restrictions. Notice that the scale of the impact was very different from that of the financial crisis – the pandemic caused a much sharper, more sudden contraction. However, there was also a rapid bounce-back as the vaccination programme took effect during 2021.

The costs of economic growth

While economic growth brings many benefits, it also imposes costs that must be considered carefully. Perhaps the most obvious costs arise in terms of pollution and degradation of the environment.

In designing long-term policy for economic growth, governments need to be aware of the importance of maintaining a good balance between enabling resources to increase and safeguarding the environment. Pollution reduces the quality of life, so pursuing economic growth without regard to environmental consequences may be damaging. This means that it is important to consider the long-term effects of economic growth, not only for people today but also for future generations.

Environmental degradation

These environmental costs represent examples of externalities. The costs have been highlighted in recent years by growing concerns about global climate change and the pressures on non-renewable resources such as oil and natural gas.

Real-World Impact: China's Rapid Growth and Environmental Concerns

For example, the rapid growth rates being achieved by large emerging economies such as China and India have raised questions about the sustainability of economic growth in the long run. China in particular has experienced a period of unprecedented growth since about 1978. The average growth rate over 5-year periods from 1978 to 2020 was nearly 8% per annum. No other economy in recent history has been able to achieve an average growth rate of almost 8% per annum over such a long period. Notice that even China's growth was affected by the COVID-19 pandemic, with the growth rate falling in the final 5-year period shown.

Economic growth may thus have important effects on the environment. In pursuing growth, countries must bear in mind the need for sustainable development, safeguarding the needs of future generations as well as the needs of the present. In other words, today's generation has a responsibility to safeguard the standard of living of people in the future.

The Definition of Sustainable Development

Sustainable development is defined as 'development that meets the needs of the present without compromising the ability of future generations to meet their own needs' (Brundtland Commission, 1987).

This definition emphasizes the intergenerational responsibility that current societies have to protect environmental resources and maintain the productive capacity of the economy for those who will come after us.

Extension: The environment as a factor of production

One way of viewing the environment is as a factor of production that needs to be used effectively, just like any other factor of production. In other words, each country has a stock of environmental capital that needs to be utilised in the best possible way.

However, if environmental capital is to be used appropriately, it must be given an appropriate value. This can be problematic when property rights are not firmly established. In many developing countries, it is difficult to enforce legislation to protect the environment. Furthermore, if the environment as a factor of production is underpriced, then 'too much' of it will be used by firms.

There are externality effects at work here too. The loss of biodiversity is a global loss, affecting something that impacts the local economy. In some cases, there have been international externality effects of a more direct kind, such as when forest fires in Indonesia caused the airport in Singapore to close down because of the resulting smoke haze.

Trade-offs with other objectives

Economic growth involves opportunity costs and potential conflicts with other important policy objectives.

An important consideration for developing countries concerns the opportunity cost involved in pursuing economic growth. Devoting more resources to investment in capital goods creates an opportunity cost in terms of the consumption that must be sacrificed in the present. For developing countries where consumption today is needed to help alleviate poverty, this represents a significant trade-off. Indeed, poverty levels may increase if economic growth primarily benefits richer members of society, thus increasing inequality in the distribution of income.

There may also be concerns about the desirability of economic growth when it entails structural change in the economy. If economic growth involves workers being displaced from declining sectors, they may find that they do not have the right skills for employment in expanding sectors. In other words, there may be structural unemployment, although hopefully this could prove to be a transitional problem as workers retrain and adapt.

Balance of Payments Effects

Economic growth can also affect the balance of payments. When the marginal propensity to import is high, rising incomes lead to a rapid increase in imports. This can create balance of payments difficulties, particularly if export growth does not keep pace with import growth.

It is also possible that a focus on economic growth could have social effects if people feel stressed or find that leisure time is coming under pressure from longer working hours or more intensive work patterns.

Therefore, although economic growth is important to a society, the drive for growth must be tempered by an awareness of the possible trade-offs with other important objectives. In other words, societies need to balance the possible benefits from economic growth against the associated costs.

Remember!

Key Points to Remember:

-

Economic growth means expanding productive capacity. Potential growth occurs when the economy's ability to produce increases (shown by LRAS shifting right or PPF shifting outward), while actual growth is measured by the percentage change in real GDP.

-

The output gap measures unused capacity. A negative output gap indicates unemployment and spare capacity, while a positive output gap (operating above sustainable capacity) can only be maintained temporarily and creates inflationary pressure.

-

Growth comes from capital, labour, and productivity. Investment increases the capital stock, human capital development improves workforce quality, and productivity gains mean factors of production are used more efficiently. International trade enables specialisation and export-led growth strategies.

-

The business cycle creates fluctuations around trend. Real GDP varies around its long-term trend through phases of recession, trough, recovery, boom, peak, and slowdown. Major crises like the 2008 financial crisis and 2020 pandemic cause sharp deviations from trend.

-

Growth brings benefits but also costs. While growth raises living standards, creates employment, and increases government revenue, it also causes environmental degradation and pollution. Sustainable development requires balancing present needs with the ability of future generations to meet their own needs.