Photo AI

Last Updated Sep 26, 2025

Business Stakeholders Simplified Revision Notes for Leaving Cert Business

Revision notes with simplified explanations to understand Business Stakeholders quickly and effectively.

390+ students studying

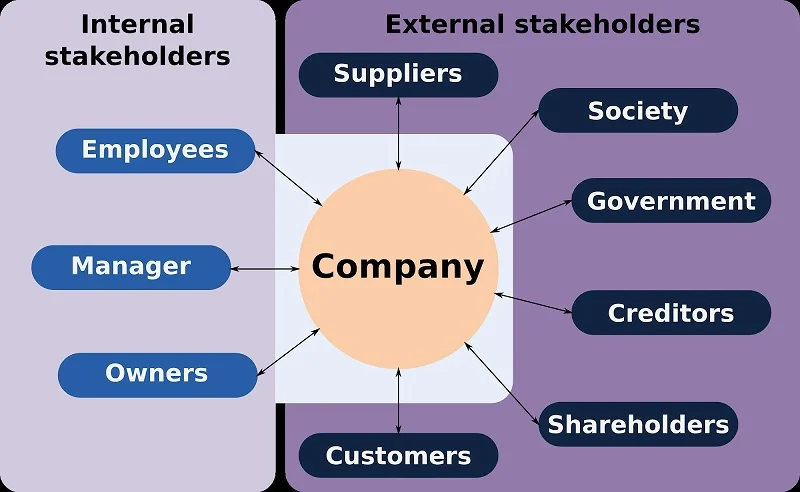

Business Stakeholders

Stakeholders: A stakeholder is any individual or group who has an interest or is affected by the activities and success of a business. They can influence or be influenced by the business's actions, objectives, and policies.

Internal Stakeholders:

- Entrepreneurs: People who take the initiative to set up a business, organise resources (labour, capital, enterprise), and take financial and personal risks in the hope of making a profit.

- Example: Phillip McKenna and Oisin Devoy, the founders of SimpleStudy, developed an education technology business.

- Investors: Individuals or institutions who provide capital to the business (e.g. loans, shares) in exchange for a financial return, such as dividends or interest.

- Example: Enterprise Ireland supports Irish start-ups through equity investment.

- Employees: People who work for the business in exchange for wages or salaries. They contribute their time and effort and expect fair treatment, job security and opportunities for advancement.

- Example: Retail staff at Dunnes Stores who work on shop floors and expect clear employment contracts.

- Managers: Responsible for the day-to-day running of the business. They make decisions to achieve the business's strategic goals, and balance the needs of multiple stakeholders.

External Stakeholders:

- Customers: Individuals or organisations who purchase goods or services. They expect value for money, quality, and good customer service.

- Example: Customers of Ryanair expect low fares and reliable service.

- Suppliers: Provide raw materials or goods for resale. They want prompt payment and long-term contracts.

- Example: Glanbia supplies dairy products to supermarkets across Ireland.

- Government: Regulates businesses through laws and taxation. It also offers grants and supports.

- Example: Revenue Commissioners enforce tax compliance; Local Enterprise Offices offer business support schemes.

- Local Community: The area in which the business operates. The community expects jobs, environmental protection, and ethical behaviour.

- Example: Dairygold is expected to operate responsibly by avoiding pollution and supporting local employment. As a major agri-food business in Ireland, its factories are expected to meet environmental standards and contribute to the local economy through job creation.

- Competitors: Other businesses offering similar goods or services. They want to gain market share and may drive innovation and pricing strategy.

- Example: SuperValu and Tesco are direct competitors in Irish retail.

Conflict and cooperation between stakeholders

Stakeholders can have cooperative or competitive relationships depending on their interests:

- Entrepreneur and Investor (Cooperative): Both want the business to succeed and grow. Investors want a return; entrepreneurs want profit.

- Employer and Employee (Competitive): Employers may want to reduce costs, while employees seek higher wages.

- Producer and Consumer (Cooperative): Producers aim to meet consumer needs to build loyalty and increase sales.

- Entrepreneur and Competitor (Competitive): Competing for market share can lead to innovation but also to conflict.

Interest Groups

An interest group is an organised group of people who work together to promote a common goal by influencing decision-makers such as businesses, government or regulators. They aim to protect or advance the interests of their members through lobbying, negotiation, or public campaigns. Interest groups are not involved in running businesses but try to shape business policy, law, or conditions from the outside.

They can be:

- Voluntary: representing members' interests (e.g. trade unions)

- Institutional: formally recognised in national policy-making (e.g. through social partnership)

Why are interest groups important?

- Interest groups are important because they give individuals, workers, or businesses a collective voice to influence decisions made by government or regulators.

- This is especially valuable in areas such as employment law, environmental policy, consumer protection, and business regulation.

- They help:

- Shape legislation and policy by lobbying ministers and state bodies

- Represent large groups of people or firms that may otherwise go unheard

- Balance the interests of stakeholders, especially in industrial relations

- Raise public awareness through campaigns and protests

Key examples of Irish interest groups

1. Irish Farmers' Association (IFA)

- Represents**:** Irish farmers

- Objective:**** To secure fair prices, supports, and improved working conditions for farmers

- Actions:

- Lobbies the government and EU on issues such as CAP reforms, farm subsidies, and environmental regulations

- Organises protests and campaigns when farmers' livelihoods are threatened

- Impact:

- Influences agricultural and environmental policy

- Pressures supermarkets to ensure fair farmgate prices Example: The IFA actively lobbied in Brussels (i.e. with EU institutions) prior to the abolition of milk quotas in 2015. Their goal was to secure greater flexibility in the lead-up to the quota removal, as Irish dairy farmers were preparing to expand production significantly once the quotas were lifted.

2. IBEC (Irish Business and Employers Confederation)

- Represents: Irish businesses and employers across sectors

- Objective: To influence economic and employment policy to support Irish enterprise

- Actions:

- Negotiates with government and trade unions on wage policy, taxation, and employment regulation

- Advises members on compliance with EU legislation, industrial relations, and business trends

- Impact:

- Helps shape business-friendly legislation

- Opposes excessive regulation or changes seen as damaging to business competitiveness Example: IBEC represented employers during Ireland's Social Partnership era (1987–2009). It participated in national wage negotiations with trade unions and the government, advocating for employer interests on pay, tax, and competitiveness.

3. ICTU (Irish Congress of Trade Unions)

- Represents: Over 40 trade unions and their members

- Objective: To improve workers' rights, pay, and working conditions

- Actions:

- Lobbies the government on employment law (e.g. minimum wage, sick pay, union recognition)

- Participates in industrial relations bodies, representing employees in national discussions

- May coordinate strikes or public campaigns where negotiations fail

- Impact:

- Shapes employment rights legislation

- Balances the power of employers in negotiations Example: ICTU supported the campaign to introduce statutory sick pay in Ireland (introduced in 2023).

Co-operation and conflict between interest groups and businesses

Interest groups do not always agree with businesses:

| Group | Possible Conflict With | Reason |

|---|---|---|

| ICTU | Employers | Workers want better pay; employers want to reduce costs |

| IBEC | Trade unions | Businesses want flexible contracts; unions want secure jobs |

| IFA | Government / Supermarkets | Farmers demand higher prices; retailers resist to keep costs low |

However, co-operation can also benefit both sides:

- IBEC and ICTU have worked together in the past through national wage agreements and social partnership deals. These agreements helped avoid strikes by agreeing on wages and working conditions, giving both employers and workers more certainty and stability in the economy.

- IFA and the government cooperate on issues important to farmers, such as improving rural broadband access through the National Broadband Plan, and supporting farmers with programs that help them export their products abroad. This partnership helps improve farming businesses and rural communities.

500K+ Students Use These Powerful Tools to Master Business Stakeholders For their Leaving Cert Exams.

Enhance your understanding with flashcards, quizzes, and exams—designed to help you grasp key concepts, reinforce learning, and master any topic with confidence!

60 flashcards

Flashcards on Business Stakeholders

Revise key concepts with interactive flashcards.

Try Business Flashcards6 quizzes

Quizzes on Business Stakeholders

Test your knowledge with fun and engaging quizzes.

Try Business Quizzes29 questions

Exam questions on Business Stakeholders

Boost your confidence with real exam questions.

Try Business Questions1 exams created

Exam Builder on Business Stakeholders

Create custom exams across topics for better practice!

Try Business exam builder84 papers

Past Papers on Business Stakeholders

Practice past papers to reinforce exam experience.

Try Business Past PapersOther Revision Notes related to Business Stakeholders you should explore

Discover More Revision Notes Related to Business Stakeholders to Deepen Your Understanding and Improve Your Mastery

96%

114 rated

Introduction to People in Business

Stakeholder Relationships

286+ studying

194KViews96%

114 rated

Introduction to People in Business

Stakeholder Relationships

360+ studying

187KViews