Financial Documents (Grade 10 NSC Matric Mathematical Literacy): Revision Notes

Financial Documents

What are financial documents?

Financial documents are written records that track money transactions in our daily lives. These documents show exactly what was bought, sold, received, or paid during any financial activity.

Financial documents play a crucial role in personal, business, and government finances because they serve multiple important functions. They provide proof of all purchases and payments you make, which is essential when you need to verify transactions later. These documents help you record and monitor your income and expenses, making it easier to understand where your money comes from and where it goes. They also clearly show any money owed or received, helping you keep track of debts and credits. Additionally, financial documents assist with budgeting and tax preparation by providing accurate records of your financial activities. Finally, they serve as evidence during audits or disputes, protecting you in legal or financial disagreements.

Understanding how to read, fill in, and check these documents is an essential life skill that will help you manage your finances effectively throughout your life.

Common types of financial documents

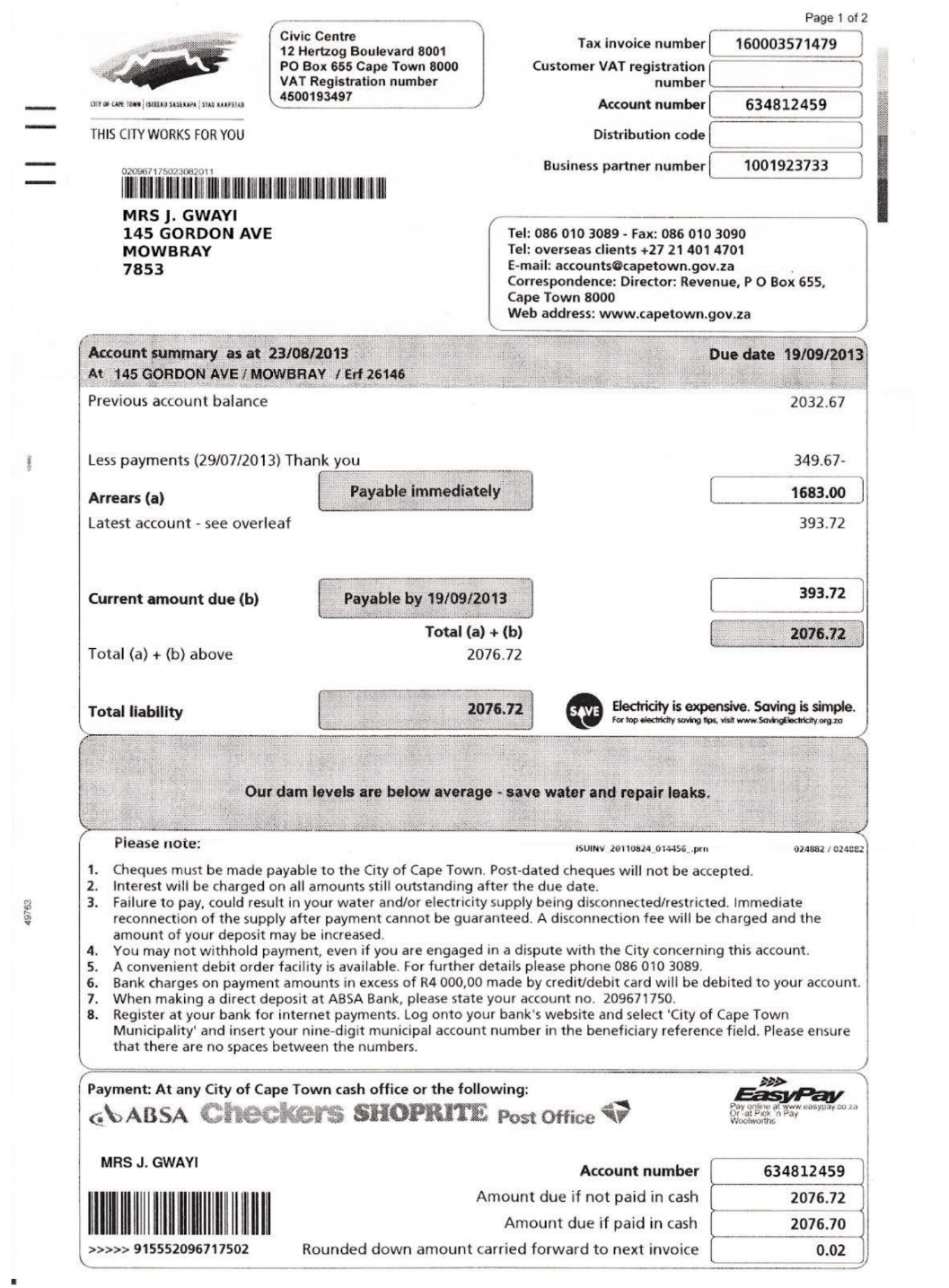

Municipal and other utility bills

In South Africa, most households receive a range of municipal and utility services, including electricity, water, waste removal (rubbish collection), and often telephone or other communication services. These services are provided either by the local municipality or by approved utility providers. Every household is required to pay a monthly charge for these services, and the amount owed usually depends on how much electricity, water, or data/airtime has been used, as well as any fixed service fees that apply.

Utility and municipal bills serve several purposes:

* They show how much of each service was used during the billing period.

* They include meter readings (for water and electricity) or usage summaries (for telephone or data services).

* They list tariffs, service charges, and taxes such as VAT.

* They help households track and manage spending on essential services.

* They act as official proof of residence and payment.

Deposit slip

A deposit slip is used when you want to put money into your bank account. This document ensures that both you and the bank have a record of the money being deposited.

The deposit slip must include several key pieces of information: the account holder's name, account number, date of deposit, branch details, and the amount being deposited (written in both numbers and words). Most deposit slips have separate spaces for cash deposits and cheque deposits, allowing you to specify what type of money you're putting in.

It's crucial that deposit slips are filled out accurately and with clear handwriting to prevent fraud and ensure your money goes into the correct account.

Withdrawal slip

A withdrawal slip is the document you use when taking money out of your bank account. This could be at a bank branch or sometimes at an ATM.

The withdrawal slip must contain your account number, the date of withdrawal, the amount you want to withdraw (in both numbers and words), and your signature. When making a withdrawal, you'll usually need to provide proof of identity to verify that you are the account holder.

This document creates a paper trail showing when and how much money was taken from your account, which is important for your personal record-keeping.

Cheque

A cheque is a written instruction that you give to your bank, telling them to pay a specific amount of money to another person or business. When you write a cheque, you're known as the drawer, and the person receiving the payment is called the payee.

Every cheque must include several key parts to be valid: the drawer's name and signature, the date it was written, the amount to be paid (written in both words and numbers), the payee's name, and the cheque number for tracking purposes.

There are different types of cheques you should understand. A crossed cheque has two parallel lines drawn across it and can only be deposited into a bank account - it cannot be cashed over the counter. An open cheque has no crossing lines and can be cashed immediately at the bank counter.

However, post-dated or unsigned cheques are invalid and cannot be processed by the bank.

Invoice

An invoice is sent by a seller to a buyer requesting payment for goods or services that have been provided. Think of it as a formal request for money that includes all the details of what was purchased.

A proper invoice lists several important pieces of information: details about both the seller and buyer, a clear description of the goods or services provided, the quantity purchased and unit price for each item, the total cost before VAT, the VAT rate and VAT amount, and the final total including VAT.

Invoices are used for record-keeping by both businesses and customers, and they serve as proof that a sale took place.

Receipt

A receipt is given to you when you make a payment. It confirms that the seller has received your money and completes the transaction.

The receipt shows important details including the date of payment, the payer's name, the amount paid, the payment method used (such as cash, EFT, or card), and either the seller's signature or business stamp.

Receipts serve as your proof of payment and should be kept safely in case you need to return items, claim warranties, or verify expenses for tax purposes.

Bank statement

A bank statement is a monthly record provided by your bank that shows all the activity in your account during that period.

The statement lists all deposits, withdrawals, debit orders, bank charges, and your account balances throughout the month. This document helps you check for any errors or unauthorised transactions that might have occurred in your account.

Bank statements are extremely useful for budgeting and tracking your spending patterns, as they provide a complete overview of your financial activity.

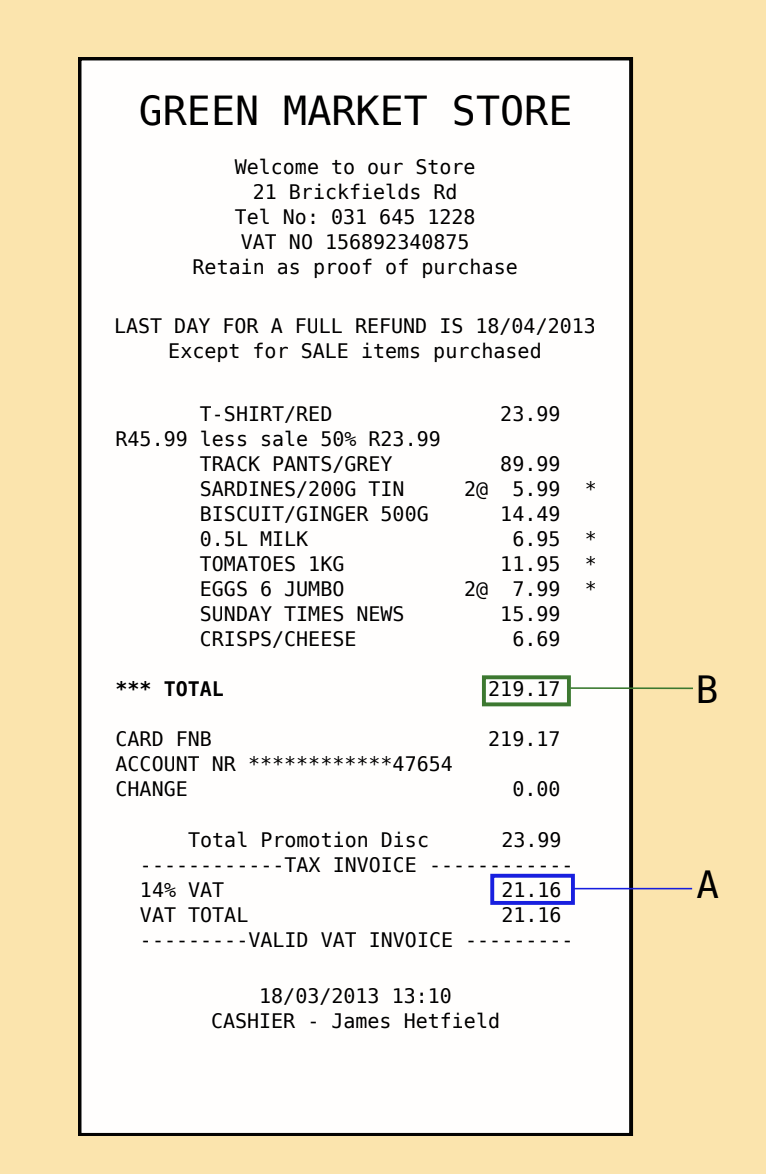

Value added tax (VAT)

VAT is a government tax that is charged on most goods and services in South Africa. The standard VAT rate is 15%, though some basic items like bread, milk, and maize meal are zero-rated, meaning no VAT is charged on them.

Below you can see a till slip with the VAT (A) and the total amount paid (B) highlighted.

VAT calculations

When working with VAT, you need to understand two key formulas:

Worked Example 1: Calculating VAT

If an item costs R200 excluding VAT, let's calculate the VAT amount and total cost:

- VAT Amount = R200 × 0.15 = R30

- Total Cost = R200 + R30 = R230 (including VAT)

Worked Example 2: Finding the original price

If you know the total price including VAT is R230, you can find the original price by dividing by 1.15:

- Original Price = R230 ÷ 1.15 = R200

Worked Example 3: Checking an invoice

An invoice shows:

- Item cost: R150 (excluding VAT)

- VAT: R22.50

- Total: R172.50

Let's verify: VAT = R150 × 0.15 = R22.50 ✓ Total = R150 + R22.50 = R172.50 ✓

Students should practise using these formulas to check invoices and receipts for accuracy.

Reading and completing financial documents

To work effectively with financial documents, you must be able to perform several key tasks.

First, you need to identify key information such as dates, reference numbers, account holder details, and totals on any document you're working with. You should also be able to complete missing details correctly on forms, ensuring all required fields are filled in properly.

Calculating totals, subtotals, VAT, and balances is another essential skill. This involves using the VAT formulas correctly and double-checking your arithmetic. You should also be able to explain the purpose of each part of a document - for example, understanding that an invoice number serves as a tracking reference.

Finally, you need to be able to spot errors in incorrect or incomplete documents, such as missing signatures, wrong dates, or incorrect calculations.

You'll encounter these skills when working with practical examples like electricity and telephone bills, retail shop receipts, sample invoices, and bank statements.

Accuracy and good practice

When working with financial documents, following good practices is essential for avoiding problems and protecting yourself from fraud.

Always write clearly and legibly so that others can read your writing without confusion. Use correct dates, currency symbols (R), and units to avoid misunderstandings about amounts or timing.

Check calculations carefully before signing or submitting any document, as errors can cause significant problems later. Keep copies or photos of important documents for your own records.

Most importantly, never sign blank forms or share banking details carelessly - this prevents fraud and identity theft. Taking these precautions will help you maintain good financial records and protect yourself from potential problems.

Key Points to Remember:

- Financial documents are written proof of all money transactions and are essential for managing personal and business finances effectively.

- Each document type serves a specific purpose: deposit slips for putting money in, withdrawal slips for taking money out, cheques for instructing payments, invoices for requesting payment, receipts for confirming payment, and bank statements for monthly summaries.

- VAT calculations are crucial skills: remember that VAT Amount = Cost × 0.15 and Total Cost = Cost × 1.15, with South Africa's standard VAT rate being 15%.

- Accuracy and clear writing prevent fraud and errors - always double-check calculations, write legibly, and keep copies of important documents.

- These skills are practical life tools that help you budget, track spending, verify transactions, and manage your finances responsibly.