Banking (Grade 11 NSC Matric Economics): Revision Notes

Banking

Bank deposits

Banks accept different types of deposits from customers. These deposits form the foundation of the banking system and allow banks to provide various financial services. Understanding the three main types of deposits helps you grasp how money flows through the banking system.

Demand deposits

Demand deposits are funds placed in current accounts (also known as cheque accounts) or savings accounts. The key feature of these accounts is that you can access your money immediately without giving the bank any advance warning. This makes them highly liquid and convenient for everyday transactions.

Short-term deposits

Short-term deposits are funds that can be withdrawn with 30 days or less notice to the bank. These deposits typically earn slightly higher interest rates than demand deposits because the bank has more certainty about how long they can use the money.

Long-term deposits

Long-term deposits are funds deposited for extended periods of time. Examples include fixed deposits or investment accounts where the money is locked away for months or years. These deposits usually offer the highest interest rates to compensate customers for reduced access to their funds.

The three types of deposits create a trade-off between accessibility and returns: the more immediate your access to funds (demand deposits), the lower the interest earned. Conversely, the longer you commit to keeping funds deposited (long-term deposits), the higher the interest rate offered by the bank.

Credit creation

Credit creation is one of the most important functions of the banking system. It explains how banks can multiply the money supply in the economy through their lending activities.

Understanding credit creation

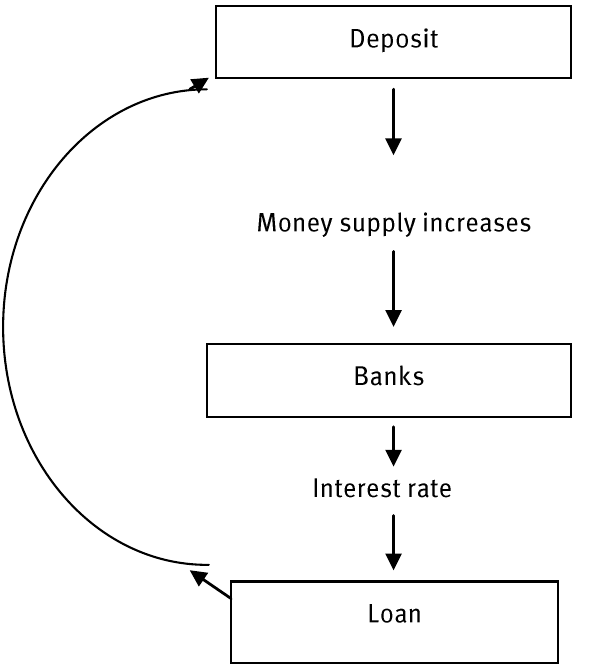

Credit creation occurs when banks expand deposits through lending. This is a fundamental principle of modern banking: banks do not keep all deposited money locked away. Instead, they lend out the majority of deposits to borrowers whilst keeping only a small portion available for customers who want immediate access to their funds.

The tendency of commercial banks to multiply their deposits through lending is called the creation of credit. This process is fundamental to how modern banking systems operate.

How the fractional reserve system works

The banking system as a whole can expand loans many times beyond its actual cash reserves. When a bank provides a loan to an individual or business, the money is not handed over in physical cash. Instead, the bank opens a deposit account in the borrower's name and allows them to draw upon these funds as needed. When the borrower spends this money, it often becomes a deposit at another bank, continuing the cycle.

Practical Example: Fractional Reserve Banking in South Africa

In 2010, the cash reserve requirement in South Africa was 2.5%. This meant:

Step 1: Banks were legally required to keep only 2.5% of deposits as cash reserves

Step 2: Banks could lend out 97.5% of the money deposited with them

Result: For every R100 deposited, banks kept R2.50 in reserve and could lend out R97.50

This system of keeping only a fraction of deposits as reserves is called fractional reserve banking.

Restrictions on credit creation

A bank's ability to create money through credit is not unlimited. Several factors restrict how much credit banks can create:

- The size of the cash reserve - Banks must maintain minimum reserves set by the central bank

- The demand for bank loans - Banks can only lend if people and businesses want to borrow

- Money invested outside the banking system - If people invest in stocks, bonds, or property instead of keeping money in banks, this reduces the amount available for credit creation

- Money held by the public in cash - When people keep cash at home rather than depositing it, banks cannot use these funds for lending

- Investment held in foreign countries - Money sent abroad is removed from the domestic banking system

Money supply and money creation

To measure the total amount of money available in the economy, economists use various money supply measures called M1, M2 and M3. Each measure includes different types of money and accounts, with M1 being the most liquid.

The M1 money supply

M1 represents the most liquid forms of money in the economy. It includes all notes and coins in circulation outside the banking sector, plus all demand deposits held by the domestic private sector with banks.

The M1 money supply is calculated using this formula:

Where:

- = money supply

- = cash (notes and coins in circulation outside banks)

- = demand deposits (money in current and savings accounts)

This formula shows that money supply consists of both physical currency held by the public and bank deposits that can be quickly accessed. The formula is simple but powerful: it captures the two main components of liquid money in the economy.

Interest rates

Interest rates play a crucial role in the banking system and the wider economy. They affect decisions about saving, borrowing, and investing.

What are interest rates?

An interest rate is the percentage charged on borrowed funds over a specific period, typically expressed annually. When you borrow money from a lender, you must pay back the original amount (called the principal) plus interest for the use of that money.

Interest rates serve as a vital tool of monetary policy. The South African Reserve Bank uses interest rate targets to influence important economic variables including investment levels, inflation rates, and unemployment.

Types of interest rates

There are many different types of interest rates in the banking system. Two are particularly important:

Repurchase (repo) rate

The repurchase rate (commonly called the repo rate) is the interest rate at which commercial banks can borrow money from the South African Reserve Bank.

When the Reserve Bank changes the repo rate, it influences all other interest rates in the economy. A higher repo rate makes borrowing more expensive throughout the banking system, whilst a lower repo rate makes borrowing cheaper.

Prime overdraft rate

The prime overdraft rate (often simply called prime) is the lowest rate at which a bank will lend money to its most creditworthy customers.

Banks typically add a percentage onto the prime rate when setting interest rates for other customers, depending on their credit risk.

Factors influencing interest rates

Different factors affect the interest rates that banks charge:

- The market rate - General supply and demand for loans in the economy

- Risk factors - The likelihood that a borrower might fail to repay affects the rate charged

- Length of time of loan - Longer loans typically carry higher interest rates due to increased uncertainty

- Expectations of future interest rates - If people expect rates to rise, current rates may adjust accordingly

Micro-lending

Micro-lending addresses the financial needs of individuals who typically cannot access traditional banking services.

What is micro-lending?

Micro-lending is the practice of providing small loans to people in need. These micro-loans are typically for modest amounts and are commonly used to help individuals start small businesses. Recipients are most often economically disadvantaged people living in urban areas or developing nations who cannot obtain loans from conventional banks.

Regulation in South Africa

In South Africa, micro-lending is regulated by the Micro Finance Regulatory Council (MFRC). This body has three main aims:

- Promote sustainable growth in the micro-lending industry

- Serve the credit needs of those who do not have access to traditional banks

- Protect customer rights and ensure fair treatment

The National Credit Act

In 2008, the National Credit Act came into force in South Africa. This legislation aims to protect borrowers by ensuring they are not charged excessively high interest rates.

The Act also requires that loans are only granted to people who have the financial capacity to service the debt, preventing individuals from falling into unsustainable debt traps.

Remember!

Key Points to Remember:

-

Three types of deposits: Demand deposits (immediate access), short-term deposits (30 days or less notice), and long-term deposits (extended periods) serve different customer needs.

-

Credit creation multiplies money: Banks create money by lending out most deposits whilst keeping only small cash reserves (e.g., 2.5%), allowing the banking system to multiply the money supply.

-

M1 money supply formula: , where money supply equals cash in circulation plus demand deposits.

-

Key interest rates: The repo rate (rate at which banks borrow from SARB) and prime rate (lowest rate for preferred customers) influence all other rates in the economy.

-

Micro-lending serves the disadvantaged: Small loans help those without access to traditional banking, regulated by the MFRC and National Credit Act to protect borrowers from exploitation.