Budgets and Statements of Income and Expenditure (Grade 11 NSC Matric Mathematical Literacy): Revision Notes

Budgets and Statements of Income and Expenditure

What are budgets?

A budget is a financial planning document that shows predicted income and expenditure for a future period. Think of it as a financial forecast that helps organisations plan ahead.

Key features of budgets:

- Show estimated or expected amounts for the future

- Used for planning and setting financial targets

- Help organisations prepare for upcoming expenses and income

- Allow comparison between what was planned and what actually happened

Purpose of budgets:

- Planning tool - helps organisations decide how to spend money wisely

- Control mechanism - provides targets to work towards

- Performance measurement - allows comparison of actual results against plans

What are statements of income and expenditure?

A statement of income and expenditure shows the actual financial results for a period that has already ended. This document records what really happened financially.

Key features of income and expenditure statements:

- Show real amounts that were earned and spent

- Cover past time periods only

- Provide factual financial information

- Used to assess actual business performance

Purpose of statements:

- Historical record - documents what actually occurred financially

- Performance analysis - shows how well the organisation performed

- Decision making - provides data for future planning

Key differences between budgets and statements

| Budgets | Statements of Income and Expenditure |

|---|---|

| Future-focused (predicted amounts) | Past-focused (actual amounts) |

| Used for planning | Used for reporting results |

| Show estimated figures | Show real figures |

| Help set targets | Help measure performance |

The fundamental difference is timing: budgets are about future predictions while statements record past reality. Understanding this distinction is crucial for interpreting financial documents correctly.

Reading and interpreting budget documents

When reading a budget document, you need to understand its structure and components. Look for these key sections:

1. Summary section

- Total income (all money coming in)

- Total expenses (all money going out)

- Net income (profit or loss)

2. Income details

- Breakdown of different income sources

- Shows where money comes from

3. Expense details

- Breakdown of different types of spending

- Shows where money goes

4. Comparison columns

- Previous year's actual results

- Current year's budget (predicted amounts)

- Current year's actual results

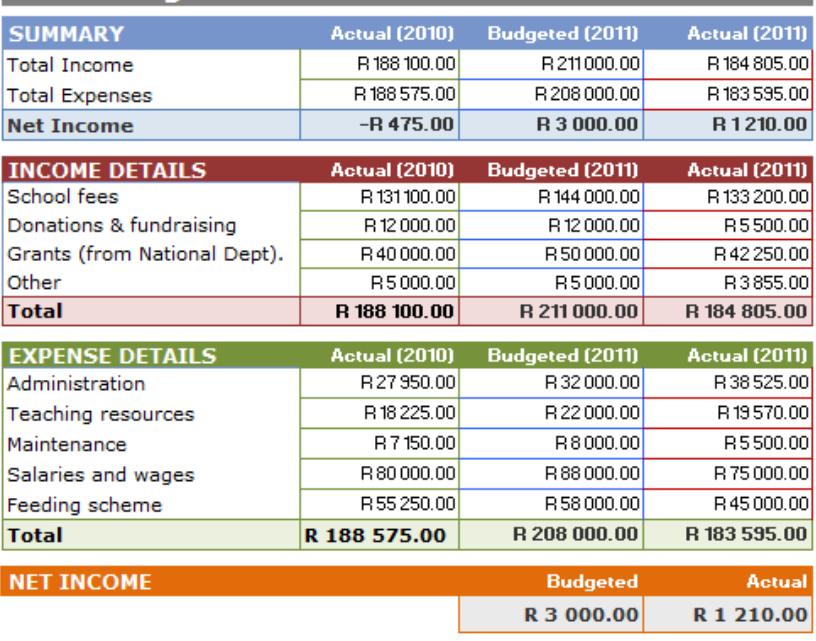

This school budget example shows how organisations compare their financial performance across different time periods. Notice how it includes actual figures for 2010, budgeted amounts for 2011, and actual results for 2011.

Worked Example: Interpreting a School Budget

Looking at the Laddswood Primary School budget:

Income sources include:

- School fees: R133,200 (actual 2011)

- Donations and fundraising: R5,500

- Government grants: R42,250

- Other income: R3,855

Main expenses include:

- Administration costs: R38,525

- Teaching resources: R19,570

- Maintenance: R5,500

- Salaries and wages: R75,000

- Feeding scheme: R45,000

Net income calculation:

- Total income: R184,805

- Total expenses: R183,595

- Net income: R1,210

The budget shows the school made a small profit of R1,210, which was much less than the budgeted profit of R3,000.

Reading and interpreting income and expenditure statements

Income and expenditure statements provide a clear picture of an organisation's financial performance over a specific period. These documents typically show:

1. Time period comparison

- Two or more time periods side by side

- Changes between periods

2. Income section

- All sources of revenue

- Total income figure

3. Operating expenses section

- All business costs

- Detailed breakdown by category

4. Net income

- Final profit or loss figure

- Shows overall financial performance

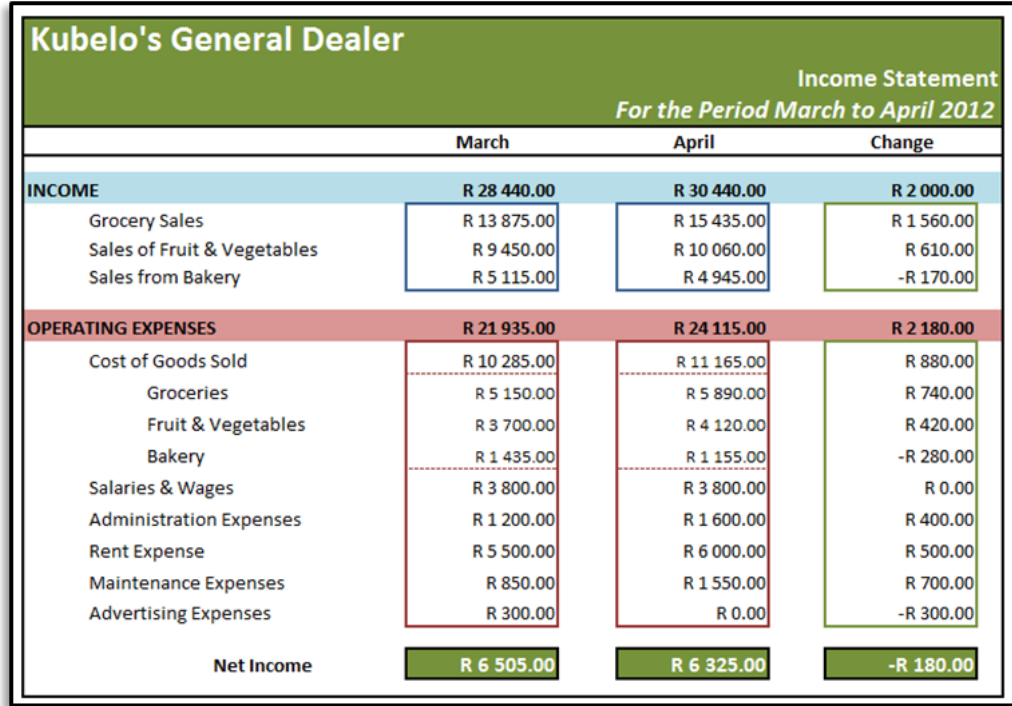

This example shows Kubelo's General Dealer comparing March and April 2012 performance.

Worked Example: Interpreting an Income Statement

From Kubelo's General Dealer statement:

Income analysis:

- March total income: R28,440

- April total income: R30,440

- Change: +R2,000 (improvement)

Income breakdown:

- Grocery sales increased from R13,875 to R15,435

- Fruit and vegetable sales increased from R9,450 to R10,060

- Bakery sales decreased from R5,115 to R4,945

Expense analysis:

- March expenses: R21,935

- April expenses: R24,115

- Change: +R2,180 (increased costs)

Net income results:

- March net income: R6,505

- April net income: R6,325

- Change: -R180 (slight decrease in profit)

Performance interpretation: Although income increased by R2,000, expenses increased by even more (R2,180), resulting in lower profit in April.

Practical tips for exam success

Understanding how to analyse financial documents effectively is essential for academic success. Here are proven strategies to help you excel:

When analysing financial documents:

-

Always calculate net income using:

-

Look for trends - is performance improving or declining over time?

-

Compare actual vs budgeted figures - did the organisation meet its targets?

-

Identify the largest income sources and expense categories

-

Calculate percentage changes to show the significance of differences

Common exam mistakes to avoid:

- Confusing income with expenses

- Not showing calculation steps clearly

- Forgetting to include units (R for Rand amounts)

- Mixing up predicted and actual figures

Key Points to Remember:

- Budgets show predicted future amounts for planning purposes

- Income and expenditure statements show actual past results for performance evaluation

- Net income = Total income - Total expenses

- Always compare figures across time periods to identify trends and performance changes

- Both documents are essential tools for financial management and decision-making