Loans (Grade 12 NSC Matric Mathematical Literacy): Revision Notes

Loans

What are loans?

Loans are financial arrangements where people borrow money when they need it most. The key principle is that borrowers must pay interest on the borrowed amount, making the total repayment more than the original loan.

When you take out a loan, you agree to repay the borrowed money plus additional costs over a specified period through regular monthly payments.

The fundamental concept of lending is that money has a time value - lenders charge interest because they are giving up the use of their money for a period of time, and borrowers pay this cost for immediate access to funds they don't currently have.

Components of loan payments

Understanding what makes up your loan payments is crucial for making informed financial decisions. Each payment you make consists of several components that together determine your total loan cost.

Monthly instalment

A monthly instalment is the amount you pay each month towards your loan. This payment typically includes both repayment of the borrowed amount and interest charges.

Loan fees

Additional Loan Costs

Loans come with additional fees that increase the total cost beyond just the borrowed amount and interest:

- Initiation fee: This is a one-time charge by the lender to process your loan application, payable when the loan is approved

- Monthly administration fee: An additional monthly cost added to your monthly instalment for administrative services

Premium charges

Some loans include optional services such as a monthly premium for personal protection plans, which provide insurance coverage for the loan.

How loan terms affect costs

The length of your loan repayment period significantly impacts both your monthly payments and total loan cost.

This table demonstrates a key principle that all borrowers should understand:

Key Loan Principle: Longer repayment periods result in lower monthly payments. For example, a R16,000 loan costs R864 per month over 24 months, but only R470 per month over 60 months.

However, this lower monthly payment comes at the cost of paying significantly more in total interest over the life of the loan.

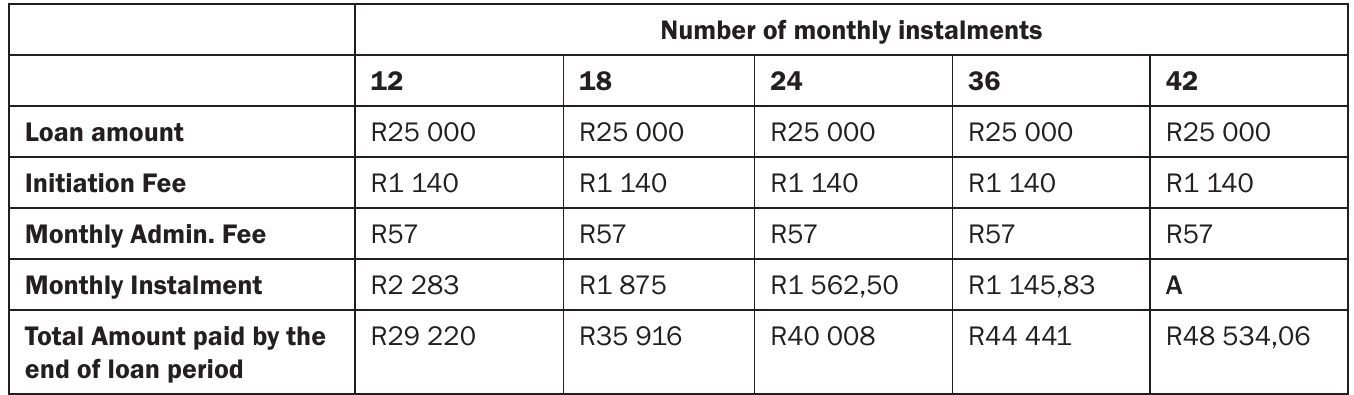

Detailed loan comparison

When comparing loan options, you need to consider multiple factors beyond just the monthly payment. The relationship between loan term and total cost is crucial for making informed financial decisions.

This comparison shows how different loan terms affect the total cost. Notice that:

- Shorter loans have higher monthly payments but lower total costs

- Longer loans have lower monthly payments but significantly higher total costs

Total loan cost formula

The total amount to be repaid can be calculated using:

Worked examples

Worked Example 1: Basic loan calculation

If someone borrows R16,000 and chooses different repayment terms:

24-month option:

- Monthly payment: R864

- Total paid: 24 × R864 = R20,736

60-month option:

- Monthly payment: R470

- Total paid: 60 × R470 = R28,200

Analysis: The shorter loan saves R7,464 in total costs, demonstrating that borrowing for a shorter time involves less interest.

Worked Example 2: Comprehensive loan analysis

For a R25,000 loan over 42 months:

Step 1: Calculate missing monthly instalment (A):

- Total paid = R48,534.06

- Subtract initiation fee: R48,534.06 - R1,140 = R47,394.06

- Divide by number of months: R47,394.06 ÷ 42 = R1,128.43

- Subtract admin fee: R1,128.43 - R57 = R1,071.43

Step 2: Total loan cost: R48,534.06

Step 3: For instalment sale at 33% interest:

- Deposit (10%): R25,000 × 0.10 = R2,500

- Balance: R25,000 - R2,500 = R22,500

- Interest: R22,500 × 0.33 × 2 = R14,850

- Monthly payment: R37,350 ÷ 24 = R1,556.25

Worked Example 3: Comparing payment methods

When deciding between a loan and instalment sale:

- Loan total cost: R48,534.06

- Instalment sale cost: R2,500 + (24 × R1,556.25) = R39,850

Conclusion: The instalment sale costs less in total, making it the better financial choice.

Exam tips for loan problems

Essential Exam Strategies

- Always identify all costs: Look for initiation fees, admin fees, and interest rates

- Use the correct formula: Remember the total cost formula and apply it systematically

- Compare total costs, not just monthly payments: A lower monthly payment often means higher total cost

- Show your working clearly: Break down calculations into logical steps

- Check your answers: Ensure monthly payments × number of months + fees = total cost

Decision-making factors

When choosing between loan options, you need to evaluate multiple criteria to make the best financial decision for your situation. Consider:

- Monthly affordability: Can you comfortably make the monthly payments without straining your budget?

- Total cost: Which option costs less overall when all fees and interest are included?

- Loan term: Do you prefer to be debt-free sooner or have lower monthly payments?

- Additional benefits: Does the loan include useful services like insurance coverage?

Financial Planning Tip

Always consider your long-term financial goals when choosing loan terms. While lower monthly payments might seem attractive, paying less interest overall by choosing shorter terms can free up money for other financial priorities like savings and investments.

Key Points to Remember:

- Loans cost more than the borrowed amount due to interest and fees

- Shorter loan terms mean higher monthly payments but lower total costs

- Always calculate the total amount you'll repay, not just the monthly instalment

- Compare all options carefully - the cheapest monthly payment isn't always the best deal

- Use the formula: