Analysing Investment and Loan Options (Grade 12 NSC Matric Mathematics): Revision Notes

Analysing Investment and Loan Options

When making financial decisions, you need to carefully compare different loan and investment options to determine which choice offers the best value for your situation. This involves calculating monthly payments, total amounts paid, and interest costs to make informed decisions.

Financial decision-making requires careful analysis of multiple factors including payment amounts, time periods, and total costs. Always calculate the complete picture before making commitments.

Understanding loan repayment periods

The length of time you take to repay a loan significantly affects both your monthly payments and the total amount of interest you'll pay. Shorter loan periods result in higher monthly payments but lower total interest costs, while longer loan periods reduce monthly payments but increase the total interest paid over time.

Key loan formula

The monthly payment formula for loans is essential for comparing different borrowing options:

Monthly Payment Formula:

Where:

- = monthly payment amount

- = principal loan amount

- = monthly interest rate (annual rate ÷ 12)

- = total number of payments (years × 12)

Worked example: comparing loan repayment periods

Worked Example: Home Loan Repayment Comparison

Scenario: A couple takes out a home loan of R 2,600,000 with a 10% annual interest rate compounded monthly.

30-year repayment period calculation

Step 1: Identify the variables

- months

Step 2: Calculate monthly payment

Step 3: Calculate total amounts

- Total amount paid =

- Total interest =

20-year repayment period calculation

Step 1: Adjust the time period

- months

- Other variables remain the same

Step 2: Calculate monthly payment

Step 3: Calculate total amounts

- Total amount paid =

- Total interest =

Comparing the options

- Monthly payment difference: R 25,090.56 - R 22,816.86 = R 2,273.70

- Total interest difference: R 5,614,069.60 - R 3,421,734.40 = R 2,192,335.20 saved

By paying an additional R 2,273.70 each month over the shorter period, the borrowers save over R 2 million in total interest payments.

Analysing investment opportunities

When comparing investment options, you must calculate three key values for each option to make informed decisions: Future value (F), Total amount paid (T), and Total interest earned (I).

Investment analysis requires systematic comparison using standardised calculations. Never rely on promotional materials alone - always verify the numbers yourself.

Investment comparison formula

The future value formula for regular payments is:

Where:

- = future value of all payments

- = monthly payment amount

- = monthly interest rate

- = total number of payments

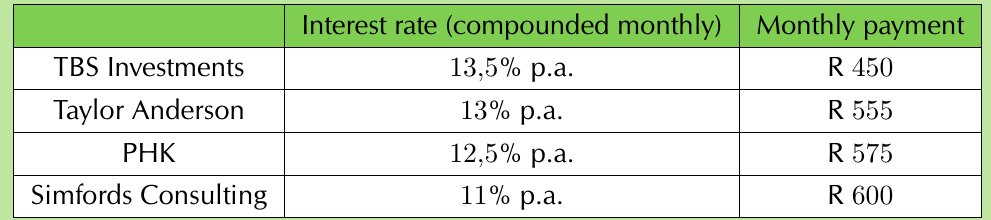

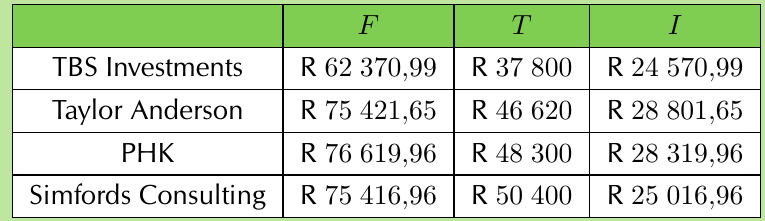

Worked example: investment option analysis

Worked Example: Investment Firm Comparison

Scenario: An investor can afford to invest between R 400 and R 600 monthly for 7 years and wants to compare four investment firms.

Calculation approach for each option

Step 1: Calculate future value using the formula:

Step 2: Calculate total amount paid = monthly payment × number of months

Step 3: Calculate total interest = future value - total amount paid

Investment comparison results

Analysis: While PHK provides the highest future value (R 76,619.96), Taylor Anderson offers the highest interest return (R 28,801.65), making it the better investment option for maximising returns.

Analysing loan options

When comparing loan offers from different institutions, you need to systematically evaluate the monthly payment amount, total amount paid, and total interest charged to identify the most cost-effective option.

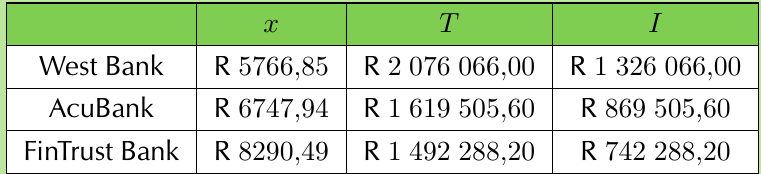

Worked Example: Bank Loan Comparison

Scenario: A borrower needs R 750,000 and can afford monthly payments between R 5,500 and R 7,000. Three banks offer different terms.

Bank comparison results

Key insight: FinTrust Bank offers the lowest total interest but highest monthly payments. If the borrower can afford the higher payments, this option saves significant money long-term.

Understanding credit ratings

A credit rating estimates your ability to fulfil financial commitments based on your payment history. This rating affects your access to future loans and the interest rates you'll be offered.

Credit Rating Impact

Defaulting on loans negatively affects your credit rating and reduces your chances of obtaining future loans. When taking out loans, ensure the monthly payment amount is manageable within your budget.

Always maintain a good credit rating by:

- Making payments on time consistently

- Only borrowing what you can afford to repay

- Keeping debt levels reasonable relative to your income

Pyramid schemes awareness

Pyramid schemes are illegal investment scams that promise unusually high returns with no risk. These schemes are designed to collapse when they can no longer recruit new members, causing most investors to lose their money.

Warning: Pyramid Scheme Characteristics

Be alert for these red flags:

- Promise of quick, high returns with little risk

- Require recruiting new members to generate returns

- Focus on recruitment rather than legitimate business activities

- Money flows upward to early investors from new recruits

- Eventually collapse when recruitment slows

Protection strategies:

- Only invest with registered financial institutions

- Be suspicious of "too good to be true" investment offers

- Verify that investment companies are regulated and supervised

- Never hand over money to unregistered individuals or groups

Key formulas summary

Understanding these essential formulas enables you to make informed financial decisions:

Essential Financial Formulas

Monthly loan payment:

Future value of regular payments:

Present value of payment series:

Interest calculation:

Key Points to Remember:

- Shorter loan periods mean higher monthly payments but significantly lower total interest costs

- When comparing investments, calculate the future value (F), total paid (T), and interest earned (I) for each option

- Always verify that financial institutions are registered and regulated before investing

- Pyramid schemes are illegal and will eventually collapse - avoid investments that seem too good to be true

- Maintain a good credit rating by making payments on time and only borrowing what you can afford to repay