Influence of Government (HSC SSCE Business Studies): Revision Notes

Influence of Government

Introduction

Government plays a crucial role in shaping how businesses manage their finances. This influence occurs through economic policies (monetary and fiscal policy), legislation, and regulatory bodies that monitor and enforce compliance. Understanding these governmental influences is essential for effective financial management decision-making.

The two key governmental influences on business financial management in Australia are:

- The Australian Securities and Investments Commission (ASIC) - regulatory oversight

- Company taxation policy - fiscal impact on profits

The Australian Securities and Investments Commission (ASIC)

What is ASIC?

ASIC is an independent statutory commission that reports to the Commonwealth Parliament. It serves as Australia's corporate regulator, enforcing and administering the Corporations Act 2001.

ASIC's role and responsibilities

ASIC protects consumers and ensures fair practice across multiple financial sectors, covering four key areas of the financial services industry:

- Investments – regulates investment products and financial markets

- Life and general insurance – ensures insurers comply with regulations

- Superannuation – oversees retirement savings providers

- Banking – monitors banking activities (excluding lending)

The primary aim of ASIC is to reduce fraud and unfair practices in financial markets and products. This protects both businesses and consumers from misconduct and maintains the integrity of Australia's financial system.

Key functions of ASIC

ASIC performs three critical functions that directly impact business financial management:

Ensuring legal compliance: ASIC monitors businesses to ensure they follow corporate law. Companies must adhere to strict financial reporting standards, ensuring that financial information is accurate, complete, and presented in accordance with accounting standards.

Information collection and disclosure: ASIC collects financial information from companies and makes it publicly available. This includes the financial statements companies must disclose in their annual reports, promoting transparency and accountability. This public disclosure helps investors, creditors, and other stakeholders make informed decisions.

Public protection: By enforcing regulations, ASIC helps maintain trust in Australia's financial system and protects stakeholders from corporate misconduct, creating a safer environment for investment and commerce.

ASIC's enforcement powers

When businesses breach the Corporations Act, ASIC has extensive powers to investigate and impose remedies. The commission acts as both investigator and enforcer, with the ability to take legal action against companies and individuals who fail to comply with corporate law. The severity of the penalty depends on the seriousness of the misconduct:

- Imprisonment – for serious breaches involving fraud or deliberate misconduct

- Monetary penalties – fines proportionate to the violation

- Negative publicity – non-compliance damages a business's reputation, affecting investor confidence and customer trust

These enforcement mechanisms act as both punishment and deterrent, encouraging businesses to maintain high standards of financial management and corporate governance. The threat of penalties motivates companies to invest in proper compliance systems and internal controls.

ASIC and insolvency regulation

ASIC regulates companies facing financial distress, ensuring that insolvent companies are managed appropriately and creditors' interests are protected. During the COVID-19 pandemic, the federal government amended the Corporations Act 2001 to provide temporary relief for struggling businesses. These changes included:

- Increasing the minimum debt threshold for statutory demands from ``20,000

- Raising the bankruptcy notice threshold from ``20,000

- Protecting directors from personal liability under insolvent trading rules, provided they act within the law

These measures gave businesses breathing room during economic uncertainty, demonstrating how government regulation can adapt to support businesses during crises. This flexibility shows that regulatory frameworks can be responsive to changing economic conditions while still maintaining essential protections.

Company taxation

Understanding company tax

All incorporated Australian businesses – both private and public companies – must pay company tax on their profits. Company tax represents a significant cost for businesses and directly impacts the amount of profit available for distribution to shareholders or reinvestment in the business.

Unlike personal income tax, which uses a progressive scale where higher earners pay higher rates, company tax is levied at a flat rate regardless of profit size. This means a company earning ``100 million (assuming both meet the same turnover threshold).

Company tax is paid before profits are distributed to shareholders as dividends, directly affecting the amount of profit available for reinvestment or distribution. This is sometimes referred to as "pre-dividend taxation."

Current tax rates

Prior to 2017, all companies paid company tax at a rate of 30%. However, in 2016, the government introduced a lower rate for eligible businesses to encourage growth and competitiveness among smaller enterprises:

Current Company Tax Rates:

| Company turnover | Tax rate |

|---|---|

| Under $50 million | 27.5% |

| $50 million or more | 30% |

Eligibility criteria: To qualify for the lower 27.5% rate, a company must have an annual turnover of less than $50 million.

Important note: The government originally planned to reduce the rate further to 26% in 2020-21 and 25% in 2021-22, but these plans were abandoned due to budget concerns and political opposition.

Historical context

The Australian company tax rate has gradually decreased over time, reflecting both domestic policy priorities and international competitive pressures:

- 2000-01: Reduced from 36% to 34%

- 2001-02: Further reduced to 30%

- 2016: Introduced 27.5% rate for eligible businesses

This trend reflects a broader global movement toward more competitive corporate tax rates, as countries compete to attract and retain business investment.

Purpose of tax reform

The Australian government reformed the company tax system to achieve several interconnected objectives that support long-term economic prosperity:

Improving international competitiveness: Lower tax rates make Australia more attractive compared to other countries, encouraging both domestic and foreign investment. When companies compare operating costs across different countries, the tax rate is a significant factor in their decision-making process.

Attracting investment: Competitive tax rates help Australia compete for global capital, as investors consider tax burden when deciding where to establish or expand businesses. A lower tax rate can be the deciding factor that brings major projects and headquarters to Australia.

Driving economic growth: By reducing the tax burden on businesses, more profit is available for reinvestment, expansion, and innovation. This creates a positive cycle of growth where today's tax savings become tomorrow's new jobs and increased productivity.

Job creation and wage growth: When businesses invest and expand, they create more employment opportunities and can afford to offer higher wages, benefiting the broader economy. Research suggests that over the long term, workers benefit from corporate tax cuts through higher wages and more job opportunities.

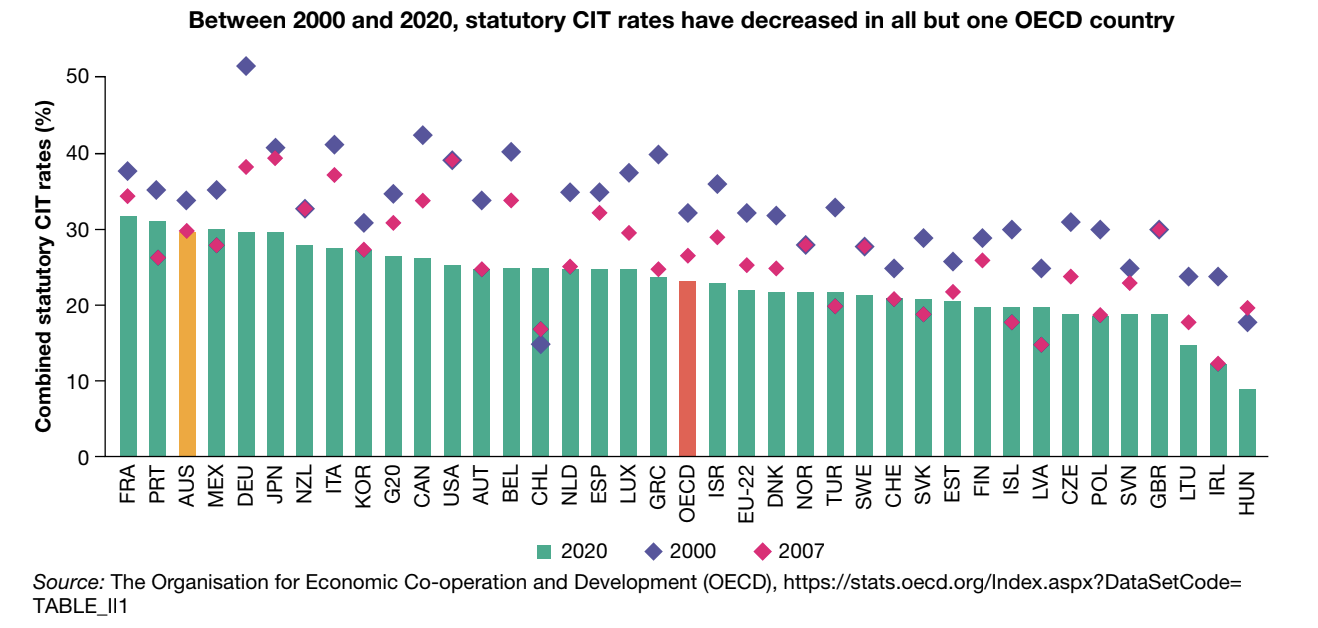

International comparison

Understanding Australia's position in the global tax landscape is crucial for appreciating the rationale behind tax reform efforts. Research by the Organisation for Economic Co-operation and Development (OECD) in July 2020 revealed significant global trends.

Key Global Tax Trends:

- Between 2000 and 2020, the average global company tax rate fell from 30.8% to 23.1%

- Statutory corporate income tax rates decreased in all but one OECD country during this period

- Australia's effective marginal tax rate for businesses was found to be the highest among wealthy OECD nations

This international context highlights why the Australian government considers company tax reform important – to remain competitive with other developed economies and attract global investment. Without reform, Australia risks losing investment to countries with more favorable tax environments.

Exam focus: Analysing the impact of company taxation

When answering exam questions about company taxation, a comprehensive analysis should consider multiple perspectives and dimensions of impact:

Financial implications:

- Lower tax rates increase retained profits available for reinvestment

- Businesses with turnover under $50 million save 2.5% on tax

- More after-tax profit can be distributed as dividends to shareholders

Strategic implications:

- Tax rates influence business location decisions and expansion plans

- Companies may restructure to optimise tax position

- International competitiveness affects long-term viability and market positioning

Stakeholder impacts:

- Shareholders: Higher dividends or company value growth through increased retained earnings

- Employees: Potential for wage increases and improved job security through business growth

- Government: Reduced tax revenue in short term, but potentially increased revenue from economic growth and expanded tax base

- Community: More employment opportunities and economic activity, leading to improved living standards

Worked Example: Calculating Tax Savings

Consider a company with an annual turnover of ``5 million:

Step 1: Determine the applicable tax rate

- Turnover is under $50 million → qualifies for 27.5% rate

Step 2: Calculate tax under current system

- Tax payable = ``1,375,000

Step 3: Compare with previous 30% rate

- Old tax = ``1,500,000

- Tax saving = ``1,375,000 = $125,000

This $125,000 saving represents additional profit available for reinvestment or dividend distribution.

Remember!

Key Points to Remember:

- ASIC is Australia's independent corporate regulator, enforcing the Corporations Act 2001 to protect consumers and reduce fraud in financial markets

- ASIC has extensive powers including imprisonment, monetary penalties, and can create damaging publicity for non-compliant businesses

- Company tax is a flat rate tax on business profits – currently 27.5% for companies with turnover under $50 million and 30% for larger companies

- Company tax reform aims to improve Australia's international competitiveness, attract investment, and drive economic growth

- Both ASIC regulation and taxation policy directly influence business financial management decisions and must be carefully considered in strategic planning

Key Terms:

- ASIC – Australian Securities and Investments Commission

- Corporations Act 2001 – Primary legislation governing companies in Australia

- Company tax – Flat rate tax on incorporated business profits

- Incorporated – Legally registered as a company (private or public)

- Flat rate – Single tax percentage regardless of profit size

- Turnover – Total business revenue

- Insolvency – When a business cannot pay its debts

Critical Framework: Government influences financial management through:

- Regulation (ASIC enforcement)

- Taxation (company tax policy)

- Economic policy (supporting business during crises)