The Impact of International Protection Levels on Australia (HSC SSCE Economics): Revision Notes

The Impact of International Protection Levels on Australia

Introduction

International protection policies affect Australia's economy in significant ways. When foreign governments impose tariffs on Australian exports, these goods become less competitive in overseas markets. Similarly, when other countries subsidise their own exports, they increase global supply and reduce prices, disadvantaging Australian producers selling similar products on world markets.

Overall, international protectionism reduces Australia's national output and income. Conversely, reducing global protection levels should increase Australia's economic performance.

Research by the Centre for International Economics (2018) estimated that a global tariff reduction lowering import prices by 10% would boost Australia's real GDP by 0.6% annually. This demonstrates the significant economic cost of international protectionism to Australia.

As a relatively small economy with substantial agricultural trade, Australia faces particular disadvantages from foreign protectionist policies. Different sectors of the Australian economy experience varying levels of international protection.

Impact on the agricultural sector

Agricultural subsidies in developed economies

Australia's agricultural exporters face significant competitive disadvantages due to heavy subsidies provided by governments in developed countries. The European Union has maintained substantial agricultural support for decades through the Common Agricultural Policy (CAP), which:

- Absorbs over one-third of the EU's total budget

- Provides around one-fifth of European farmers' incomes

- Creates an uneven playing field for unsubsidised Australian producers

Beyond Europe, farmers receive significant government support in the United States, Japan, South Korea and Switzerland. Australian agricultural producers therefore compete in global markets at a structural disadvantage compared with their counterparts in most industrialized nations.

Competitive Disadvantage for Australian Farmers

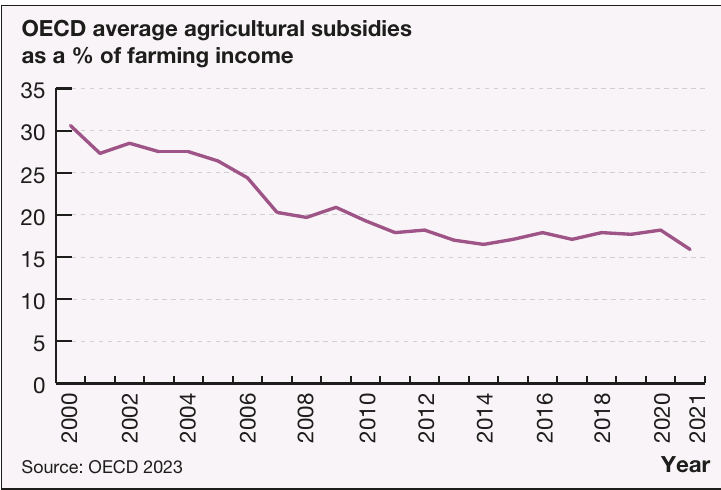

While farmers in developed economies receive substantial government subsidies (representing 17-18% of farm incomes across OECD countries), Australian agricultural producers receive minimal government assistance. This creates a fundamental structural disadvantage in global markets, where Australian farmers must compete on price and quality against subsidised foreign producers.

The graph shows that while agricultural protection levels have declined from around 31% of farm incomes in 2000 to approximately 17-18% in recent years, subsidies still make a significant contribution to farm incomes across OECD countries. This ongoing support continues to disadvantage Australian agricultural exporters who receive minimal government assistance.

Impact from major trading partners

Protection levels in Australia's major export markets also create substantial challenges. China's punitive tariffs imposed in late 2020 demonstrate the significant domestic impact of foreign trade barriers.

China Wine Tariff Impact: A Case Study

Before COVID-19, Australian wine exports to China were valued at $1.3 billion annually. After China imposed punitive tariffs in late 2020, these exports collapsed to just $12.4 million in 2023 — a reduction of over 99%.

This dramatic decline forced Australian wine producers to:

- Rapidly divert exports to alternative markets

- Accept significant adjustment costs

- Absorb substantial lost revenue

This example demonstrates how quickly foreign trade barriers can devastate an export industry.

Slow progress in reducing agricultural protection

Global progress toward reducing agricultural protection has been limited in recent years. This reflects two key trends:

- A general increase in tariffs and protectionist measures worldwide

- Agriculture remaining more heavily protected than other industries despite decades of trade liberalization

Many countries with highly protectionist agricultural policies have exploited complex loopholes in WTO regulations to avoid genuinely opening their agricultural markets. According to the Australian Bureau of Agricultural and Resource Economics and Sciences (ABARES), global agricultural subsidies and trade barriers currently reduce Australian agricultural exports by between $8 billion and $10 billion per year.

Agricultural protection and carbon emissions

An emerging dimension of agricultural protection concerns carbon emissions policy. The European Union is introducing carbon border adjustments (CBAs) from 2026, which will impose import taxes on emission-intensive goods from countries that do not adequately charge producers for carbon emissions through domestic carbon taxes or emissions trading schemes.

These CBAs work similarly to traditional tariffs. Because the EU imposes carbon prices on its own producers, its businesses may face competitive disadvantages compared with firms in countries like Australia that lack comprehensive carbon pricing. CBAs can create incentives for Australian firms to reduce emissions.

The Double-Edged Sword of Agricultural Subsidies

ABARES has highlighted that removing global agricultural subsidies would actually help reduce emissions by:

- Eliminating production distortions

- Improving productivity

- Reducing waste

This would maintain global food security while simultaneously addressing environmental concerns — demonstrating that protectionist policies can have unintended negative consequences beyond their economic impact.

Impact on non-agricultural goods

Mining and resources sector

Australian firms exporting mining and resource products face very few barriers to trade. This sector, which contributes the largest share of Australia's total exports, benefits from several factors:

High global demand: Products such as coal, natural gas, oil and iron ore are in consistently high demand worldwide.

Limited domestic alternatives: Countries importing Australian resources often lack their own deposits of these materials. They cannot develop domestic alternatives simply by imposing protection.

Cost implications: If foreign governments imposed tariffs on Australian resource exports, they would merely increase costs for their own consumers and businesses without encouraging domestic production of resources that do not exist.

An Ironic Twist

Mining companies and gas producers are more likely to face export restrictions from the Australian Government attempting to secure domestic energy supplies than from foreign governments trying to protect their own resources industries. This highlights how the same economic principles that prevent foreign protection can also motivate domestic restrictions.

Manufacturing industries

Australian manufacturing exporters generally face fewer barriers to trade due to substantial reductions in industrial tariffs negotiated through multilateral and bilateral trade agreements in recent decades. Most industrialized economies worldwide now maintain low manufacturing tariffs, and average manufacturing tariffs across the Asia-Pacific region are also relatively low.

However, exceptions exist. Motor vehicles, for example, face tariffs of around 15% in China. Additionally, some Australian exporters argue that non-tariff barriers to trade play an increasingly important role in creating obstacles to market access.

Non-tariff barriers include:

- Technical restrictions and standards

- Licensing requirements

- Inconsistent or varying health regulations across different regions within a country

The Rise of Non-Tariff Barriers

As traditional tariffs have declined through trade agreements, non-tariff barriers have become increasingly significant obstacles for Australian exporters. For example, inconsistent health regulations for processed food products in different areas of a country can make it extremely difficult for Australian exporters to penetrate foreign markets.

These technical barriers to trade are now formally addressed in WTO negotiations and bilateral trade agreements, reflecting their growing importance.

Impact on service industries

The challenge of services trade

Australia's service industries account for approximately 70% of the domestic economy but less than one-fifth of total exports. Service businesses arguably face the most prohibitive barriers to international trade.

The Services Trade Paradox

Despite representing 70% of Australia's economy, services account for less than 20% of exports. This dramatic imbalance reflects the unique challenges facing services trade — both natural barriers and deliberate protectionist policies severely limit the ability of Australian service providers to compete in global markets.

Natural barriers vs protectionist barriers

Trade in services faces two distinct types of barriers:

Natural barriers arise from:

- Geography and transport costs

- Language and cultural differences

- Local tastes and preferences

For example, Australian restaurants might produce exceptional food, but the market for restaurant customers is limited to people either living in or visiting Australia. This makes it difficult for restaurateurs to export their services (except to tourists, who represent a very small proportion of the global consumer market).

Protectionist barriers result from deliberate government policies designed to restrict foreign competition in service industries. Unlike goods, the main barriers to services trade are not tariffs but various government regulations and practices.

Common protectionist barriers

Many countries protect their service industries through multiple mechanisms:

Banking and financial services: Restrictions on granting licences to overseas-owned banks limit the growth of Australia's competitive financial services industry in foreign markets.

Utilities and infrastructure: Competitive Australian firms in electricity, recycling and communications face overseas markets dominated by monopoly government providers or procurement arrangements favouring local suppliers.

Professional services: Licensing laws that only recognize domestic educational qualifications prevent Australian professionals from practicing in foreign markets.

Construction and transport: Government procurement rules mandating local suppliers and restrictions on flight routes limit market access for Australian businesses.

Economic impact of services trade barriers

The Productivity Commission reported in 2015 that international barriers to Australian services trade remain costly, particularly restrictions on establishing commercial operations in key Asian markets. Financial services face especially significant barriers.

Reducing these trade barriers has become a primary objective of Australia's trade agreements with countries such as Japan and South Korea. However, progress remains slower than for goods trade, partly because services protection is more complex and less transparent than tariff protection.

Case study: The Australian Domestic Gas Security Mechanism

While most trade restrictions are imposed on imports, governments sometimes restrict exports when they determine markets are not operating in the national interest. Natural gas provides an important example.

The Australian Domestic Gas Security Mechanism (ADGSM)

Most gas-exporting countries apply some form of gas reservation policy or similar mechanism to protect their national interest in supplying domestic energy markets. Although Australia is the world's largest supplier of liquefied natural gas (LNG), it historically lacked a national policy to guarantee domestic supplies. Only Western Australia had a state-based law requiring 15% of gas production be made available for domestic use.

The Problem: In 2017, energy retailers and manufacturers argued that Australia's LNG industry had committed all its output to long-term overseas contracts at the expense of the domestic market, creating potential supply shortages.

The Solution: The Federal Government introduced the ADGSM to restrict LNG exports during gas supply shortages on Australia's east coast.

2023 Reforms: The mechanism was strengthened by:

- Enabling quarterly activation ahead of peak seasonal demand

- Introducing protections for long-term gas contracts

- Creating shared responsibility for LNG exporters in preventing shortfalls

- Extending the mechanism to 2030

Key Insight: This case demonstrates that Australia itself sometimes employs protectionist measures, not to shield industries from import competition but to ensure adequate domestic supply of critical resources.

Summary

Key Points to Remember:

-

International protection harms Australia: Foreign tariffs and subsidies reduce Australian export competitiveness and national income. A 10% global tariff reduction could boost Australia's GDP by 0.6% annually.

-

Agriculture faces the greatest disadvantage: Heavy subsidies in developed economies (especially the EU's Common Agricultural Policy) cost Australia $8-10 billion in lost agricultural exports each year. OECD agricultural subsidies still provide 17-18% of farm incomes.

-

Mining faces minimal barriers: Australia's resources sector experiences few trade restrictions because products are in high global demand and importing countries often lack domestic alternatives.

-

Services face the most prohibitive barriers: Despite representing 70% of Australia's economy, services account for less than 20% of exports. Government regulations restricting foreign banks, utilities, and professional services create significant obstacles. Natural barriers (geography, language, culture) also limit services trade.

-

Protection takes many forms: Beyond traditional tariffs, non-tariff barriers (technical restrictions, licensing rules, government procurement policies) increasingly restrict Australian exports, especially in manufacturing and services.