Sources of Income and Wealth (HSC SSCE Economics): Revision Notes

Sources of Income and Wealth

Understanding where income and wealth come from helps explain patterns of inequality in Australia. By examining how each factor of production generates income and wealth, we can identify the key drivers of economic distribution.

Sources of household income

Household income in Australia derives from five main sources, each linked to different factors of production. These sources contribute different proportions to total national income.

Wages from the sale of labour

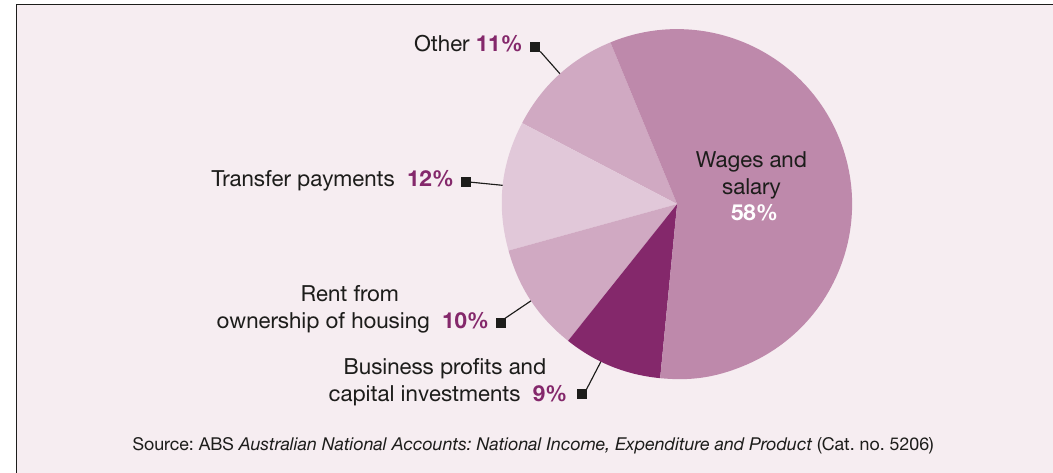

Labour income represents the dominant source of household income in Australia, accounting for 58% of total household income. This category encompasses:

- Wage and salary payments: Regular income received for participating in the labour market

- Non-wage benefits: Bonuses, fringe benefits and employer superannuation contributions

The Australian Bureau of Statistics classifies this income as "Compensation of employees" or "Returns to labour". For most Australian households, wage income forms the foundation of their economic wellbeing.

Wage and salary income is by far the most important income source for Australian households, representing more than half of all household income. This makes labour market participation the primary pathway to economic security for most families.

Rent from land

Property ownership generates rental income when land or buildings are leased to others. Investment properties are the primary example of this income source. Rent from ownership of housing accounts for 10% of household income in Australia.

This income stream requires initial capital to purchase property, meaning it is more accessible to households that already possess wealth. The ability to generate rental income thus contributes to wealth inequality.

Earnings from capital

Capital ownership provides significant returns through various channels:

- Financial assets: Investment funds, bank deposits, and savings accounts generate interest

- Share ownership: Dividends from company shares provide regular income

- Business ownership: Returns from owning companies or parts of companies

Capital earnings contribute 9% to household income through business profits and capital investments. However, ownership of capital is highly concentrated among Australia's wealthiest households. This concentration means that capital income primarily flows to those who already possess substantial wealth.

Link to inequality: The concentrated nature of capital ownership represents the main mechanism through which wealth inequality drives income inequality. Households with greater wealth accumulate more capital, which then generates additional income, creating a reinforcing cycle of wealth accumulation.

Profit from entrepreneurship

Many Australians operate small businesses, using entrepreneurial skill to generate income. When these enterprises make a profit, that income represents returns to entrepreneurship. The Australian Bureau of Statistics measures this through "mixed income from unincorporated enterprises".

Calculating entrepreneurial returns is particularly complex because small business income often combines returns to labour (the owner's work), capital (invested assets), and entrepreneurial skill. Despite this complexity, entrepreneurship remains an important income source for Australian households.

Transfer payments

Government benefits represent a significant income source, providing 12% of household income. Transfer payments redistribute income collected through taxation back to households requiring support.

Key characteristics of transfer payments:

- Social assistance benefits: Welfare payments supporting unemployed, sick, or disadvantaged individuals

- Social insurance benefits: Compensation payments such as workers' compensation

- Types of support: Unemployment benefits, age pensions, disability pensions, family allowances, and sickness benefits

Transfer payments play a crucial redistributive role in Australian society. Over one-third of total income tax collected funds these payments, helping reduce income inequality by supporting lower-income households.

Sources of wealth in Australia

Wealth differs fundamentally from income. While income represents a flow over time, wealth measures the stock of assets at a particular moment.

Understanding household net worth

The Australian Bureau of Statistics uses household net worth to measure private sector wealth. Net worth calculates the difference between what households own (assets) and what they owe (liabilities).

Calculating Net Worth:

This calculation provides a snapshot of household wealth by subtracting debts from total assets.

Current wealth levels (2021-22):

- Average household assets: $1.7 million

- Average household liabilities: $276,462

- Average net worth: approximately $1.4 million

Composition of household wealth

Australian household wealth concentrates in several key asset categories, with property dominating the composition.

Housing assets

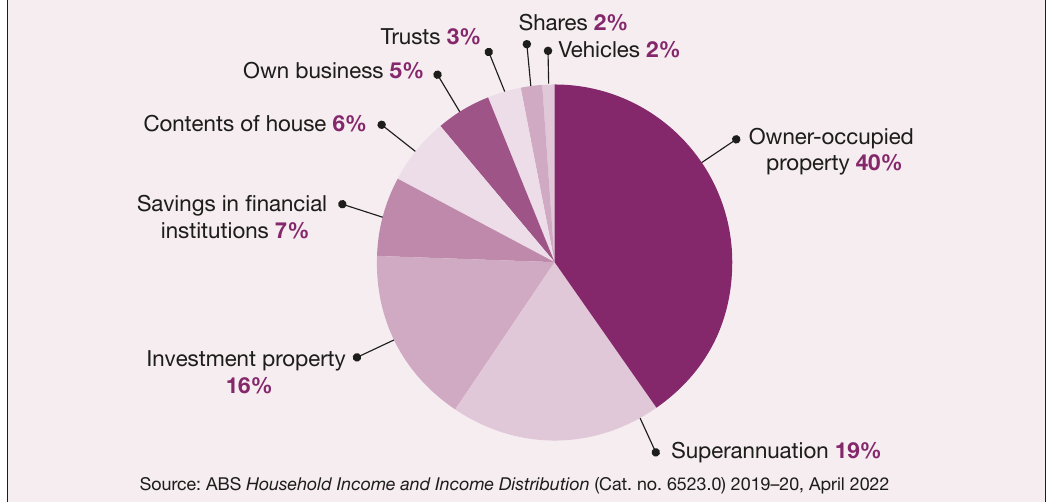

Owner-occupied property forms the largest single component of household wealth at 40% of total assets. The average value of owner-occupied homes reaches $502,500. Around two-thirds of Australian households own their primary residence, making home ownership central to wealth accumulation.

Investment property contributes an additional 16% of household wealth. Approximately 24% of households own property beyond their primary residence. Combined, real estate assets (both owner-occupied and investment properties) comprise 56% of total household wealth in Australia.

Property dominates Australian household wealth. More than half of all household wealth is held in real estate, making the property market a critical factor in wealth inequality. When house prices rise, wealth inequality typically increases because property ownership is not universal.

Superannuation

Superannuation represents the second-largest household asset and the largest financial asset. Superannuation funds account for 19% of household wealth, with an average value of $229,900 per household. Australia's compulsory superannuation system has made retirement savings a major wealth component.

Other assets

Remaining wealth distributes across several categories:

- Savings in financial institutions: 7% of household wealth

- Contents of house: 6% of household wealth

- Own business: 5% of household wealth

- Trusts: 3% of household wealth

- Shares: 2% of household wealth

- Vehicles: 2% of household wealth

Trends in wealth composition

The relative importance of different wealth sources has shifted over recent years:

Increasing components:

- Housing wealth has grown as property values have risen

- Superannuation has expanded due to compulsory contributions and investment returns

Declining components:

- Savings in financial institutions have decreased as a proportion

- Business ownership has fallen as a share of total wealth

These trends reflect both policy changes (such as compulsory superannuation) and economic conditions (such as property price growth). The dominance of housing in wealth composition means property market conditions significantly affect overall wealth inequality.

Exam guidance

What examiners expect when analysing income and wealth distribution:

- Distinguish between income and wealth: Income flows over time; wealth represents accumulated assets at a point in time

- Explain inequality mechanisms: Show how capital ownership creates a link between wealth inequality and income inequality

- Use current data: Reference specific percentages and dollar values from recent ABS statistics

- Connect to redistribution: Demonstrate understanding of how transfer payments reduce income inequality

- Identify trends: Recognise the growing importance of housing and superannuation in Australian wealth composition

Remember!

Key points to master:

- Five income sources: Wages (58%) dominate, followed by transfer payments (12%), rent (10%), and business profits/capital (9%)

- Net worth formula: Household assets minus household liabilities equals net worth (average $1.4 million)

- Property dominance: Real estate comprises 56% of household wealth (40% owner-occupied, 16% investment)

- Wealth-income link: Concentrated capital ownership among wealthy households explains how wealth inequality drives income inequality

- Redistribution role: Transfer payments provide 12% of household income, supporting lower-income households

Key terms to know:

- Compensation of employees

- Transfer payments

- Net worth

- Household assets and liabilities

- Mixed income from unincorporated enterprises

Critical framework:

Remember that income derives from factors of production: labour (wages), land (rent), capital (earnings), and entrepreneurship (profit). The government then redistributes some income through transfer payments. Wealth accumulates from saving income and asset appreciation, with property and superannuation dominating Australian household wealth.