Recent Trends in Inflation (HSC SSCE Economics): Revision Notes

Recent Trends in Inflation

Australia's inflation performance: a success story

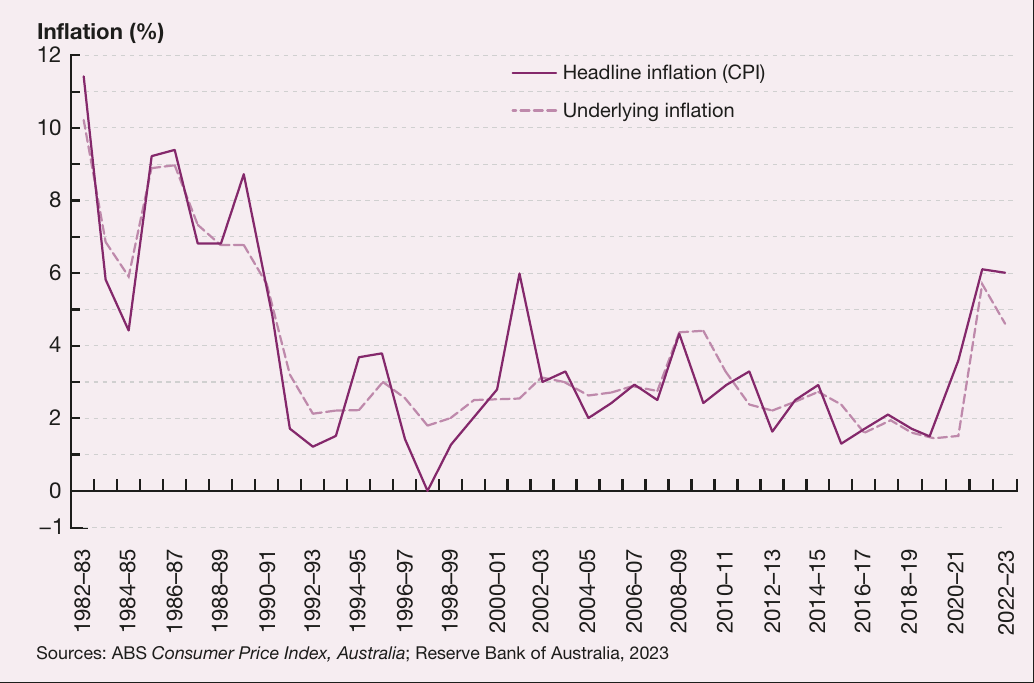

Australia has achieved one of the most significant macroeconomic successes of recent decades by maintaining consistently low inflation after experiencing high inflation during the 1970s and 1980s. Between 1996 and 2023, both headline and underlying inflation averaged just 2.6%.

The chart above shows Australia's inflation journey over four decades, highlighting the dramatic shift from volatile, high inflation in the 1980s to the stable, low inflation period that followed. This transformation represents a fundamental change in Australia's economic performance.

The inflation targeting framework

A critical factor behind Australia's low inflation success was the introduction of inflation targeting by the Reserve Bank of Australia (RBA).

Key dates:

- 1993: The RBA began targeting an inflation rate averaging 2–3% over the course of the economic cycle

- 1996: The inflation target was formalised through an agreement between the Treasurer and the RBA Governor

This target band remained the cornerstone of monetary policy, with inflation generally staying within or close to this range until 2022.

How inflation targeting works

The RBA's Interest Rate Strategy

The RBA uses interest rate adjustments to keep inflation within the target band:

- When inflationary pressures emerge, the RBA increases interest rates to slow demand growth and curb rising prices

- When inflation falls persistently below target, the RBA decreases interest rates to stimulate economic activity

This approach proved effective during episodes of inflationary pressure in 1994, 1999, 2007, 2010, and 2022.

The turning point: early 1990s recession

The early 1990s recession marked the end of Australia's high-inflation era. The economy emerged from this downturn with significantly lower inflation levels, which the RBA's new targeting framework then helped to maintain.

This framework created a systematic approach to managing inflation whenever pressures emerged, preventing a return to the high inflation rates of previous decades.

Factors behind sustained low inflation (1991-2019)

During Australia's remarkable unbroken run of economic growth from 1991 to 2019, several factors worked together to keep inflation pressures constrained:

Structural changes and microeconomic reform

Understanding Structural Change

Structural change refers to the process by which the pattern of production in an economy is altered over time, with certain products, processes, and industries disappearing while others emerge. During the 1980s and 1990s, Australia underwent significant structural transformation through microeconomic reform.

These reforms increased competition both within Australia and from overseas markets. Greater competition placed downward pressure on prices as businesses could not easily raise prices without losing market share.

Productivity improvements

Understanding Productivity

Productivity refers to the quantity of goods and services the economy can produce with a given amount of inputs such as capital and labour. Australia experienced improved productivity growth during the 1990s, which helped contain inflation.

Higher productivity meant businesses could produce more output without proportionally increasing costs, allowing the economy to grow without generating significant inflationary pressure.

Effective monetary policy

The RBA's monetary policy successfully addressed inflation pressures as they emerged, adjusting interest rates to maintain demand at appropriate levels relative to the economy's productive capacity.

The achievement: simultaneous goals

These factors combined to create an exceptional outcome - Australia achieved low inflation whilst simultaneously enjoying:

- Strong economic growth

- Falling cyclical unemployment

A Remarkable Economic Achievement

This combination had previously been difficult to achieve, as policies to reduce unemployment often risked increasing inflation. Australia's success in achieving all three goals simultaneously represented a major breakthrough in economic policy.

Notable periods of inflation variation

Elevated inflation (2005-2008)

Despite overall success, Australia experienced stronger inflationary pressures between 2005 and 2008. Underlying inflation peaked at 5.1% in September 2008, driven by:

- Higher global prices

- Strong domestic economic activity

This period ended with the 2008 global financial crisis, which reduced:

- Consumer confidence

- Investment spending

- Demand for labour

- Wage growth

The calm of the 2010s

Following the global financial crisis, Australia's inflation rate remained at or below the RBA's target band throughout the 2010s decade, representing a period of exceptional price stability.

The COVID-19 shock and recovery (2020-2023)

Deflationary pressure (2020)

Historic Deflationary Event

The COVID-19 recession created unprecedented deflationary pressure. Australia experienced:

- The largest quarterly fall in the Consumer Price Index (CPI) since 1931

- The first annual decline in inflation since the 1960s

This reflected severely weak economic activity, with falling prices for fuel and many services.

Several government emergency pandemic policies also put downward pressure on inflation during this period.

The inflation surge (2021-2023)

As the economy recovered from COVID-19, global inflation rates surged dramatically. Multiple factors combined to push inflation to its highest levels in several decades:

Supply-side factors:

- Disruptions to global supply chains

- High commodity prices

- The war in Ukraine causing the largest surge in energy prices in half a century

Demand-side factors:

- Low unemployment rates

- Wage growth pressures

- Rising rental costs

Peak inflation

Record Inflation Levels

In Australia, inflation reached its highest point in December 2022:

- Headline inflation: 7.8%

- Underlying inflation: 6.3%

Both measures significantly exceeded the RBA's 2-3% target band, marking the most severe inflationary episode in decades.

Future outlook

According to the Reserve Bank's survey of market economists (June 2023), inflation was expected to moderate:

- 2023-24: 3.3%

- 2024-25: 2.7%

This suggests a gradual return toward the RBA's target band, though inflation was expected to remain slightly elevated in the near term before normalising. The projected decline reflects expectations that supply chain disruptions would ease and demand pressures would moderate.

Understanding the two inflation measures

The chart and discussion reference two different inflation measures that are important to understand:

Two Key Inflation Measures

-

Headline inflation (CPI): The overall change in consumer prices, including all items in the consumer basket. This measure can be volatile due to temporary price shocks.

-

Underlying inflation: A measure that removes volatile price movements to show the persistent trend in inflation. The RBA focuses more on this measure for monetary policy decisions.

Both measures generally move together over time, but underlying inflation provides a clearer picture of sustained inflationary pressures in the economy.

Remember!

Key Points to Remember:

- Australia successfully maintained low inflation averaging 2.6% between 1996 and 2023, following high inflation in the 1970s-1980s

- The RBA's inflation targeting framework (2-3% target introduced in 1993, formalised in 1996) was crucial to this success

- Structural changes, microeconomic reform, and productivity improvements during the 1980s-1990s helped sustain low inflation alongside strong economic growth

- COVID-19 initially caused deflationary pressure (2020), but was followed by a sharp inflation surge peaking at 7.8% in December 2022 due to global supply disruptions, commodity price rises, the Ukraine war, and domestic factors like wage growth and rising rents

- Inflation was expected to moderate back toward the target band by 2024-25, though remaining slightly elevated in the transition period