Analysing Financial Situations Using Amortisation Tables (VCE SSCE General Mathematics): Revision Notes

Analysing Financial Situations Using Amortisation Tables

Introduction

An amortisation table is a powerful tool for tracking loan repayments, annuity payments, or investment growth over time. This note will help you understand how to use these tables to find final payments, calculate total amounts paid or earned, and visualise financial trends through graphs. These skills are essential for analysing real-world financial situations.

Amortisation tables provide a clear, payment-by-payment breakdown of how your loan balance decreases or investment grows. Understanding how to read and work with these tables is crucial for making informed financial decisions.

Finding the final payment in a reducing balance loan and an annuity

When paying off a reducing balance loan or receiving payments from an annuity, the financial arrangement must eventually reach a zero balance. The final payment is often different from the regular payments to ensure the balance reaches exactly zero dollars.

Why final payments differ

Regular payments are usually fixed amounts calculated at the start of the loan or annuity. However, after making several regular payments, the remaining balance may not divide evenly by the regular payment amount. Therefore, the final payment needs to be adjusted to pay off the exact remaining balance plus any final interest charge.

The final payment is almost always different from regular payments because it must account for the exact remaining balance and final interest, ensuring the account reaches precisely $0.

Method for calculating the final payment

To find the final payment:

- Calculate the interest on the remaining balance

- Add this interest to the remaining balance

The formula is:

Worked Example: Finding the Final Payment for a Reducing Balance Loan

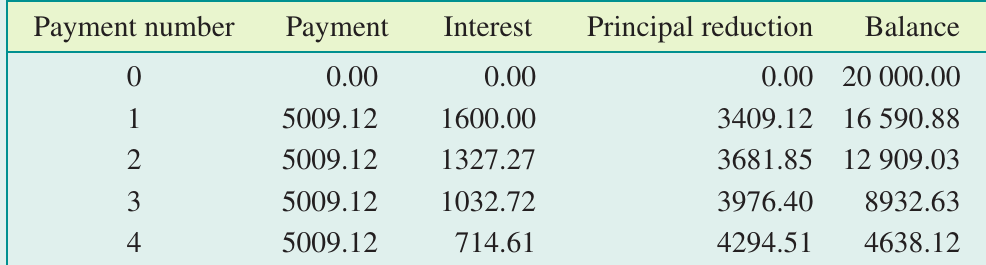

Question: Consider an amortisation table for a reducing balance loan of $20,000 with an interest rate of 8% per annum, compounding annually. Regular payments of $5,009.12 are made for the first four years. Calculate the final payment required in the fifth year to pay off the loan fully.

Solution:

First, we need to calculate the interest charged on the remaining balance of $4,638.12:

Now we can calculate the final payment by adding the remaining balance and the interest:

Therefore, the final payment is $5,009.17, which is five cents more than the regular payment.

Finding the total payment made/received and total interest paid/earned

Once you have a completed amortisation table, you can calculate the total amount paid on a loan (or received from an annuity) and the total interest paid (or earned). This information helps you understand the true cost of borrowing or the total benefit of an investment.

Two methods for finding total interest

There are two equivalent methods for calculating total interest:

Method 1: Subtract the original principal from the total payments

Method 2: Add up all the values in the interest column

Both methods will give you the same answer, so choose whichever is more convenient for the situation. Method 1 is often quicker when you need the total interest, while Method 2 serves as a useful check of your calculations.

Worked Example: Finding Total Payment and Total Interest

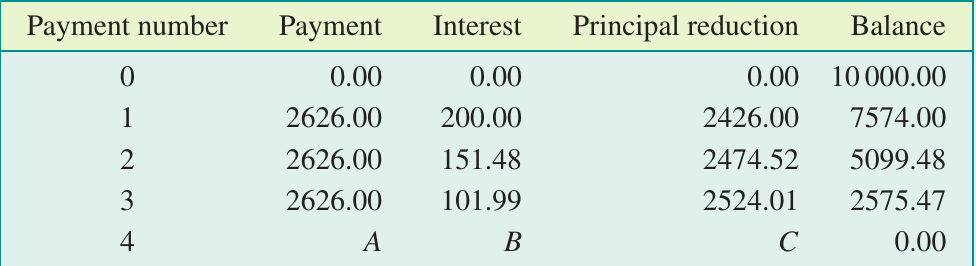

Question: Consider an amortisation table for a reducing balance loan of $10,000 with an interest rate of 8% per annum, compounding quarterly. Three quarterly payments of $2,626 are made.

a) Complete the amortisation table for payment four such that the final payment ensures the balance is zero.

b) Calculate the total payment made for the loan.

c) Calculate the total interest paid on the loan.

Solution:

Part a: Complete the table

First, find the interest (B) on the remaining balance:

The principal reduction (C) must equal the remaining balance:

The final payment (A) is the sum of the balance and interest:

Part b: Calculate total payments

Add all payments made over the four quarters:

Part c: Calculate total interest

Method 1: Subtract the principal from total payments

Method 2: Add up the interest column

Both methods confirm that the total interest paid is $504.98.

Plotting points from an amortisation table

Creating graphs from amortisation table data helps visualise how different components change over time. These visual representations make it easier to spot trends and understand the financial situation at a glance.

Understanding the trends

For a reducing balance loan:

- Interest paid each period decreases because the balance is getting smaller

- Principal paid off each period increases because more of each payment goes toward reducing the loan

For a compound interest investment:

- Interest earned each period increases because the balance is growing larger with each deposit

Common Pattern to Remember:

In a reducing balance loan, interest and principal reduction move in opposite directions: as interest decreases, principal reduction increases.

In an investment with regular deposits, both balance and interest move in the same direction: both increase over time.

Worked Example: Plotting from an Amortisation Table

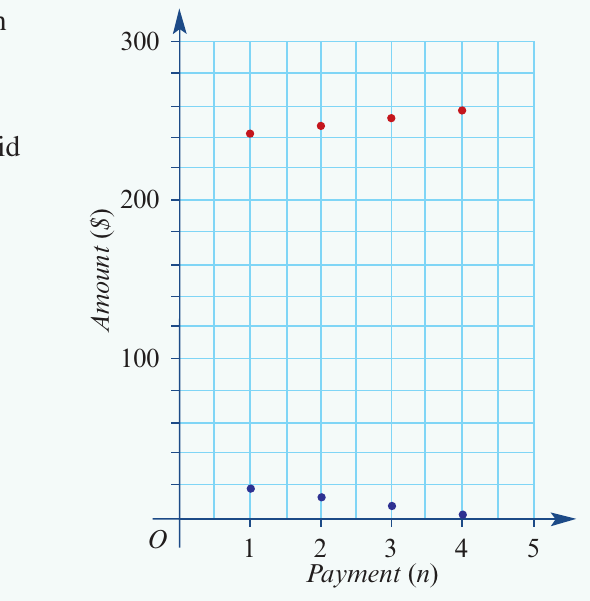

Question: Consider the following amortisation table for a reducing balance loan. Plot a graph of the interest and principal reduction on the same graph.

| Payment number | Payment | Interest | Principal reduction | Balance |

|---|---|---|---|---|

| 0 | 0.00 | 0.00 | 0.00 | 1000.00 |

| 1 | 257.85 | 12.50 | 245.35 | 754.65 |

| 2 | 257.85 | 9.43 | 248.42 | 506.23 |

| 3 | 257.85 | 6.33 | 251.52 | 254.71 |

| 4 | 257.89 | 3.18 | 254.71 | 0.00 |

Solution:

For this reducing balance loan, we plot two sets of points on the same graph:

- Blue dots represent the interest paid each payment period

- Red dots represent the principal reduction each payment period

Interpreting the graph

Notice how the blue dots (interest) show a decreasing trend from left to right. This occurs because the outstanding balance decreases with each payment, so interest is calculated on progressively smaller amounts.

Meanwhile, the red dots (principal reduction) show an increasing trend. Since each payment is approximately the same amount, as less money goes to interest, more money goes toward paying off the principal.

This inverse relationship between interest and principal reduction is a key characteristic of reducing balance loans and helps explain why it's beneficial to pay off loans as quickly as possible. The sooner you pay, the less total interest you'll pay overall.

Key Points to Remember:

-

The final payment in a loan or annuity equals the remaining balance plus the final interest charge:

-

Total interest can be calculated two ways: subtract the original principal from total payments, or add up all interest entries in the table.

-

When graphing data from an amortisation table for a loan, interest decreases over time while principal reduction increases.

-

For investments with regular deposits, both the balance and interest earned increase over time.

-

Understanding these patterns helps you make better financial decisions about loans, investments, and payment strategies.