Interest-Only Loans (VCE SSCE General Mathematics): Revision Notes

Interest-Only Loans

What is an interest-only loan?

An interest-only loan is a special type of loan where you only pay back the interest charges each period, rather than paying off any of the principal (the original amount borrowed). This means the amount you owe stays exactly the same throughout the entire loan term.

These loans are commonly used for investment purposes, such as buying property or shares, where the borrower expects the investment to grow in value over time.

How interest-only loans work

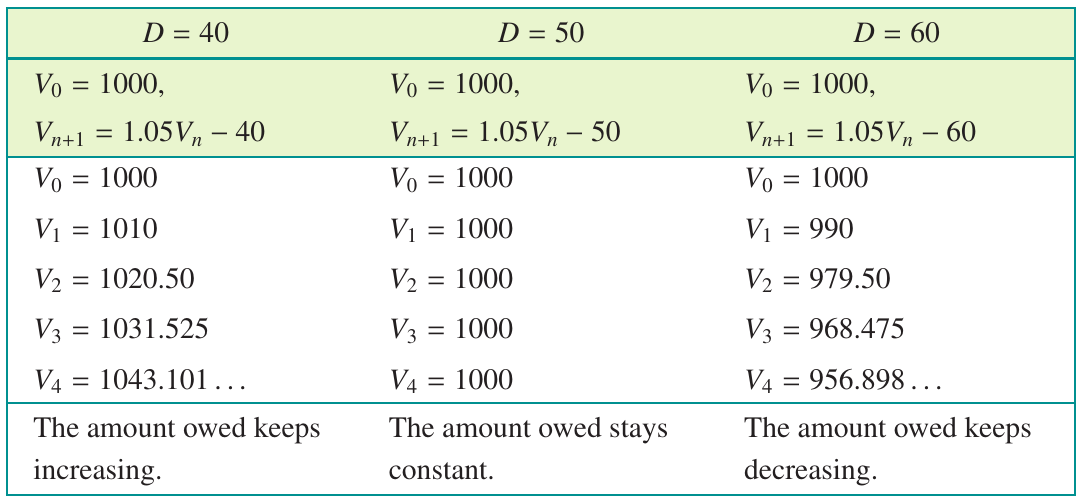

Let's understand this concept with a simple example. Imagine you borrow $1000 at an interest rate of 5% per annum, with interest compounding yearly.

After one year, the interest charged on this loan will be:

- 5% of $1000 = $50

If you only repay $50 (the interest), your loan balance remains at $1000. The key is that your payment exactly matches the interest charged, so the principal never changes.

Understanding different payment amounts

To see why the payment must equal the interest, let's examine what happens with three different payment amounts on our $1000 loan at 5% per annum:

We can model this using the recurrence relation , , where is the payment amount.

Looking at these three scenarios:

- When (less than the interest): The loan balance increases over time because you're not paying enough to cover the interest charges

- When (equal to the interest): The loan balance stays constant at $1000 - this is an interest-only loan

- When (more than the interest): The loan balance decreases because you're paying more than just the interest

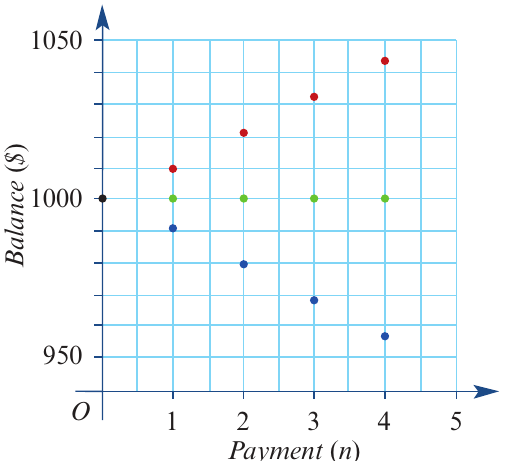

Visualising the balance

We can plot these three scenarios on a graph to see how the balance changes:

The graph clearly shows:

- Red dots: Payments below $50 cause the balance to increase

- Green dots: Payments of exactly $50 keep the balance constant at $1000

- Blue dots: Payments above $50 cause the balance to decrease

A loan where the balance stays constant is what we call an interest-only loan.

Mathematical model for interest-only loans

Let be the value of the interest-only loan after payments have been made. We can model this with:

Recurrence Relation:

Where:

- is the growth multiplier

- is the annual interest rate (as a percentage)

- is the number of compounding periods per year

- is the regular payment per compounding period

For an interest-only loan, the payment equals the interest charged, which is given by:

This formula tells us that the regular payment is simply the interest rate per period multiplied by the principal.

Finding the regular payment amount

When you know the principal and interest rate, you can calculate the required payment for an interest-only loan.

Worked Example: Finding the payment

Problem: Jane borrows $50,000 to buy some shares. She negotiates an interest-only loan at 9% per annum, compounding monthly. What monthly amount will Jane need to pay?

Solution using the formula:

We use the formula

Given information:

- (amount borrowed)

- (annual interest rate)

- (monthly compounding)

Substituting into the formula:

Answer: Jane needs to repay $375 every month on this interest-only loan.

Solution using a finance solver:

For an interest-only loan, we can think about just one compounding period since all periods are identical.

Enter the following values into the finance solver:

- N: 1 (one compounding period)

- I%: 9 (annual interest rate)

- PV: 50000 (present value - amount borrowed)

- FV: -50000 (future value - same amount still owed after payment)

- Pp/Y: 12 (monthly payments)

- Cp/Y: 12 (monthly compounding)

Then solve for PMT (the payment amount).

The calculator gives PMT = -375, which means Jane must pay $375 each month. The negative sign indicates money flowing out (a payment).

Finding the principal amount

If you know the payment amount and interest rate, you can work backwards to find how much was originally borrowed.

Worked Example: Finding the principal

Problem: A loan at 6% per annum, compounding monthly, requires payments of $440 each month. If this is an interest-only loan, what is the principal?

Solution:

We use the formula and solve for

Given information:

- (monthly payment)

- (annual interest rate)

- (monthly compounding)

Substituting and rearranging:

Answer: The principal is $88,000.

Finding the interest rate

If you know both the payment amount and the principal, you can calculate the interest rate.

Worked Example: Finding the interest rate

Problem: An interest-only loan of $1,000,000 requires quarterly payments of $4000. What is the annual interest rate?

Solution:

We use the formula and solve for

Given information:

- (quarterly payment)

- (principal)

- (quarterly compounding)

Substituting and rearranging:

Answer: The annual interest rate is 1.6%.

Exam tips

Important strategies for exam success:

- Remember that for an interest-only loan, the balance never changes

- The payment formula is crucial - make sure you can rearrange it to find any unknown variable

- Check whether interest is compounding monthly, quarterly, or at some other frequency - this affects the value of

- When using a finance solver for interest-only loans, set and make PV and FV equal in magnitude but opposite in sign

- Always express your final answer with appropriate units (dollars for money, percentage for rates)

Key Points to Remember:

- An interest-only loan means you only pay the interest charges each period, keeping the principal constant

- The payment formula is:

- If payments are less than the interest, the balance increases

- If payments equal the interest, the balance stays constant (this is an interest-only loan)

- If payments are greater than the interest, the balance decreases

- These loans are commonly used for investment purposes where the investor expects the investment value to grow over time