Private Health Insurance (VCE SSCE Health and Human Development): Revision Notes

Private Health Insurance

Private health insurance is a type of insurance where you pay a regular fee (called a premium) in exchange for coverage of health-related costs that Medicare doesn't cover. It's an optional extra on top of Medicare that gives you more choice about your healthcare.

This insurance plays an important role in Australia's health system. Not only does it give people more options for their medical care, but it also helps take pressure off the public health system by encouraging some people to use private hospitals instead.

What does private health insurance cover?

When you buy private health insurance, you can choose between two main types of coverage:

Hospital cover pays for treatment when you're admitted to hospital as a private patient. This can be in either a public or private hospital.

Extras cover (also called ancillary or general treatment cover) helps pay for services that Medicare doesn't usually cover, such as:

- Dental care

- Physiotherapy

- Chiropractic treatment

- Optometry

- Dietetics

Many people choose to have both types of cover, while others select only one depending on their needs and budget.

The four tier system

Since 2020, all private hospital insurance policies must be classified into one of four tiers. This makes it easier to compare different policies and understand what level of coverage you're getting:

- Gold – covers the most categories of hospital treatment

- Silver – covers the second most categories of hospital treatment

- Bronze – covers the second fewest categories of hospital treatment

- Basic – covers the fewest categories of hospital treatment

The tier tells you how comprehensive your hospital cover is, with Gold offering the broadest coverage and Basic offering the most limited coverage.

How private health insurance works

When you have private health insurance, you pay a premium. The amount you pay depends on several factors, including how many people are covered by your policy and what options your policy includes.

The main benefit of having private hospital insurance is being able to be admitted as a private patient in either a public or private hospital. Here's how the costs are covered:

Medicare's contribution: Medicare still pays 75% of the doctor's Schedule fee for your treatment.

Your insurance company's contribution: Your private health insurance pays most of the remaining doctor's fees and contributes to the cost of your hospital accommodation.

Your contribution: Sometimes you may need to pay something called 'the gap'. This happens when the total bill is more than what Medicare and your insurance company cover together.

Understanding "the gap"

The gap is the difference that you must pay out of your own pocket. Many insurance companies have partnership arrangements with hospitals to keep these gap payments as small as possible.

Benefits of private health insurance

People with private health insurance generally enjoy several benefits:

Choice of hospital and doctor: You can choose which hospital you go to and which doctor treats you, both in private and public hospitals.

Own room: In private hospitals, you can often have your own room if one is available.

Shorter waiting times: You typically don't have to wait as long for elective surgery (procedures that aren't emergencies, like knee reconstruction). In the public system, these waiting times can be quite lengthy.

Private hospitals in Australia

Private hospitals are largely funded by private health insurance companies. They provide about one-third of all hospital beds in Australia and handle 40% of hospital separations (when patients are discharged or transferred).

Advantages and disadvantages

Like any insurance product, private health insurance has both benefits and drawbacks:

| Advantages | Disadvantages |

|---|---|

| Enables access to private hospital care | Premiums can be expensive |

| Choice of doctor while in public or private hospital | Sometimes you must pay gap costs, which means the insurance doesn't cover the whole fee and you must pay the difference |

| Shorter waiting times for some medical procedures such as elective surgery | Qualifying periods apply for some conditions before you can make a claim (for example, pregnancy) |

| Depending on your level of cover, part or all of services such as dental, chiropractic, physiotherapy, optometry and dietetics could be paid for | |

| Helps keep the costs of operating Medicare under control | |

| High income earners with private health insurance don't have to pay the additional Medicare levy surcharge tax | |

| Government rebate available for eligible policy holders | |

| Lifetime Health Cover incentive |

Exam tip

When discussing advantages or disadvantages in an exam, you may need to link them to a specific case study. Make sure your points are relevant to the particular situation described in the question, rather than just listing general advantages or disadvantages.

Private health insurance incentives

When Medicare was introduced in 1984, many Australians cancelled their private health insurance. They realised they could access essential medical treatment through Medicare without paying expensive insurance premiums. This shift put strain on the public health system, as fewer people were using private hospitals.

To encourage more Australians to buy and keep private health insurance, the government introduced four main financial incentives for people who purchase hospital cover.

Private health insurance rebate

In 1999, the Australian government introduced a rebate (refund) on private health insurance premiums. Originally set at 30% for everyone, this rebate became income tested in 2012. This means the amount of rebate you receive now depends on your income and age.

Rebate rates for individuals under 65 (2021)

- Income under $90,000: 24.6% rebate

- Income between $90,001 and $105,000: 16.4% rebate

- Income between $105,001 and $140,000: 8.2% rebate

- Income over $140,001: no rebate

For families, the income thresholds are higher to reflect their additional expenses:

- Families earning under $180,000: 24.6% rebate

- Families earning between $180,001 and $210,000: 16.4% rebate

- Families earning between $210,001 and $280,000: 8.2% rebate

- Families earning $280,001 or more: no rebate

Older Australians receive slightly higher rebates. Those aged 65-70 get approximately an extra 4% rebate, while those over 70 receive an extra 8% rebate.

Income testing is a way of determining whether someone is eligible for government assistance based on how much they earn. It's sometimes called means testing.

If you're eligible for this rebate, you have two options:

- Pay a reduced premium (with the government contributing the rebate amount directly to your insurer)

- Pay the full premium and claim the rebate back when you lodge your tax return

Even though the government pays a substantial amount to fund this rebate, it helps raise much-needed funds for the health system that wouldn't exist otherwise.

Lifetime Health Cover

Lifetime Health Cover was introduced to encourage younger people to buy private hospital insurance earlier in life and keep it for the long term.

Here's how it works: If you first take out private hospital insurance after age 31, you pay an extra 2% on your premiums for every year you are over 30.

Lifetime Health Cover calculations

- Someone who first buys hospital cover at age 40 will pay 20% more than someone who first bought it at age 30 (10 years × 2% = 20%)

- Someone who first buys hospital cover at age 35 will pay 10% more than someone who first bought it at age 30 (5 years × 2% = 10%)

This additional cost continues until you've had hospital cover continuously for 10 years. After that, your premium returns to the normal cost (without the Lifetime Health Cover loading).

This incentive encourages younger people to take up private health insurance when they're healthier and less likely to make claims, then keep it throughout their lives.

Medicare levy surcharge

The Medicare levy surcharge is an additional tax that high income earners must pay if they don't have private hospital insurance.

Who pays it? People earning more than $90,000 per year (or families earning more than $180,000) who don't have private hospital insurance.

How much is it? The surcharge ranges from 1% to 1.5% of your taxable income, depending on how much you earn.

This incentive encourages high income earners to buy private health insurance rather than relying entirely on the public health system. For many high earners, paying for private health insurance premiums costs less than paying this extra tax.

Age-based discount

The age-based discount is the newest incentive, introduced in 2019. Under this scheme, insurance companies have the option (it's not compulsory) to offer young people aged 18-29 a discount of up to 10% on their hospital cover premiums.

The discount works like this:

- You get a 2% reduction for each year you're under 30

- The maximum discount is 10% (for someone aged 18-20)

Age-based discount examples

- An 18-year-old could receive a 10% discount (12 years under 30 × 2% = 24%, but capped at 10%)

- A 25-year-old could receive a 10% discount (5 years under 30 × 2% = 10%)

- A 28-year-old could receive a 4% discount (2 years under 30 × 2% = 4%)

If you receive this discount, you keep it until you turn 41. After that, it decreases by 2% each year until it reaches zero.

Discount phase-out example

If you join at age 25 with a 10% discount:

- You keep the 10% discount from age 25 to 40

- At age 41, it reduces to 8%

- At age 42, it reduces to 6%

- At age 43, it reduces to 4%

- At age 44, it reduces to 2%

- At age 45, the discount disappears completely

Like all the other incentives, the age-based discount aims to encourage more people to buy private health insurance and maintain it throughout their lives.

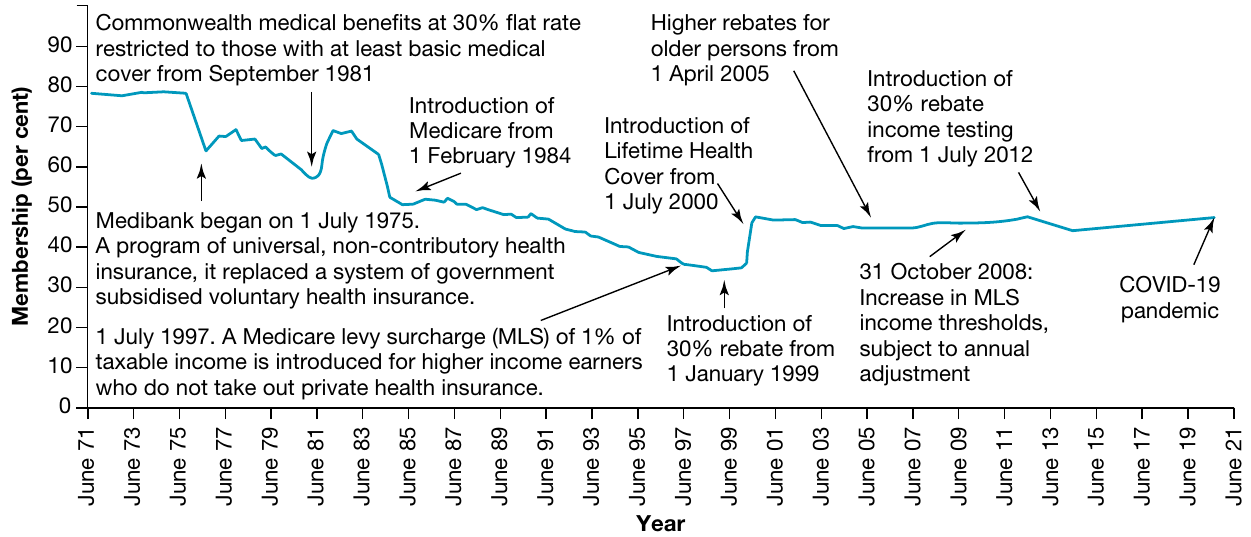

Changes in private health insurance membership over time

The proportion of Australians with private health insurance has fluctuated significantly since the 1970s.

Before Medicare: In the early 1970s, around 80% of Australians had private health insurance. This was before Medibank (later replaced by Medicare) was introduced.

After Medicare's introduction (1984): When Medicare began providing universal healthcare, private health insurance membership gradually declined. People realised they could access good quality, affordable essential healthcare through Medicare without paying for private insurance. Membership dropped to around 30% by the late 1990s.

Impact of government incentives

The decline in membership slowed after the introduction of the private health insurance rebate in 1999. When Lifetime Health Cover was introduced in 2000, membership rose sharply, showing how effective these government incentives were at encouraging people to take out private cover.

Recent trends: Since 2012, private health insurance membership has remained relatively stable. In 2020, approximately 47% of Australians had hospital cover. This represents less than half the population, but is significantly higher than the low point reached before the incentives were introduced.

These changes demonstrate how government policy can influence people's healthcare choices and help balance the use of public and private health services.

Key Points to Remember:

- Private health insurance is optional coverage that supplements Medicare by covering costs Medicare doesn't pay for

- There are two main types: hospital cover (for treatment in hospital) and extras cover (for services like dental and physiotherapy)

- Hospital policies are classified into four tiers from most comprehensive (Gold) to least comprehensive (Basic)

- The main benefits include choice of doctor and hospital, shorter waiting times, and access to private hospital care

- Four government incentives encourage Australians to buy private health insurance: the rebate, Lifetime Health Cover, the Medicare levy surcharge, and the age-based discount

- After Medicare's introduction, membership in private health insurance fell dramatically but recovered after government incentives were introduced in the late 1990s and early 2000s