Case Study: World Trade in Bananas (AQA A-Level Geography): Revision Notes

Case Study: World Trade in Bananas

Overview of the global banana trade

Bananas represent one of the world's most significant agricultural commodities, raising numerous environmental, economic, social and political issues. For many people in the least developed countries, bananas serve as a dietary staple, ranking as the fourth most important food crop and feeding approximately 500 million people globally.

The international banana trade generates substantial economic value, with annual revenues surpassing $15 billion. As an export commodity, bananas rank fifth globally among agricultural products, with world exports reaching approximately 23.3 million tonnes. These fruits provide essential nutrition, containing significant quantities of energy, vitamins, fibre and protein. A single banana can supply more than an adult's daily potassium requirement.

Whilst global production is substantial, around 80 per cent of bananas grown are consumed locally or domestically rather than entering international trade. This means that the international trade represents only a fraction of total banana production.

The banana industry

Growing conditions and production

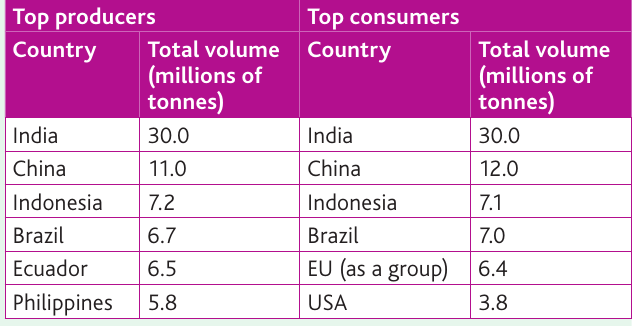

Bananas thrive in hot, rainy lowlands within tropical regions. In 2019, worldwide banana production totalled 120 million tonnes. The leading producer nations - India, China, Indonesia and Brazil - are simultaneously the largest consumers, as their output is primarily consumed domestically rather than exported. In contrast, production in African countries mostly serves the domestic market.

With the exception of the Philippines, the primary commercial export production areas are concentrated in Latin America and the Caribbean. Several nations in this region, particularly Ecuador, Costa Rica and Guatemala, rely heavily on banana exports for their economic wellbeing. The Philippines has emerged as an increasingly significant producer and exporter, supplying bananas to Japan and other parts of East Asia and the Middle East.

Environmental impacts

Heavy Environmental Costs of Banana Cultivation

Banana cultivation carries substantial environmental costs that affect ecosystems and local communities:

- Banana varieties are vulnerable to diseases, leading to widespread chemical treatment throughout the production cycle

- Commercial plantations managed by large TNCs apply approximately 30 kg of active chemical ingredients per hectare annually

- These chemicals include fungicides, insecticides and herbicides, with fertilisers also applied extensively

- After harvesting, the fruit undergoes washing with disinfectant

- The banana industry has the largest agrochemical input of any crop entering international trade (except cotton)

Banana plantations also contribute to environmental degradation through:

- Deforestation

- Soil fertility reduction (due to chemical contaminants)

- Loss of biodiversity

- Water pollution as chemical pollutants enter waterways

The global banana trade structure

Producer groups

World trade is controlled by two distinct producer groups:

The ACP group (Africa, Caribbean and Pacific) comprises mainly small and medium-sized producers. This group includes former European colonies, and banana production in the Caribbean is managed less by TNCs and more by small-scale family farm growers and co-operatives. Traditional production methods in both the Philippines and Africa have followed a similar pattern of small and medium growers, though TNC involvement has increased in both regions recently.

The 'dollar producers' of Latin America (primarily Ecuador and Colombia) are controlled by large US TNCs. Most bananas destined for export grow on large monoculture plantations, particularly in Latin America and increasingly in Africa. Production in the Caribbean has declined, with more control shifting to small and medium-scale growers on family farms and co-operatives.

Monoculture Plantations Explained

Monoculture plantations are large-scale agricultural operations that grow only a single crop variety. This approach maximises efficiency but increases vulnerability to disease and requires intensive chemical inputs.

Export and import patterns

Trade follows the traditional pattern whereby developing regions export a low-value primary product to wealthier developed countries. Latin America and the Caribbean dominate exports, producing 17 million tonnes of bananas for international markets in 2018.

The leading exporters are Ecuador, Costa Rica, Colombia and Guatemala. Smaller Central American nations, such as Panama, are now exporting at faster rates. In Asia, which accounts for 17 per cent of the export market, the main commercial producer is the Philippines. In Africa, where exports are smaller, the two principal producers are Côte d'Ivoire and Cameroon.

The largest importers are the EU and the USA.

Distribution of value

As with many commodities produced in developing regions and consumed in developed countries, 85 per cent of the price paid by the final consumer remains in the richer country and never reaches the farmers who bear most of the risks of producing a perishable fruit.

Unequal Value Distribution

Retailers capture the largest slice of profits, with bananas representing one of the highest profit-margin items in supermarkets. Workers on average receive between 5 and 9 per cent of the total banana value, whilst retailers manage to capture 36-43 per cent (Figure 7.29 in source material).

Market control and organisation

The role of TNCs

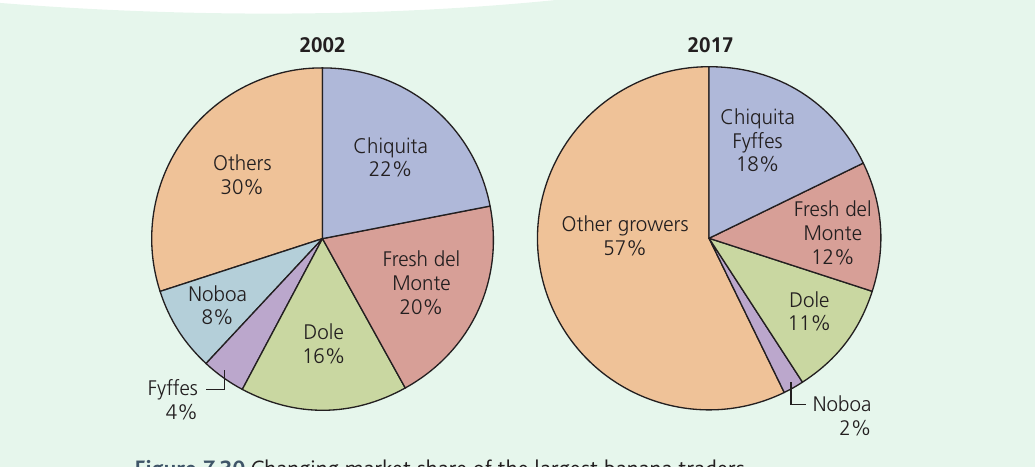

Historically, the banana trade was dominated by four large transnational corporations: Chiquita, Dole, Del Monte (all US-based TNCs) and Fyffes (based in Ireland). The other important producer is Noboa, which operates as a national corporation based in Ecuador.

Vertical Integration in the Banana Trade

Vertical integration occurs when companies control multiple stages of the supply chain, from owning plantations to operating transport and distribution networks in consuming countries.

These companies are vertically integrated in the supply chain. They own or contract with plantations, operate their own sea transport and ripening facilities, and maintain their own distribution networks in consuming countries.

Changes in market organisation

The structure of banana trade has evolved significantly in recent years. In 2002, the five major companies controlled 70 per cent of the market, but their combined share decreased to less than 45 per cent by 2017.

The large companies have moved away from direct plantation ownership, instead favouring guaranteed supply contracts with medium and large-scale producers. Consequently, an increasing number of national growing companies based in Ecuador, Costa Rica and Colombia now sell their products either to the TNCs (who act as distributors) or directly to retailers in developed countries, such as Wal-Mart and Tesco.

Shift in Supply Chain Power

A shift in power has occurred as retailers have gained an increasingly dominant position in the supply chain. As market share becomes concentrated amongst fewer retailers, suppliers have little choice but to accept conditions such as low prices, discounts and delayed payments, or risk removal from the supplier list.

Trade disputes and governance

The Lomé Convention and SDT

The banana trade became the subject of one of history's longest trade disputes, lasting 20 years from 1992 until the 2009 Geneva Banana Agreement came into effect in 2012.

The dispute originated in 1975 when EU countries negotiated a trade agreement with their former colonies. This agreement, known as the Lomé Convention, was made with 71 African, Caribbean and Pacific countries (ACP countries), many of whom produced bananas.

Special and Differential Treatment (SDT)

Special and Differential Treatment (SDT) refers to preferential tariff-free import quotas granted to developing countries. The intention is to enable these former European colonies to develop independently without having to use overseas aid.

These countries received SDT with preferential tariff-free import quotas to supply EU markets. The agreement was subsequently extended to include additional suppliers such as Cameroon, Dominican Republic, Belize, Ivory Coast, Jamaica, Ghana, Surinam and the Windward Isles.

This protection primarily benefited smaller, family-run farms in the Caribbean and Africa, shielding them from competition with the large Latin American producers, whose bananas were produced more cheaply on mechanised plantations.

The trade war

At the time, the US TNCs controlling the Latin American crop were supplying around 75 per cent of the EU market, whilst only 7 per cent came from Caribbean suppliers. Despite this, in 1992, the TNCs filed a complaint to GATT (now WTO) that the practice constituted unfair trade. In 1997, the WTO ruled against the EU and ordered the EU to cease the discrimination.

This ruling led to a trade war between the USA and the EU. As a result, the US government imposed WTO-approved sanctions on a range of EU products.

The Geneva Compromise

A compromise was eventually reached in Geneva in 2009, with the EU agreeing to gradually reduce tariffs on Latin American bananas from 2012 onwards. Tariffs decreased from $176 to $75 per tonne between 2012 and 2018. Following EU trade agreements, the deal now also applies to other Latin American countries. However, to safeguard other producers, the EU will not reduce the tariff further if there is over-supply in the EU market, because tariff increases remain possible.

Concerns for ACP producers

There are concerns from the ACP producers that they cannot compete effectively. Of the Caribbean countries, only the Dominican Republic, Belize and the Windward Isles are competing successfully with the larger producers. Their focus on producing organic and fair trade bananas is meeting the needs of a growing market for ethical, sustainably-produced food in richer EU countries.

Contemporary challenges

Race to the bottom

Because of the low prices paid to suppliers by supermarkets, many of the larger companies are relocating their plantations increasingly to West Africa, as companies search for lower labour costs and weaker legislation. This practice is called pursuing a 'race to the bottom' in terms of labour and environmental standards.

Race to the Bottom

Race to the bottom describes when companies compete to reduce costs by lowering labour standards and environmental protections, often by relocating to countries with weaker regulations.

Plantation work relies on sub-contracted casual labour. The work involves long shifts in unbearable heat, and many workers fail to earn enough to cover their basic needs.

Fair trade and organic bananas

There has been steady growth in sales of so-called 'sustainable' bananas, which includes both fair trade and organic produce. This trend helps smaller-scale producers in the Caribbean and in parts of Africa and will partially counter the deterioration of conditions in banana production.

There is undoubtedly a growing market segment of ethical consumers in richer nations who are becoming aware of the shortcomings in the supply chain and are willing to pay a higher price for a certified product.

Disease threats

There are many different banana varieties around the world, but the Cavendish cultivar, which accounts for 47 per cent of bananas grown, makes up 99 per cent of global trade. It has been grown commercially since it was discovered to be resistant to tropical race 1 (TR1), a fungus which brought the previous most popular variety, the Gros Michel, to the brink of extinction in the mid-twentieth century.

The TR4 Disease Threat

A new disease, TR4, is now ravaging Cavendish plantations throughout South East Asia and Australia and is spreading to Africa. TR4 can lie dormant in soil for decades and has proven resistant to fungicides, so there is concern that it will take hold in Latin America.

The Cavendish variety is ripe for attack because bananas have no seeds and reproduce asexually - they cannot be hybridised. The only options will be to genetically modify the variety or to encourage consumers to start eating other varieties.

Summary: key points about the banana trade

Key Points to Remember:

The world trade in bananas demonstrates a number of relevant points about trade, especially in primary commodities:

-

Mass production in developing countries has negative environmental consequences, including heavy chemical use, deforestation and biodiversity loss

-

TNCs have a large degree of control over markets and can influence political decisions through their economic power

-

The WTO supports free trade against protectionist activities or agreements at all costs, even if the protectionism may help development. In the banana trade dispute, the lobbying power of US TNCs took precedence over the SDT agreements for least developed countries, which were not truly effective in this situation

-

Geopolitical processes mean that trade disputes can spread and escalate to trade wars between regional trading blocs, affecting multiple sectors beyond the original commodity

-

Power and control of food production has shifted away from growers and towards retailers in high-income countries, who capture the majority of the profit margin

-

More ethical, sustainable consumer markets are growing but relatively slowly and only in places that can afford products bought at a higher price, limiting their impact on improving conditions for the majority of producers

Remember!

Essential Facts About the Global Banana Trade:

-

Bananas are the 5th most traded agricultural commodity globally, generating over $15 billion annually, but most production (80%) is consumed domestically

-

Two producer groups dominate: ACP countries (Africa, Caribbean, Pacific) with smaller-scale farms, and Latin American 'dollar producers' with large TNC-controlled monoculture plantations

-

The 20-year banana trade war (1992-2012) resulted from the EU's Lomé Convention giving preferential treatment to ACP countries, which the USA challenged through the WTO, ultimately forcing the EU to reduce tariffs

-

Market power has shifted from TNCs (whose share fell from 70% in 2002 to under 45% in 2017) to major retailers in developed countries, who capture 36-43% of the final value whilst farmers receive only 5-9%

-

Environmental and social challenges persist, including heavy chemical use (30kg per hectare annually), race to the bottom labour conditions, and the TR4 disease threat to the Cavendish variety that dominates global trade