Interest Rates (Edexcel A-Level Business): Revision Notes

Interest Rates

What are interest rates?

An interest rate is the price of borrowing or saving money. When businesses or individuals borrow money, they must pay interest on the loan. Equally, when they save money in a bank or building society, they receive interest on their savings.

Interest rates are expressed as a percentage of the amount borrowed or saved. The rate determines how much interest must be paid or will be earned over a specific period (usually one year).

Interest rates serve a dual purpose: they represent the cost of borrowing for those who need funds and the reward for saving for those who have surplus funds. This fundamental concept underpins all financial decisions in business.

Worked examples

Borrowing example:

A small business borrows $10,000 from a bank for one year with an interest rate of 7%.

Calculation:

The business will pay $700 in interest charges over the year.

Saving example:

A business has $1 million in the bank for one year as working capital with an interest rate of 3%.

Calculation:

The business will earn $30,000 in interest income over the year.

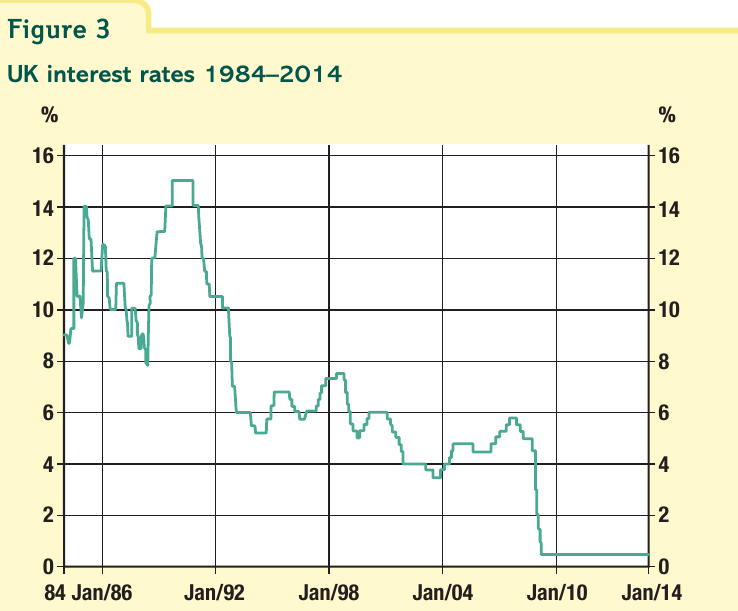

Historical context of UK interest rates

Interest rates in the UK have varied dramatically over the past three decades. In the late 1980s, rates peaked at around 15%, which had severely damaging effects on businesses. Since the 2008 financial crisis, the base rate has been maintained at just 0.5% - historically very low levels that have generally been helpful for businesses.

The dramatic fall in interest rates from 15% to 0.5% represents one of the most significant economic policy shifts in UK history. This 30-fold reduction has fundamentally changed how businesses approach borrowing, investment, and financial planning.

Monetary policy

Monetary policy refers to the use of interest rates to help control the economy. The government (through the Bank of England) adjusts interest rates to manage economic activity. For example, if inflation is rising because demand is increasing too quickly, the government might raise interest rates to dampen demand and slow price increases.

The Bank of England uses interest rates as its primary tool to maintain price stability and support economic growth. Understanding monetary policy is essential for anticipating changes in the business environment.

How interest rates affect business costs

Changes in interest rates directly impact a business's overhead costs because interest charges form part of these fixed expenses.

Variable rate loans

Variable rates mean that banks or other lenders can change the interest rate on borrowed money at any time. When interest rates in the economy rise, businesses with variable rate loans face higher interest payments.

Impact of rate increase on variable rate loans:

A business with a $10,000 overdraft experiences a rate increase from 6% to 7%.

Before increase:

After increase:

Result: Annual interest payments increase by $100 ($700 - $600).

Caution with variable rates: Businesses with variable rate loans face uncertainty in their financial planning. An unexpected rate rise can significantly increase costs and reduce profitability, particularly for highly leveraged businesses.

Fixed rate loans

Fixed rates mean the bank cannot change the interest rate over the agreed term (the repayment period) of the loan. Businesses with only fixed-rate loans are protected from interest rate rises during the loan term. However, if they need to take out new loans when rates are higher, they will face increased costs.

Fixed rate loans provide certainty and stability in financial planning, allowing businesses to accurately forecast their interest costs over the loan period. This can be particularly valuable during periods of economic uncertainty or when rates are expected to rise.

How interest rates affect business investment

Interest rate changes significantly influence how much businesses invest in new buildings, plant and machinery. There are four main reasons why higher interest rates reduce investment:

The Four Key Investment Effects:

Rising interest rates discourage business investment through multiple mechanisms:

- Increased loan costs reduce project profitability

- Saving becomes more attractive than investing

- Paying off debt becomes preferable to new projects

- Falling demand reduces projected returns

The cost of loans increases

Investment projects are often financed through borrowing. When interest rates rise, the cost of loans increases, which reduces the profitability of investment projects. Some businesses may decide to postpone or cancel their investment plans because the higher borrowing costs make projects unviable.

Even a small increase in interest rates can have a significant impact on long-term investment projects. For example, on a $1 million loan over 10 years, a 1% rate increase could add over $100,000 to total interest costs, potentially making the difference between a profitable and unprofitable project.

Saving becomes more attractive

Businesses can choose to save their funds rather than invest in physical assets. Higher interest rates make financial savings more attractive relative to investing in machinery or buildings. For example, if rates rise from 5% to 8%, a business might shelve an investment project and save the money instead to earn the higher interest.

Paying off existing debt becomes preferable

Rising interest rates increase the cost of existing variable rate borrowing. Rather than investing, businesses may choose to use available funds to pay off existing loans, reducing both their costs and the financial risk associated with debt.

Falling demand reduces project viability

Higher interest rates typically reduce total spending in the economy. This affects the profitability of investment projects because lower consumer demand means lower projected sales. For instance, an investment project might be profitable with 20,000 sales per year, but if demand falls to only 15,000 units, the project becomes unprofitable.

Investment viability and demand:

A manufacturing business plans to invest $500,000 in new machinery expected to generate $100,000 annual profit at 20,000 units sold.

Scenario 1 - Low interest rates (3%):

- Borrowing cost: $15,000 per year

- Net profit: $100,000 - $15,000 = $85,000

- Project is viable

Scenario 2 - High interest rates (8%), demand falls to 15,000 units:

- Borrowing cost: $40,000 per year

- Revenue falls due to lower demand: profit drops to $75,000

- Net profit: $75,000 - $40,000 = $35,000

- Project becomes much less attractive

How interest rates affect demand

Interest rates have a powerful effect on aggregate demand - the total demand for goods and services in the economy. Rising interest rates tend to reduce aggregate demand, while falling rates tend to increase it. This affects businesses through multiple channels:

Domestic consumption falls

Consumers are significantly affected by interest rate changes:

-

Consumer durables: Higher loan costs deter consumers from buying goods purchased on credit, such as cars, furniture and electrical equipment. These products are called consumer durables because they are used over a long period.

-

Mortgage payments: In the UK, homeowners with mortgages (loans to buy houses) often have variable rate loans. When rates rise, monthly repayments increase, leaving mortgage holders with less money to spend on other goods and services.

-

Housing market: Potential new home buyers may be deterred because they cannot afford higher repayments, directly reducing demand in the housing market.

-

Consumer confidence: If unemployment begins to rise due to reduced spending, consumer confidence falls further, making people even less willing to borrow and spend.

The impact on consumer spending creates a multiplier effect throughout the economy. When consumers reduce spending on durables, the businesses producing these goods face falling demand, which may lead to job cuts, further reducing consumer spending power and confidence.

Business investment decreases

As explained in the previous section, higher interest rates discourage businesses from investing in new buildings, machinery and equipment. This reduces demand for investment goods, affecting the businesses that manufacture these products.

Stock levels are reduced

Businesses hold stocks of raw materials and finished goods, but maintaining these inventories costs money. Higher interest rates increase the cost of holding stock because the money tied up in inventory could instead be used to reduce borrowing and interest payments.

This encourages destocking - reducing stock levels. This is particularly likely if rising interest rates have reduced demand in the economy, meaning less production is needed. When retailers cut their stock levels, they order less from suppliers, causing a fall in demand throughout the supply chain.

The destocking cascade: When businesses throughout a supply chain simultaneously reduce their stock levels, the cumulative effect can cause a sharp fall in orders for manufacturers. This amplifies the impact of higher interest rates on business demand.

Exports fall and imports rise

Rising interest rates typically cause the domestic currency to appreciate (increase in value) against other currencies. This has two effects:

-

Exports become less competitive: UK businesses find it harder to export profitably because their products become more expensive in foreign markets.

-

Imports become more competitive: Foreign firms find it easier to gain sales in the UK domestic market because they can reduce their prices in pounds while maintaining margins in their own currency.

The result is falling exports and increased import competition, both reducing demand for UK-produced goods.

Currency appreciation creates a double challenge for domestic manufacturers: they lose competitiveness in both export markets (due to higher prices) and their home market (due to cheaper imports). This effect can persist for months or years after interest rate changes.

Summary

Key Points to Remember:

-

Interest rates represent the price of borrowing or saving money, affecting both costs and returns for businesses and individuals

-

Since 2008, UK interest rates have remained at historic lows (0.5%), compared to peaks of 15% in the late 1980s

-

Higher interest rates increase business costs (particularly for variable rate borrowing) and reduce investment through multiple channels: higher loan costs, more attractive savings, debt repayment preference, and falling demand

-

Interest rates affect aggregate demand through four main channels:

- Consumer spending (durables, mortgages, housing, confidence)

- Business investment

- Stock level adjustments

- International trade (exports and imports)

-

Monetary policy uses interest rate changes to control economic activity and inflation, with the Bank of England adjusting rates to manage the economy

Key Terms:

- Interest rate - the price of borrowing or saving money

- Base rate - the benchmark interest rate set by the Bank of England

- Variable rate - interest rate that can be changed by the lender

- Fixed rate - interest rate that remains constant over the loan term

- Monetary policy - using interest rates to control the economy

- Aggregate demand - total demand for goods and services in the economy

- Consumer durables - goods used over a long period (cars, furniture, appliances)

- Destocking - reducing inventory levels