Break-even (Edexcel A-Level Business): Revision Notes

Break-even

Break-even analysis is a fundamental financial planning tool that helps businesses determine the minimum level of sales needed to cover all costs. Understanding break-even is essential for making informed business decisions, particularly when starting up or launching new products.

What is contribution?

Contribution is the amount of money remaining from sales revenue after variable costs have been deducted. This money "contributes" towards covering fixed costs and generating profit.

Why contribution matters: While contribution is not the same as profit, it shows how much each sale adds towards covering the business's fixed costs. Once all fixed costs are covered, contribution becomes profit.

Unit contribution measures the contribution from selling one unit:

Worked Example: Calculating Unit Contribution

If a business sells a product for $990 and the variable cost is $890:

Total contribution measures the contribution from multiple units sold:

Alternatively:

Worked Example: Calculating Total Contribution

If 1,000 units are sold with a unit contribution of $1.50:

Using contribution to calculate profit

Once you know total contribution, calculating profit is straightforward:

Worked Example: Camping Trailer Manufacturer

A camping trailer manufacturer has fixed costs of $200,000 per year. Each trailer sells for $800 with variable costs of $500 per unit.

If 2,000 trailers are sold:

Step 1: Calculate unit contribution

Step 2: Calculate total contribution

Step 3: Calculate profit

Understanding the break-even point

The break-even point occurs when total revenue exactly equals total costs. At this point, the business makes neither profit nor loss.

The break-even output is the quantity of units that must be produced and sold to reach the break-even point.

For many businesses, reaching break-even represents an important milestone, showing that all costs have been covered and any additional sales will generate profit.

Calculating break-even output using contribution

The simplest method to calculate break-even output uses contribution:

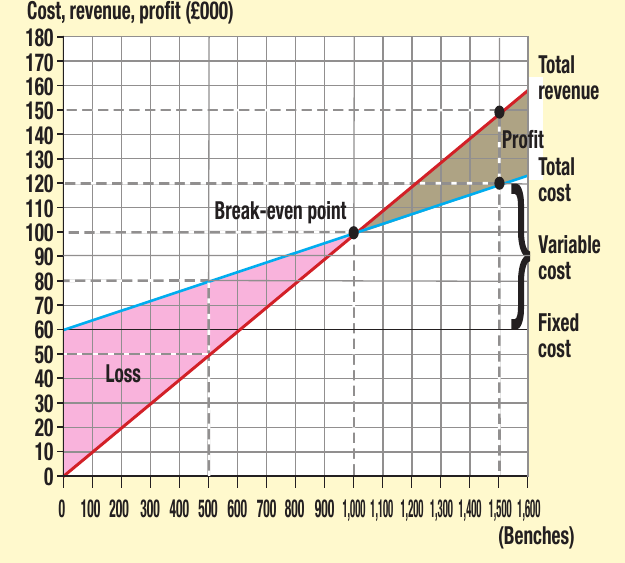

Worked Example: Park Bench Business

A business making park benches has the following cost structure:

- Fixed costs: $60,000

- Variable cost per bench: $40

- Selling price per bench: $100

Step 1: Calculate contribution per unit

Step 2: Calculate break-even output

This means the business must produce and sell 1,000 benches to cover all costs.

Verifying break-even calculations

You can check your break-even calculation by comparing total costs and total revenue at the break-even output:

At 1,000 benches:

Total costs equal total revenue, confirming the break-even point.

Break-even charts

A break-even chart provides a visual representation of costs, revenue, and profit at different output levels. The chart plots output on the horizontal axis and costs, revenue, and profit on the vertical axis.

Key features of a break-even chart

Fixed costs line: A horizontal line showing that fixed costs remain constant regardless of output level.

Total cost line: Starts at the fixed cost level and rises as output increases, reflecting the addition of variable costs.

Total revenue line: Starts at zero and rises with output. The steeper the line, the higher the selling price.

Break-even point: Where the total cost and total revenue lines intersect. At this point, the business makes neither profit nor loss.

Loss zone: The area below the break-even point (shaded pink in the diagram) where total costs exceed total revenue.

Profit zone: The area above the break-even point (shaded beige in the diagram) where total revenue exceeds total costs.

Reading information from break-even charts

Break-even charts allow you to quickly identify:

-

Total costs at any output level: Read up from the output on the horizontal axis to the total cost line, then across to the vertical axis.

-

Total revenue at any output level: Read up from the output to the total revenue line, then across to the vertical axis.

-

Profit or loss at any output level: Measure the vertical distance between the total cost and total revenue lines. Above break-even, this gap represents profit. Below break-even, it represents loss.

-

Fixed costs: The point where the total cost line intersects the vertical axis (when output is zero).

-

The relationship between fixed and variable costs: At low output levels, fixed costs represent a larger proportion of total costs. As output increases, variable costs become more significant while fixed costs remain constant.

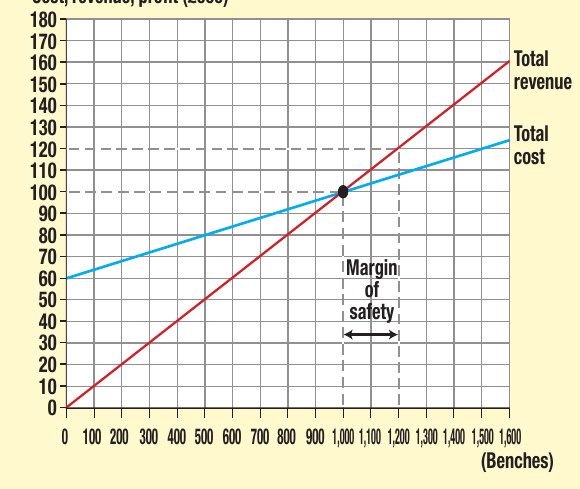

Margin of safety

The margin of safety measures how far current output exceeds the break-even level. It shows by how much sales can fall before the business starts making a loss.

Worked Example: Park Bench Business Margin of Safety

Using the park bench business:

- Break-even output: 1,000 benches

- Current output: 1,200 benches

This means sales can fall by 200 benches before the business makes a loss.

Why margin of safety matters

Large margin of safety: Provides a safety cushion. Sales can drop significantly before losses occur, giving the business more protection against market changes.

Small margin of safety: Indicates higher risk. Even a modest fall in sales could push the business into loss-making territory.

Businesses generally aim to operate with a comfortable margin of safety to protect against unexpected changes in demand or market conditions.

Using break-even analysis in business decisions

Break-even analysis helps businesses answer critical "what if" questions when planning for the future:

Pricing decisions: What would happen to the break-even point if prices increased or decreased?

New product launches: How many units of a new product must be sold to avoid making a loss?

Cost management: What impact would rising costs have on the break-even point?

Make or buy decisions: Would the break-even point be lower if components were bought from external suppliers rather than made in-house?

Start-up planning: What minimum level of output must be achieved to prevent losses when starting a new business?

Break-even analysis is also essential in business plans, particularly when seeking finance from banks or investors. Lenders want to see that a business understands its cost structure and knows what sales level is required to become viable.

Limitations of break-even analysis

While break-even analysis is a useful tool, it has several important limitations:

Output equals sales assumption

Break-even analysis assumes all output is sold immediately, meaning no stock is held. In reality, many businesses maintain stocks of finished goods to manage changes in demand. Some businesses may also stockpile unsold output during quiet periods rather than laying off staff, meaning production doesn't always equal sales.

Static conditions

Break-even charts are drawn for a specific set of conditions at one point in time. They cannot easily accommodate sudden changes in wages, material costs, or technology. Market conditions change constantly, making the analysis quickly outdated if not regularly updated.

Data accuracy

The reliability of break-even analysis depends entirely on the accuracy of the underlying data. If fixed costs are underestimated or variable costs incorrectly calculated, the break-even output will be wrong. Poor data quality leads to flawed decisions.

Example: If fixed costs are underestimated by $10,000, the calculated break-even point will be lower than the actual break-even point, potentially leading to unrealistic sales targets.

Linear relationships assumption

Break-even charts assume that cost and revenue lines are straight (linear). In practice, these relationships are often curved:

Revenue considerations: Businesses may need to offer discounts on large orders, meaning total revenue doesn't increase proportionally at high output levels.

Cost considerations: Bulk-buying discounts can reduce costs at higher output levels, meaning the total cost line may curve downward.

When relationships are non-linear, the simple break-even chart becomes less accurate.

Multi-product businesses

Most businesses sell more than one product, each with different variable costs and selling prices. This creates a problem: how should fixed costs be allocated across different products? There are various allocation methods, but none is perfect. If fixed costs are incorrectly allocated to individual products, the break-even analysis for each product becomes unreliable.

Stepped fixed costs

Some fixed costs don't remain constant over all output ranges. To increase production capacity, a business may need to rent additional premises or buy more machinery, causing fixed costs to "step up" suddenly. Break-even analysis becomes difficult when fixed costs change at different output levels.

Remember!

Key Points to Remember:

-

Contribution per unit is calculated by subtracting variable cost from selling price. It shows how much each sale contributes to fixed costs and profit.

-

Break-even output is found by dividing fixed costs by contribution per unit. This shows the minimum sales needed to cover all costs.

-

Break-even charts provide a visual tool to analyse costs, revenue, profit, and losses at different output levels. The break-even point is where total cost and total revenue lines intersect.

-

Margin of safety is the difference between current output and break-even output. A larger margin of safety provides more protection against falling sales.

-

Break-even analysis has limitations: it assumes all output is sold, conditions remain unchanged, relationships are linear, and data is accurate. It also struggles with multi-product businesses and stepped fixed costs.