Business Planning (Edexcel A-Level Business): Revision Notes

Business Planning

Introduction

Planning is essential for any business, particularly when seeking to raise finance. For businesses like CoolCo Ltd, a children's clothing manufacturer looking to expand capacity and raise £200,000, a comprehensive business plan with detailed financial forecasts is the critical first step in attracting investors such as business angels or venture capitalists.

Research consistently shows that start-up businesses which prepare thorough business plans have significantly higher success rates than those that do not. This is because effective planning forces entrepreneurs to think carefully about every aspect of their venture before committing resources and time.

The relevance of a business plan

Setting up a business represents a life-changing decision with far-reaching consequences. A business plan provides a structured document showing how the business will develop over a specific time period. Beyond internal planning, business plans serve crucial external purposes.

Obtaining finance

Lenders and investors require clear evidence before committing funds to a business venture. A well-prepared business plan demonstrates:

- How investment funds will be allocated and spent

- When and how investors can expect returns on their investment

- The viability and profitability potential of the business proposition

When companies plan to raise money through floating on the stock market, they must publish a prospectus - a formal document containing key elements of the business plan and other information for potential shareholders. This gives investors confidence in the company's future prospects before they purchase shares.

Benefits of a thorough business plan

A comprehensive and well-written business plan delivers several advantages:

Objective assessment: It encourages business owners to evaluate their business idea objectively, critically and without emotional bias. This helps identify potential weaknesses before they become problems.

Strategic direction: The plan provides a clear roadmap showing the intended direction for business development, ensuring all stakeholders understand the journey ahead.

Action planning: It identifies specific tasks that must be completed and goals that must be achieved to maximise chances of success.

Risk identification: Potential problems can be flagged in advance, allowing investors to be aware of risks and enabling the business to develop solutions proactively.

Credibility: A professional business plan demonstrates to lenders and investors that the owner is cautious, responsible, serious and credible - qualities that inspire confidence.

The contents of a business plan

Banks and other financial institutions provide detailed templates outlining what should be included in a business plan. The main components are:

Executive summary

An overview of the entire business start-up that briefly describes:

- The business opportunity to be exploited

- The marketing and sales strategy

- Operations

- Finance

This section should be concise yet compelling, as it often determines whether readers continue to the detailed sections.

The business opportunity

A clear description of:

- The product or range of products to be made or sold

- The quantity to be sold

- Estimated pricing

Buying and production

Details about:

- Where the business will source its supplies

- Production methods to be employed

- Cost of production

Financial forecasts

Multiple financial projections including:

- Sales forecast: predicted revenue over time

- Cash-flow forecast: expected cash movements

- Profit and loss forecast: anticipated profitability

- Break-even analysis: the point at which the business covers all costs

The business and its objectives

Fundamental information:

- Business name

- Trading address

- Legal structure (sole trader, partnership, limited company, etc.)

- Aims and objectives

The market

Market analysis covering:

- Size of the potential market

- Description of target customers

- Nature of competition

- Marketing priorities and strategy

Personnel

Human resource information:

- Who will run the business

- Number of employees (if any)

- Skills, qualifications and experience of key personnel

Premises and equipment

Details of:

- Premises to be used (owned, leased, or from home)

- Equipment needed

- How these will be financed

Finance

Explanation of:

- Where start-up finance will come from

- How the business will be funded operationally

- Financial requirements over time

Cash-flow forecasts

Cash is the lifeblood of any business - without it, trading cannot continue. Research suggests approximately 20% of business failures are directly attributable to poor cash flow management. Even businesses operating in favourable market conditions can fail if they cannot pay staff wages and bills when due.

A cash-flow forecast is a planning tool that lists all likely receipts (cash inflows) and payments (cash outflows) over a future period, typically shown month by month. All entries represent estimates since they refer to future transactions that have not yet occurred.

Interpreting cash-flow forecasts

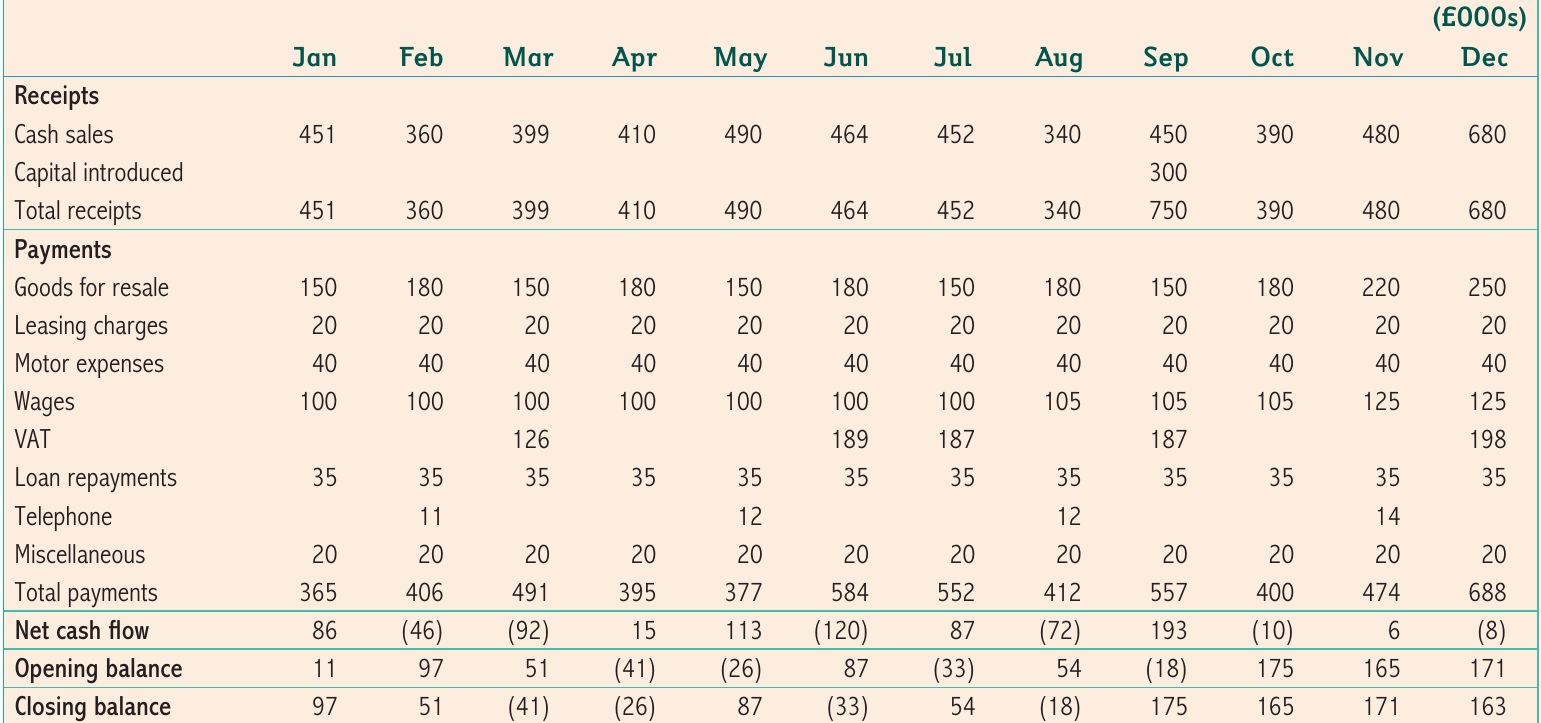

Understanding how to read and interpret cash-flow forecasts is essential for effective financial management. Let's examine a twelve-month forecast for Fishan's Ltd, a grocery wholesaler:

Key components explained

Opening balance: The amount of cash the business has at the start of the period.

Receipts (cash inflows): Money expected to come into the business from various sources such as:

- Cash sales

- Payment from credit customers

- Capital introduced by owners

- Loans received

- Interest earned

Payments (cash outflows): Money expected to leave the business for:

- Purchasing goods for resale (stock)

- Wages and salaries

- Rent and rates

- Utilities (electricity, gas, water)

- VAT payments

- Loan repayments

- Marketing costs

- Other operating expenses

Key Formulas:

Reading the forecast month-by-month

Worked Example: Analyzing Fishan's Ltd Cash-flow Forecast

January: Fishan's starts with an opening balance of £11,000. Expected receipts of £451,000 exceed payments of £365,000, creating a positive net cash flow of £86,000. The closing balance reaches £97,000 (£11,000 + £86,000).

February: Payments (£406,000) exceed receipts (£360,000), resulting in a negative net cash flow of £46,000. However, the opening balance of £97,000 covers this deficit, leaving a healthy closing balance of £51,000.

March: This month presents a problem. Payments exceed receipts by £92,000, which is greater than the opening balance of £51,000. This creates a negative closing balance of £41,000 - a cash-flow problem requiring immediate attention, perhaps through bank borrowing.

April to May: Cash-flow difficulties persist in April despite positive net cash flow (because the opening balance is negative). By May, the positive net cash flow of £113,000 overcomes the negative opening balance, restoring a positive closing balance of £87,000.

June onwards: Problems recur in June and August, but from September forward, the business maintains positive closing balances. This improvement results from the owners introducing £300,000 of fresh capital in September.

Changes in cash-flow variables

Once prepared, cash-flow forecasts can be adjusted to show how changes in individual variables affect overall cash position. This flexibility makes them valuable planning tools.

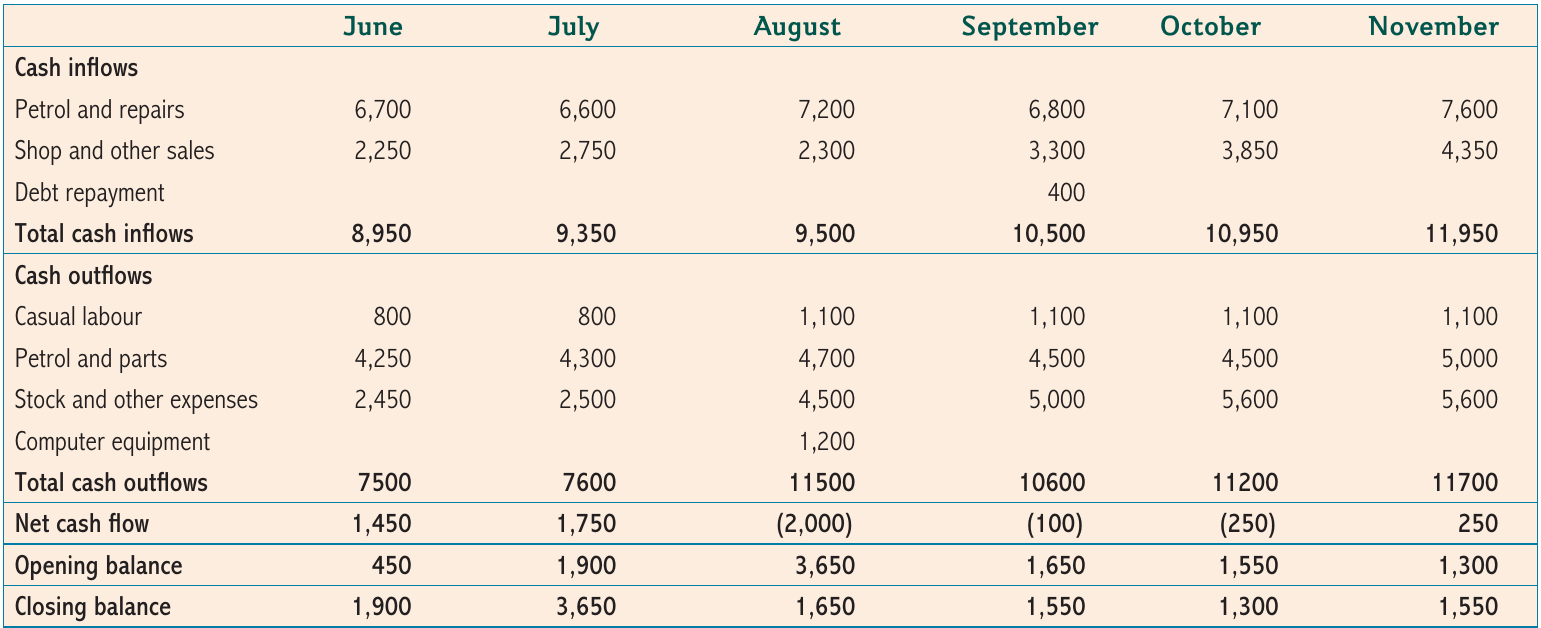

Consider Patel Motors, a garage and car service business that opened a shop in May:

The original forecast showed the closing cash balance improving from £1,900 in June to £3,550 in November - a positive trend.

However, circumstances changed:

- Computer equipment costing £1,200 was needed in August for repairing modern vehicles

- Casual labour costs increased to £1,100 monthly from August (due to shop staffing needs)

- An unexpected £400 debt repayment was received in September

The amended forecast reveals a significantly different outcome:

Worked Example: Impact of Variable Changes

Instead of improving to £3,550, the closing balance now falls to £1,550 by November - a difference of £2,000. This demonstrates how changes in single variables create ripple effects throughout the forecast.

The multiplier effect of variable changes

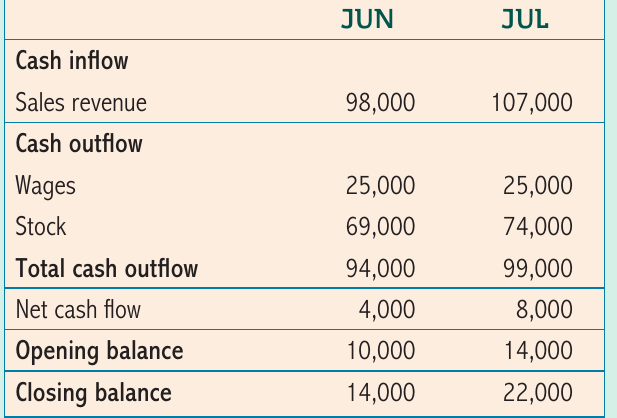

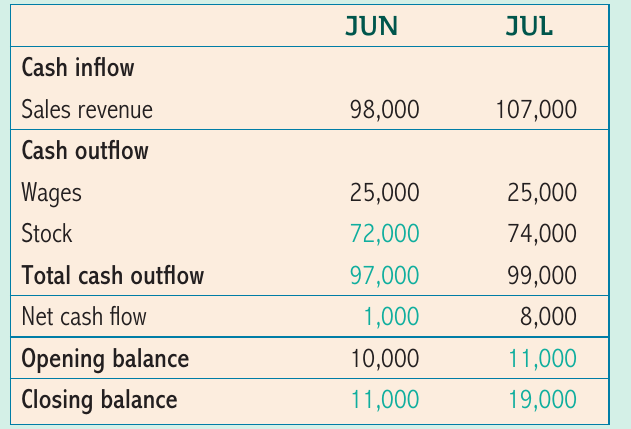

Even a simple change has multiple impacts on a cash-flow forecast. Consider this example:

A £3,000 increase in stock purchases in June (from £69,000 to £72,000) affects five different values:

- Total cash outflow increases

- Net cash flow decreases

- Closing balance for June decreases

- Opening balance for July decreases

- Closing balance for July decreases

Important: Modern spreadsheet software automatically recalculates all affected values when variables change, making scenario planning quick and efficient.

The use of cash-flow forecasts

Cash-flow forecasts serve multiple important functions in business management:

Identifying the timing of cash shortages and surpluses

Forecasts clearly show the monthly closing balances, enabling businesses to:

- Identify when borrowing is needed: For example, Fishan's Ltd could see in advance that overdraft facilities would be required in March, April, June and August

- Spot surplus opportunities: Large cash surpluses might present opportunities to purchase equipment or make investments

- Avoid unnecessary interest charges: By planning ahead, businesses can delay certain payments until cash is available, reducing the need for expensive overdraft facilities

Cash-flow forecasts prove particularly valuable for businesses with seasonal demand. These businesses experience irregular cash inflows - high during peak seasons and low during off-peak periods. Forecasting allows them to plan payments strategically, delaying non-essential spending during low cash-flow months.

Supporting applications for finance

Lenders consistently require businesses to provide documents demonstrating:

- Current financial performance

- Future business outlook

- Solvency (ability to meet financial obligations)

A cash-flow forecast indicates the future financial health of the business. For start-ups, producing a cash-flow forecast as part of the business plan is standard practice - potential investors or lenders will not finance a business without one.

Enhancing the planning process

Careful planning helps businesses clarify aims and improve performance. Cash-flow forecasting is fundamental to the planning process because it:

- Forces businesses to think about the future systematically

- Helps identify problems before they occur

- Reduces the likelihood of costly mistakes

Without forward planning, businesses operate reactively rather than proactively, typically resulting in poorer performance.

Monitoring cash flow

During and after each financial period, businesses should compare forecasted figures with actual results. This variance analysis helps:

- Identify where problems have occurred

- Determine reasons for significant differences between predicted and actual figures

- Take corrective action (for example, investigating overpayments)

Constant monitoring enables effective cash flow control and improves the accuracy of future forecasts.

The limitations of cash-flow forecasts

Despite their usefulness, cash-flow forecasts have several limitations that must be recognised:

Forecasts depend on estimates

Much of the financial information used in forecasts is estimated rather than certain:

Sales revenue: Even under normal trading conditions, predicting future sales is extremely difficult. Customer behaviour, market conditions and competitive actions all affect actual sales.

Variable costs: These depend on sales volumes, which are themselves uncertain. If sales estimates prove inaccurate, cost estimates will also be wrong.

Fixed costs: These are more predictable (rent, rates, insurance) but can still change unexpectedly.

When cash inflow and outflow estimates are inaccurate, the calculated net cash flows and closing balances become unreliable, potentially leading to poor decisions.

External factors beyond control

Business activity is subject to external forces that owners and managers cannot control:

- Interest rate changes: Affect borrowing costs and customer spending

- Economic conditions: Recessions reduce consumer spending

- Government legislation: New regulations may increase compliance costs

- Exchange rates: Impact import costs and export revenues

- Competition: New entrants or competitor actions affect sales

- Consumer tastes: Changing preferences alter demand patterns

For example, a wheat farm's cash-flow forecast would be significantly affected by poor weather conditions reducing crop yields - a factor completely outside management control.

Resource intensive

Preparing and maintaining cash-flow forecasts requires:

- Time to gather accurate information

- Regular updates for meaningful monitoring

- Employee or owner attention that could be directed elsewhere

There is a risk that business owners spend excessive time on financial forecasting at the expense of meeting customer needs or developing products.

One-dimensional focus

Cash-flow forecasts concentrate solely on cash movements. While cash is crucial, other variables are equally important for business success:

- Profit: Overall financial performance

- Profit margins: Efficiency of operations

- Productivity: Output per employee or unit of input

- Market share: Competitive position

- Customer satisfaction: Long-term sustainability

The cash-flow forecast is a one-dimensional tool and cannot evaluate overall business performance in isolation. It must be used alongside other financial and non-financial measures.

Exam guidance

When answering exam questions on business planning and cash-flow forecasting:

Exam Strategy Guide:

For "explain" questions: Clearly define key terms and show cause-and-effect relationships. For example, explain how a business plan helps obtain finance by demonstrating profitability potential to investors.

For "assess" or "analyse" questions:

- Examine both advantages and limitations

- Apply your answer to the specific business context provided

- Consider short-term versus long-term impacts

- Use data from tables and forecasts to support your points

For "evaluate" questions:

- Present balanced arguments showing both sides

- Make a clear judgement at the end

- Justify your conclusion with evidence from the case

- Consider whether cash-flow forecasting is beneficial overall to the specific business

When completing cash-flow calculations:

- Show all working clearly

- Remember: Closing balance = Opening balance + Net cash flow

- The closing balance of one period becomes the opening balance of the next

- Use brackets to show negative figures

- Check your calculations add up correctly

Remember!

Key Takeaways:

- A business plan demonstrates how a business will develop over time and is essential for obtaining finance from investors and lenders

- Business plans should include executive summary, market analysis, financial forecasts, operational details and information about personnel and resources

- Cash-flow forecasts predict future cash receipts and payments, helping businesses identify when they will face cash shortages or surpluses

- ;

- Changes in any single variable in a cash-flow forecast have multiple knock-on effects throughout the forecast period

- Cash-flow forecasts help businesses time their borrowing, support finance applications, enhance planning and enable monitoring of actual versus predicted performance

- Limitations include reliance on estimates, vulnerability to external factors, resource requirements and one-dimensional focus on cash rather than overall business performance

Key Terms:

- Business plan - a document showing how the business will develop over a period of time

- Cash-flow forecast - lists all likely receipts (cash inflows) and payments (cash outflows) over a future period

- Net cash flow - the difference between total receipts and total payments in a period

- Opening balance - cash available at the start of a period

- Closing balance - cash available at the end of a period

- Prospectus - a document containing key business plan elements published when floating on the stock market

- Solvency - the ability of a business to meet its financial obligations

Critical Formulas: