Liability (Edexcel A-Level Business): Revision Notes

Liability

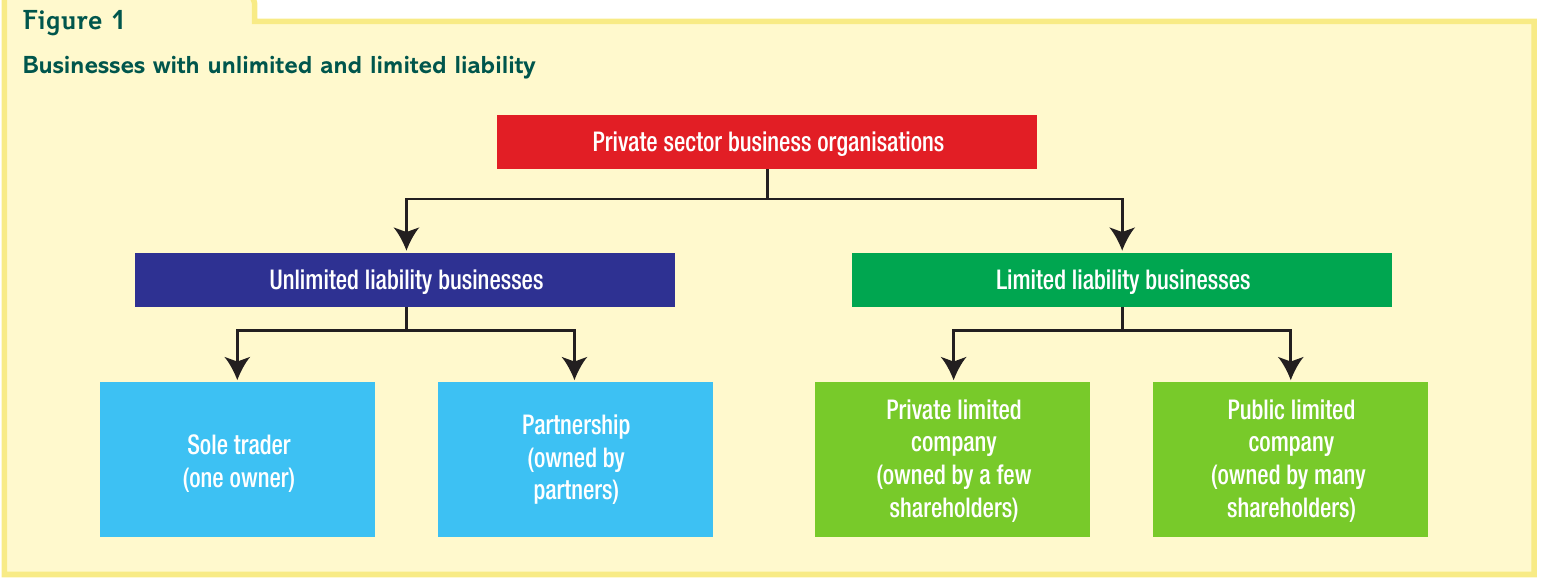

Understanding limited and unlimited liability

The legal status of a business determines whether its owners have limited liability or unlimited liability. This is one of the most important considerations for any business owner, as it directly affects their personal financial risk.

Understanding the difference between limited and unlimited liability is fundamental to business studies. This distinction affects everything from personal financial risk to how businesses can raise finance, and it's determined by whether a business is incorporated or unincorporated.

Unlimited liability businesses

Unlimited liability businesses are organisations where there is no legal difference between the owners and the business itself. These are also called unincorporated businesses because everything is carried out in the name of the owner or owners. The business and the owner are legally treated as the same entity.

These businesses tend to be small and include:

- Sole traders (one owner)

- Partnerships (owned by partners)

Limited liability businesses

Limited liability businesses have a legal identity that is separate from their owners. This means the business itself (not the owners) can be sued, taken over or liquidated. These are also called incorporated businesses.

These businesses include:

- Private limited companies (Ltd) - owned by a few shareholders

- Public limited companies (PLC) - owned by many shareholders

The owners of limited liability businesses are called shareholders, and they benefit from limited liability protection.

Implications of unlimited liability

Financial exposure and personal risk

Business owners with unlimited liability face significant personal financial risk if their business fails. When an unincorporated business collapses while owing money to external parties such as banks, suppliers or tax authorities, the owners must pay these debts using their personal money and assets.

If owners do not have sufficient funds to pay business debts, they can be legally forced to sell personal possessions to raise the necessary cash. For example, a sole trader could be required to sell their house to meet a demand from tax authorities, regardless of the hardship this causes to them and their family.

This creates serious consequences that highlight the substantial risk entrepreneurs take when establishing an unincorporated business. Unlike limited liability businesses, there is no protection for personal wealth - everything the owner possesses is potentially at risk if the business fails.

Worked Example: Understanding Personal Asset Risk

Imagine Sarah runs a sole trader business that owes £150,000 to suppliers and the bank when it fails. Sarah personally has:

- £20,000 in business assets

- £80,000 equity in her house

- £15,000 in personal savings

- A car worth £10,000

Step 1: Calculate the shortfall Business debts = £150,000 Business assets = £20,000 Shortfall = £150,000 - £20,000 = £130,000

Step 2: Identify what Sarah must use Because Sarah has unlimited liability, she must use her personal assets to pay the £130,000 shortfall. This means she could be forced to sell her house and use all her savings and possessions.

This example shows why unlimited liability is considered high-risk for business owners.

Legal liability

Owners of unlimited liability businesses are also liable for any unlawful acts committed by themselves or their employees. For instance, if an employee writes something libellous about someone, that person could claim compensation from the business owner. If the business lacks sufficient funds to pay compensation, the owner must use their personal savings and assets to meet the claim.

Similarly, owners can be held financially liable if sued successfully by other stakeholders, including customers, employees or suppliers. This occurs because there is no separation of legal identity between the business and its owners - they are treated as one and the same in law.

Legal liability extends beyond just financial debts. Owners of unincorporated businesses can be personally liable for damages, compensation claims, and penalties resulting from the actions of their business or employees. This makes professional insurance particularly important for unlimited liability businesses.

Potential advantages

Despite these risks, unlimited liability businesses can sometimes find it easier to raise finance. This is because lenders know they will be reimbursed even if the business defaults, as they can claim against the owner's personal assets.

Unlimited liability businesses are often seen as more credible by lenders and suppliers. This is because owners are encouraged to be more cautious and responsible in their decision-making, knowing their personal assets are at stake if the business fails.

Implications of limited liability

Limited financial risk

The owners of limited liability businesses are shareholders, and they benefit from significant financial protection. The key advantage is that shareholders' financial liability is limited to the amount of money they invested in the business when purchasing shares. This is a fixed sum - shareholders cannot lose more than their initial investment.

If a limited company collapses, the owners' personal assets are fully protected. Shareholders cannot be legally forced to sell personal possessions such as their homes, cars or savings to meet the business's debts. This protection is possible because the business has a separate legal identity from its owners.

The phrase "limited liability" literally means shareholders can only lose what they originally invested. If you buy £5,000 worth of shares in a company, the maximum you can lose is £5,000 - even if the company goes bankrupt owing millions. Your house, car, savings, and other personal possessions remain completely safe.

Protection from legal claims

Shareholders also have protection from legal claims made against the business. Because the owners and the business have separate legal identities, personal liability is avoided. For example, if a customer sues a limited company for damages, the claim can only be made against the business itself. The personal wealth of the company's shareholders cannot be touched if the business cannot pay the compensation.

Worked Example: Comparing Limited and Unlimited Liability

Consider two business owners, Alex (sole trader) and Jordan (shareholder in a Ltd company), both facing business failure:

Alex's situation (Unlimited Liability):

- Business debts: £200,000

- Business assets: £50,000

- Shortfall: £150,000

- Result: Alex must use personal assets to pay the £150,000 shortfall

Jordan's situation (Limited Liability):

- Business debts: £200,000

- Business assets: £50,000

- Shortfall: £150,000

- Jordan's investment in shares: £10,000

- Result: Jordan loses only the £10,000 invested; personal assets are fully protected

This example clearly demonstrates why limited liability is considered much safer for investors and business owners.

Exceptions to limited liability protection

However, there are important exceptions to this protection. Courts can decide that individuals are personally liable in certain circumstances.

Critical Exceptions to Limited Liability Protection:

Limited liability protection can be removed if:

- A crime has been committed

- The company has failed to maintain adequate records and accounts

- The company has not held annual general meetings

- The company has not filed annual reports

These exceptions are more likely to apply to private limited companies, where owners are more directly involved in management. If these conditions occur, shareholders can lose their limited liability protection and become personally liable for company debts.

Raising finance

Because shareholders' personal assets are protected, limited companies often find it easier to raise larger amounts of money from investors. Investors are more willing to buy shares in limited companies because they know precisely the extent of their liability - they can only lose the money they invest in shares, nothing more.

However, in some cases the owners of small limited companies (who are frequently also shareholders) are required to give personal guarantees of the company's debts to lenders. When personal guarantees are given, those specific owners become liable for the debts if the company cannot pay, although other shareholders remain protected.

Personal guarantees are common when small limited companies seek bank loans. While the company has limited liability, banks may require director-shareholders to personally guarantee the loan, effectively making them personally liable if the company defaults. This shows that in practice, limited liability protection isn't always absolute for small businesses.

Choosing appropriate finance based on liability

The liability status of a business influences the finance options available to it. Several factors determine which sources of finance are most appropriate.

Short-term versus long-term finance needs

The time period for which finance is required affects the choice of funding method.

Long-term finance (ten years or more) includes:

- Mortgages - can be taken out for up to 25 years

- Debentures - can be issued for up to 30 years (limited companies only)

- Share capital - money raised from selling shares; this is permanent capital that is never repaid, making it the most long-term method available

Short-term finance (typically under five years) includes:

- Trade credit - payment terms from suppliers

- Bank overdrafts - flexible borrowing up to an agreed limit

- Leasing - renting assets rather than buying

- Unsecured bank loans - typically granted for one to five years

Businesses should match the term of the finance to the time period for which funds are needed.

Matching finance duration to need is crucial for effective financial management. Using short-term finance like overdrafts for long-term investments can create cash flow problems, while using long-term finance for short-term needs means paying unnecessary interest.

Financial position of the business

A business's financial health significantly affects its ability to raise finance. When a business is in a poor financial position, lenders become more reluctant to offer funding, and the cost of borrowing increases. Financial institutions prefer to lend to secure businesses that have substantial collateral (assets that can be used as security for loans).

For unlimited liability businesses, the owner's personal assets effectively act as additional collateral, which can make borrowing easier even if the business itself has limited assets.

Type of expenditure

The nature of the spending influences the appropriate finance source.

Capital expenditure refers to investment in expensive long-term assets. For example, building a new factory would typically be financed by long-term sources such as a share issue (for limited companies) or a mortgage.

Revenue expenditure refers to day-to-day operational spending. For example, purchasing raw materials would typically be funded by short-term sources such as trade credit or a bank overdraft.

Matching Finance to Expenditure Type:

The general principle is to match the life of the asset with the term of the finance:

- Capital expenditure (long-lasting assets) → Long-term finance

- Revenue expenditure (day-to-day costs) → Short-term finance

This approach helps businesses manage their cash flow more effectively and avoid financial strain.

Cost considerations

Businesses prefer sources and methods of finance that minimize costs, both in terms of:

- Interest payments - the cost of borrowing money

- Administration costs - expenses involved in arranging and managing the finance

For example, share issues can carry high administration costs due to legal requirements and regulatory compliance. In contrast, interest payments on bank overdrafts, while potentially having higher interest rates, tend to have lower administration costs.

Limited companies have access to share capital, which provides permanent funding without interest payments (though shareholders expect dividends). Unlimited liability businesses cannot issue shares and must rely on other methods such as loans or personal funds from the owner.

Key Points to Remember:

About Unlimited Liability:

- Unlimited liability means owners are personally responsible for all business debts and can be forced to sell personal assets

- Applies to sole traders and partnerships (unincorporated businesses)

- Owners face significant personal financial risk if the business fails

- May find it easier to raise small amounts of finance because lenders can claim against personal assets

- Owners take substantial personal risk but gain credibility with lenders

About Limited Liability:

- Limited liability means shareholders can only lose their investment amount, with personal assets protected

- Applies to private limited companies (Ltd) and public limited companies (PLC) (incorporated businesses)

- Business has separate legal identity from its owners

- Can raise larger amounts through share issues because investors know their risk is limited

- Exceptions exist: protection can be removed for criminal activity, poor record keeping, or failure to meet legal requirements

Choosing Appropriate Finance:

Choice of finance depends on four key factors:

- Time period needed - short-term versus long-term requirements

- Financial position of the business - affects ability to borrow and cost

- Type of expenditure - capital expenditure needs long-term finance; revenue expenditure needs short-term finance

- Cost - consider both interest payments and administration costs

Essential Terms:

- Unincorporated = no separate legal identity (unlimited liability)

- Incorporated = separate legal identity (limited liability)

- Shareholders = owners of limited companies

- Collateral = assets used as security for loans

- Share capital = permanent finance from selling shares (limited companies only)