Macroeconomic Policies (Edexcel A-Level Economics A): Revision Notes

Policy Objectives

Introduction

Macroeconomic policy success depends on understanding what the policy aims to achieve. This note explores the main objectives of policy at the macroeconomic level and examines potential conflicts between these targets.

Understanding policy objectives is crucial because it helps explain why certain policy actions are taken and allows for better evaluation of their effectiveness. Economic policymakers must constantly balance competing goals while working toward optimal outcomes for society.

When evaluating economic performance, policymakers focus on several key objectives. Understanding these objectives helps explain why certain policy actions are taken and allows for better evaluation of their effectiveness.

The seven key objectives

When considering macroeconomic policy, structure your thinking around these seven objectives:

- Increased economic growth

- A reduction in unemployment

- Control of inflation

- Restoration of equilibrium in the current account of the balance of payments

- Making the distribution of income more equal

- Balancing the government budget

- Protection of the environment

Economic growth

Economic growth represents an increase in the productive capacity of the economy. In simpler terms, this means expanding the potential output that the economy can produce. If society's ultimate aim is to improve citizens' well-being, then economic growth is essential because it widens people's choices by increasing available resources.

Why economic growth matters

Economic growth serves as the most fundamental macroeconomic policy objective. Other policy objectives often depend on achieving sustainable growth, making it the foundation upon which other goals are built.

Economic growth's central role becomes clear when examining how it enables other objectives:

- Low inflation is maintained partly to encourage firms to invest, which enables economic growth

- Full employment ensures the best possible use of society's resources, enabling the economy to reach the production possibility frontier

- Running sustained current account deficits limits future growth prospects by requiring the sale of UK assets

Economists measure economic growth by tracking sustained increases in real GDP over time. Real GDP provides the nearest measure of resources available to members of society.

Exam tip: Remember that 'full' employment does not mean zero unemployment. There will always be some unemployment in any economy due to frictional and structural factors.

Full employment (low unemployment)

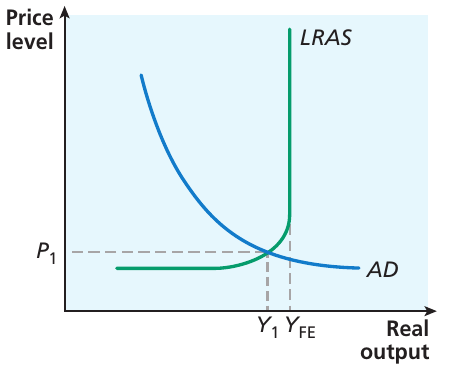

When an economy operates on the production possibility frontier, the factors of production are fully employed. Operating below full capacity represents waste, as surplus capacity could be used productively.

The diagram above shows macroeconomic equilibrium below full employment. The economy operates at output level , which falls below the potential full employment level . This situation means:

- Unnecessary waste of potential output

- Costs for people who are unemployed but could have been productively employed

- The economy could produce more without inflationary pressure

Understanding full employment

Full employment occurs when an economy operates on the production possibility frontier, with full utilisation of factors of production. An economy operating below full capacity is characterised by unemployment.

Price stability

Controlling inflation has been one of the most prominent macroeconomic policy objectives since 1976. Governments focus on price stability because high inflation creates significant economic costs.

Causes of inflation

Cost-push inflation

Inflation represents a rise in the general price level. It's important to distinguish between a one-off increase and a sustained rise over time.

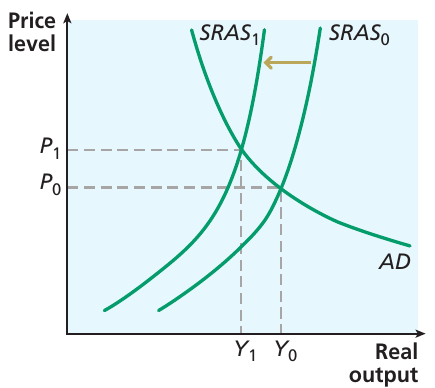

Cost-push inflation is initiated by an increase in the costs faced by firms, arising on the supply side of the macroeconomy. For example:

- A one-off rise in oil prices may affect the price level by shifting aggregate supply

- This shifts the economy to a new equilibrium price level

- If nothing else changes, there's no reason for prices to continue rising beyond this point

The diagram shows how a supply shock (such as an oil price increase) shifts the short-run aggregate supply curve leftward from to . This takes the economy to a new equilibrium price level. The increase in overall prices is cost driven.

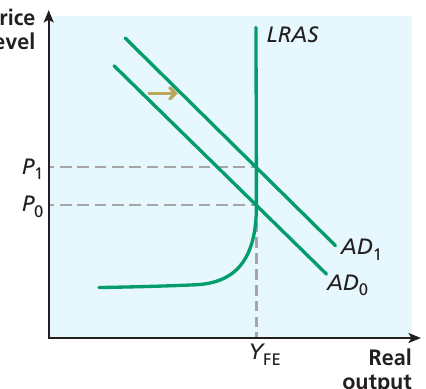

Demand-pull inflation

In terms of the AD/AS model, an alternative explanation comes from the demand side. An increase in aggregate demand leads to a rise in prices, especially if the AS curve becomes steep or vertical in the long run.

Demand-pull inflation is initiated by an increase in aggregate demand. An increase in aggregate demand could come from:

- An expansion of money supply causing interest rates to fall

- Higher consumption and investment expenditure

- Government fiscal stimulus

- Increased exports

The money supply

Persistent increases in prices over time require explanation. One-off movements in either aggregate demand or aggregate supply may lead to one-off changes in the overall price level. However, unless the movements continue in subsequent periods, there's no reason to suppose that inflation will continue.

Money supply refers to the quantity of money circulating in the economy.

Persistent inflation occurs only when the money supply grows more rapidly than real output. This is a critical relationship for understanding sustained inflation.

This can be shown in terms of aggregate demand and aggregate supply:

- If the money supply increases, firms and households find they have excess cash balances

- They have more purchasing power than expected and are holding more money than intended

- Their impulse is to increase spending, causing the aggregate demand curve to move right

- They will probably also save some excess, which tends to result in lower interest rates

- Lower rates reinforce the increase in aggregate demand

- As the AD curve moves right, the equilibrium price level rises, returning the economy to equilibrium

If the money supply continues to increase, the process repeats itself, with prices rising persistently. People get accustomed to the process and speed up their spending decisions, accelerating the whole process.

Costs of inflation

High inflation creates several significant costs for society and reduces the effectiveness of markets.

Menu and shoe-leather costs

When inflation is relatively high, firms must keep amending their price lists, raising the costs of undertaking transactions. These costs are known as menu costs of inflation. However, these should not be significant unless inflation is very high.

A second cost of high inflation is that it discourages people from holding money. At very high nominal interest rates that occur when inflation is high, the opportunity cost of holding money becomes great. People therefore try to keep their money in interest-bearing accounts for as long as possible, making frequent trips to the bank. These are known as shoe-leather costs of inflation.

The spread of online banking has made it easier for people to shift funds between savings and current accounts rather than needing to visit the bank in person. This has contributed to the closure of many bank branches. However, the effect of very high inflation on the opportunity cost of holding money remains.

Case Study: Argentina's Hyperinflation Crisis (2022)

In August 2022, Argentina's central bank raised the official interest rate to 69.5% in an attempt to curb inflation. In July, monthly inflation had reached 7%, and bartering fairs were operating where unemployed women set out blankets on the ground, hoping to exchange household goods for food. The economy minister pledged to stop printing money to fund government expenditure.

Ineffective markets

High inflation may inhibit the effectiveness of markets. Markets will not work effectively when people do not use money and the economy begins to slip back towards a barter economy. The situation worsens if:

- Taxes or pensions are not properly indexed to keep up with inflation

- Tax revenue fails to keep up with government expenditure, forcing authorities to print more money to finance spending plans

- Those on fixed incomes (such as some pensions) lose out, worsening income inequality

These costs are felt mainly when inflation reaches the hyperinflation stage. This has been rare in developed countries in recent years, although many Latin American economies were prone to hyperinflation during the 1980s, and some transition economies experienced very high inflation as they began to introduce market reforms.

Case Study: Hyperinflation in Ukraine and Zimbabwe

Ukraine reached 10,000% per year inflation in the early 1990s. Zimbabwe's inflation became almost impossible to measure because it was so rapid. The BBC claimed that inflation had reached 231,000,000% in 2008, with printing presses having difficulty keeping up with the need for bank notes.

Uncertainty

Even when inflation doesn't reach extreme heights, costs may still arise, especially if inflation is volatile. If firms cannot confidently predict the rate of price changes, the increase in uncertainty may be damaging. Firms may become reluctant to undertake investment that would expand the economy's productive capacity, which is crucial for economic growth.

Unreliable price signals

Prices are very important in allocating resources in a market economy. Inflation may consequently inhibit the ability of prices to act as reliable signals in this process, leading to wastage of resources and lost business opportunities.

Study tip: The key costs of inflation are:

- Menu costs

- Shoe-leather costs

- Reluctance to use money for transactions

- Redistribution of income away from those on fixed incomes

- Uncertainty reduces incentives for investment

- Prices fail to be reliable signals for resource allocation

The inflation target

The control of inflation became central to UK government macroeconomic policy due to concerns with investment incentives and the failure of prices to act as reliable signals. However, the target for inflation has not been set at zero.

During the period when the inflation target was set in terms of RPIX, the target was 2.5%. From 2004, the target for CPI inflation became 2%. The reasoning is twofold:

- Measured inflation will overstate actual inflation, partly because it's difficult to account for quality changes in products (such as PCs or smartphones)

- Wages and prices tend to be sticky in a downward direction - firms may be reluctant to reduce prices and wages

A modest rate of inflation (e.g. 2%) allows relative prices to change more readily, with prices rising by more in some sectors than others. This helps price signals to be more effective in guiding resource allocation.

In the UK over the last 20 or 30 years, inflation has been at relatively modest levels. When prices began to accelerate in 2022, inflation suddenly gained renewed attention. The rapid onset of higher inflation stemmed from the economy's recovery from the pandemic, reinforced by interruptions to oil and gas supplies at the time of the Ukrainian war. Both demand-side and supply-side factors were at work.

The balance of payments

Maintaining equilibrium on the current account is identified as a key objective of macroeconomic policy, although it's less obvious why this should be important compared with economic growth, controlling inflation or unemployment.

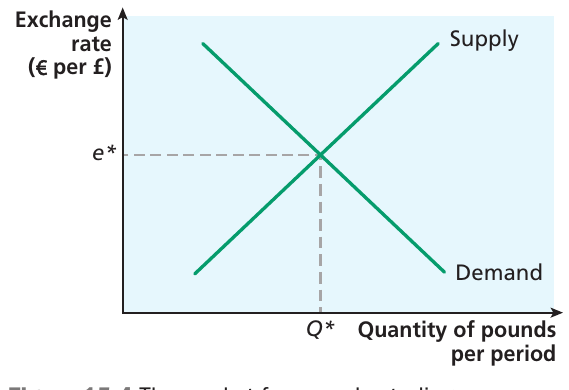

The diagram shows the market for pounds relative to euros. The demand for pounds arises from residents in the Eurozone wanting to buy UK goods, services and assets. The supply arises from UK residents wanting to buy goods, services and assets from the Eurozone.

The role of exchange rates

In a free foreign exchange market, the exchange rate can be expected to adjust to bring about equilibrium. Even under a fixed exchange rate system in which the government pledges to hold the exchange rate at a particular level, any discrepancy between demand for and supply of pounds would be met by the monetary authorities buying or selling foreign exchange reserves. Thus, the overall balance of payments is always in equilibrium.

Why balance of payments matters

The problem arises not with the overall balance of payments, but with an imbalance between components of the balance of payments. Attention focuses on the balance of the current account, which shows:

- The balance of trade in goods and services

- Investment income flows

- Current transfers

A deficit on current account

If the current account is in deficit, UK residents are spending more on imports of goods and services than the economy is exporting. Another way of expressing this is that UK earnings from exports are not sufficient to pay for UK imports. This is like a household spending beyond its income, which can be sustained only by selling assets or by borrowing.

The concern is that a large and sustained deficit on the current account implies that the financial account must also be experiencing a large and sustained surplus. This means:

- The UK is effectively exporting assets

- Overseas residents are buying up UK assets

- This may mean a leakage of investment income in the future

- Overall balance could be achieved through the sale of foreign exchange reserves, soaking up the excess supply of pounds

However, a large deficit cannot be sustained indefinitely. This raises questions about what constitutes a 'large' deficit.

UK Context: Current Account Trends

The current account has been in deficit every year since 1984, although the deficit has been a relatively small proportion of GDP. The 2010s saw a significant increase in the size of the deficit. The initial effect of the financial crisis that began in the late 2000s was a reduction in the current account deficit to 2.4% of GDP in 2011. However, the deficit increased, reaching 5.5% in 2016 (the highest since records began in 1946). According to the ONS, this was partly attributable to a decline in investment income from abroad. Since then, with interruptions to trade caused by Brexit and the COVID-19 pandemic, the deficit fell relative to GDP, reaching 2.0% in 2021.

Investment from abroad

A critical issue is whether UK assets remain attractive to buyers in the rest of the world. Running a sustained deficit on the current account requires running a surplus on the financial account. If overseas buyers of UK assets become reluctant to buy, UK interest rates might have to rise to make UK assets more attractive.

A by-product would be a curb in spending by UK firms and consumers. Given that part of this reduction in spending would affect imports, this would begin to reduce the current account deficit.

Policy implications

The balance of payments is important from a policy perspective when a government wishes to stimulate the economy, perhaps because it regards unemployment as excessive. An expansionary policy may be intended to increase domestic aggregate demand. However, in designing such a policy, it's vital to remember that some of the increased demand will go not on domestic goods, but on imports, which dilutes the effect of the expansion.

Causes of a deficit on current account

The quantity of exports of goods and services from the UK depends partly on:

- Income levels in the rest of the world

- The competitiveness of UK goods and services (which depends partly on the sterling exchange rate and partly on relative prices in the UK and elsewhere)

Similarly, the level of imports depends partly on:

- Domestic income

- The relative international competitiveness of UK goods and services

A fundamental cause of a deficit on the current account is a lack of competitiveness of UK goods and services, arising from:

- An overvalued exchange rate

- High relative prices of UK goods and services

- UK incomes rising more rapidly than those in the rest of the world

A balanced government budget

The financial crisis of the late 2000s focused attention on the government budget position. If the government spends more than it raises in revenue, the resulting deficit must be financed in some way.

Key terms

Public sector net cash requirement (PSNCR): the difference between public sector spending and revenues (also known as the government deficit). Part of the PSNCR is covered by borrowing, and the government closely monitors its net borrowing.

Net debt: the accumulation of past borrowing.

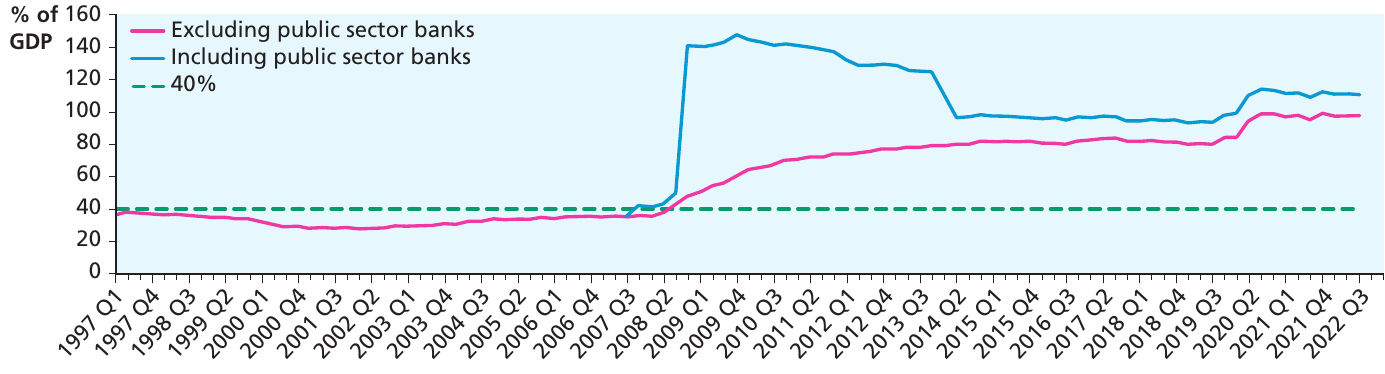

The Labour government in power from 1997 to 2010 aimed to keep net debt below 40% and was successful in achieving this until the financial crisis hit.

The debt debate

A major argument in favour of controlling the level of public sector net debt arose from concern for the long-run effects of policy on spending and borrowing. It was argued that sustainable economic growth must take into account the needs of future generations.

The Labour government took the view that:

- Current spending should be met out of current revenues

- Only investment for the future should be met through borrowing

- Future generations should not have to meet the cost of the consumption of the present population

Impact of financial crisis

While public sector debt was stable at less than 40% of GDP, it was not seen as being of major concern. However, the financial crisis led to a refocusing of macroeconomic policy.

The diagram shows the impact of the crisis on public sector net debt in the UK. The crisis manifested in the banking system, beginning with the failure of Northern Rock in 2008, followed by problems in other commercial banks. The bailout needed to safeguard the financial system led to an enormous increase in public sector net debt, evident in the figure above.

Key observations:

- The government's stake in bailed-out banks has been gradually reduced

- Public sector debt has remained at more than 80% of GDP

- The need to bring down the level of debt has influenced policy design

COVID-19 impact

The measures taken to safeguard the economy during the COVID-19 pandemic pushed up public sector borrowing again. By the end of 2021, public sector net debt stood at 112.7% of GDP. While interest rates remained relatively low, such high levels of debt might be tolerated, as interest repayments on the debt would also be low.

However, during 2022 inflation began to accelerate. In response, the Bank of England began to raise interest rates. If sustained, this would mean an increase in debt repayments, which would carry an opportunity cost, leaving less funding for other public sector expenditures.

Concern for the environment

International externalities pose problems for policy design because they require coordination across countries. Examples include:

- If pollution caused by the UK manufacturing sector creates acid rain elsewhere in Europe, the UK imposes costs on other countries not fully reflected in market prices

- Effects felt across generations - if the environment today is damaged, it may not be enjoyed by future generations (intergenerational externality effects)

Growing concerns about global warming have drawn attention to possible harm caused by rapid economic growth. The relationship between the environment and economic growth has highlighted the macroeconomic dimension to environmental concern, leading to growing calls for growth to be sustainable.

Income redistribution

The final macroeconomic policy objective concerns attempts to influence the distribution of income within society. These may involve:

- Transfers of income between groups in society (from richer to poorer)

- Progressive taxation (whereby those on high incomes pay a higher proportion of their income in tax)

- A system of social security benefits such as Universal Credit

Causes of inequality

Some degree of inequality in income distribution is inevitable. People have different innate talents and abilities, and choose to undergo different types and levels of education and training, acquiring different sets of skills. Market forces imply that different payments will be made to people in different sectors of economic activity and different occupations.

Income inequality also arises because of inequality in the ownership of assets. However, people in identical circumstances and with identical skills and abilities may receive identical income. This notion is known as horizontal equity, which most people would agree is desirable.

Policy approaches

One category of policy measures is designed to encourage horizontal equity. Equal opportunities legislation tries to ensure that members of society do not suffer discrimination that might deny them:

- Equal pay for equal work

- Equal access to employment

Nonetheless, significant differences remain in earnings and employment between ethnic groups and between men and women.

The image shows women demonstrating for equal pay in London in 2014, highlighting that significant differences in earnings between men and women persist.

The costs of inequality

In a society where there is substantial inequality in income distribution, there are likely to be groups of people who are disadvantaged in various ways. For example:

- They may find it more difficult to obtain education for themselves or their children

- Lower proportions of students from low-income families go to university

- Potential entrepreneurs may find it more difficult to obtain credit needed to launch business ideas

This suggests that there are people in society who are inhibited from developing their productive potential, which in turn implies that economic growth in the future will be lower than it could be. This could provide justification for redistributing income, or at least for trying to ensure equality of opportunity for all members of society.

However, redistribution can be taken too far. If higher-income groups face too high a marginal tax rate on their income, this could remove their incentive to exploit income-earning opportunities, which could have a damaging impact on economic growth. Getting the right balance between protecting the vulnerable and providing appropriate incentives for enterprise is a tricky task for policy-makers.

Too much inequality may also lead to:

- High crime rates

- Social discontent

- Political instability

- Threats to property rights security

- Inhibited economic growth

There is evidence that inequality has been widening in many countries in recent years. In particular, the way that technology has been progressing places a higher premium on skills, so that the gap between the earnings of skilled and unskilled workers has been widening.

Key Points to Remember:

-

Seven key objectives: Economic growth, low unemployment, price stability, balance of payments equilibrium, balanced government budget, environmental protection, and income redistribution guide macroeconomic policy.

-

Economic growth is fundamental: It expands productive capacity and widens choices for citizens, making it the foundation for other macroeconomic objectives.

-

Inflation control is central: Since 1976, controlling inflation has been a major focus because high inflation creates menu costs, shoe-leather costs, uncertainty for investment, and unreliable price signals.

-

Balance of payments matters: A sustained current account deficit means the UK is effectively exporting assets or accumulating debt, which cannot continue indefinitely without consequences for future growth.

-

Government debt requires careful management: While some borrowing is acceptable for investment, excessive debt accumulation creates burdens for future generations and limits policy flexibility, especially when interest rates rise.