Fiscal and Monetary Policy (Edexcel A-Level Economics A): Revision Notes

Fiscal and Monetary Policy

Introduction to macroeconomic policy instruments

Governments have three main types of policy instruments available to achieve their macroeconomic objectives. These policies are designed to address issues such as economic growth, unemployment, inflation, and the balance of payments.

The three key policy instruments are:

-

Fiscal policy: Government decisions about spending, taxation, and borrowing that affect aggregate demand in the economy.

-

Monetary policy: The use of monetary variables such as the money supply and interest rates to influence aggregate demand. Under fixed exchange rate systems, monetary policy must focus on maintaining the exchange rate.

-

Supply-side policies: Measures that directly impact the productive capacity of the economy by affecting aggregate supply. These can be microeconomic in nature and are designed to increase output and promote economic growth.

The effectiveness of each policy depends significantly on the broader policy environment in which it operates and the relationships between the different types of policy. These three instruments often work together and can reinforce or counteract each other's effects.

Fiscal policy

What is fiscal policy?

Fiscal policy refers to decisions made by the government regarding its expenditure, taxation, and borrowing. An expansionary fiscal policy involves increasing government spending or reducing taxes, which shifts the aggregate demand curve to the right.

Fiscal policy operates primarily on the demand side of the economy. When the government increases its spending or cuts taxes, this directly affects the level of aggregate demand, which in turn influences economic activity, employment, and the price level.

Government expenditure and the multiplier effect

Government spending covers a wide range of goods and services. Major expenditure areas include:

- The National Health Service (NHS)

- Education

- Infrastructure projects (such as the Elizabeth line or HS2)

These infrastructure projects are particularly important as they facilitate long-term economic growth by improving the productive capacity of the economy. They not only boost demand in the short run but also enhance the economy's supply-side capabilities in the long run.

The Elizabeth line, which opened in 2022, is an example of government infrastructure investment designed to support economic growth.

When government expenditure increases, it acts as an injection into the circular flow of income. This triggers the multiplier effect, which amplifies the initial impact on aggregate demand. The strength of the multiplier depends on the size of withdrawals from the circular flow. If consumers have a high marginal propensity to import, the multiplier effect will be weaker.

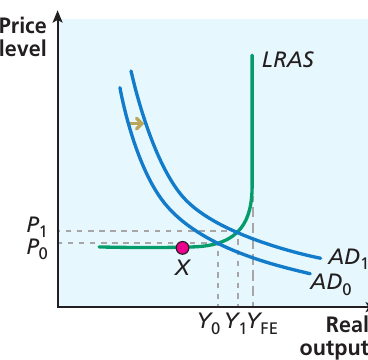

Understanding the Fiscal Policy Mechanism

The diagram above illustrates how fiscal policy works through the AD/AS model:

Initial Position:

- Macroeconomic equilibrium occurs at the intersection of the long-run aggregate supply curve (LRAS) and the initial aggregate demand curve (AD₀)

- Real output is at Y₀, which is below the full employment level YFE

After Government Expenditure Increases:

- The AD curve shifts rightward from AD₀ to AD₁

- The overall price level rises to P₁

- Real output increases to Y₁, which is closer to the full employment level YFE

Key Insight: The increase in government expenditure raises the real output level in the economy, although some of the increase is dissipated through a rise in the overall price level. This happens because the initial equilibrium is on the upward-sloping section of the Keynesian LRAS curve (between point X and YFE).

The importance of aggregate supply

Fiscal policy is only effective in increasing real output if the aggregate demand curve intersects the aggregate supply curve below full employment. If the economy is already operating at the full employment level of output, an increase in aggregate demand will merely result in higher prices without any increase in real output. This would also occur with a vertical (monetarist) LRAS curve.

The effective use of fiscal policy requires policymakers to have accurate information about the current state of the economy. They need to know whether the economy is operating at or below full employment. Without this knowledge, there is a danger that expansionary fiscal policy will lead to price increases without significantly affecting output, particularly if the LRAS curve is relatively steep.

Common Pitfall: If AD intersects LRAS in the vertical segment, expansionary fiscal policy will only cause inflation, not growth. Understanding where the economy is positioned relative to full employment is crucial when evaluating whether fiscal policy will be effective.

The impact on the balance of payments

When aggregate demand increases, part of this increase is likely to be spent on imports. However, there is no immediate reason for exports to change. In the short run, therefore, an increase in aggregate demand is likely to worsen the current account deficit on the balance of payments.

Taxation and the government budget

Although much discussion of fiscal policy focuses on government expenditure, taxation is equally important. The key issue in considering overall fiscal policy is the government budget deficit (or surplus), which is the balance between government expenditure and government revenue.

An increase in the government budget deficit (or a decrease in the government budget surplus) moves the aggregate demand curve to the right. The budget deficit may arise either from an increase in expenditure or from a decrease in taxation, although these have some differential effects.

Key Distinction

A government budget deficit occurs when government spending (G) is greater than tax revenue (T).

A surplus occurs when T is greater than G.

When evaluating fiscal policy situations, always compare government expenditure with revenue from taxation to determine whether a deficit or surplus exists.

Direct and indirect taxes

Fiscal policy, and taxation in particular, serves multiple purposes beyond establishing a balance between the public and private sectors. Taxation is an important tool for:

- Addressing market failures

- Influencing the distribution of income

The choice between direct and indirect taxes has significant implications for these objectives.

Direct taxes are levied on income of various kinds, such as personal income tax. Income tax can be effective in redistributing income when structured as a progressive tax, where higher income tax rates are charged to those earning higher incomes.

Indirect taxes are taxes on expenditure, such as VAT and excise duties. These tend to fall more heavily on those with lower incomes. Poorer households spend a higher proportion of their income on items subject to excise duties, so a greater share of their income is taken through indirect taxes (making them regressive taxes). VAT can have similar effects if higher-income households save a greater proportion of their incomes.

Indirect taxes can be targeted at specific instances of market failure:

- High excise duties on tobacco are designed to discourage consumption due to significant negative externality effects

- High duties on petrol address environmental concerns related to greenhouse gas emissions

This demonstrates how fiscal policy can serve both economic stabilisation and social policy objectives.

Fiscal policy in the UK

When the government spends more than it raises in revenue, the resulting deficit must be financed. The government borrows by issuing financial assets such as Treasury bills or gilt-edged securities. When the deficit is covered by borrowing, the result is an accumulation of public sector net debt.

The global financial crisis led to a substantial increase in public sector net debt in the late 2000s, and debt rose further during the COVID-19 pandemic. This massive increase in debt required a rethinking of fiscal policy, with decisions needed about reducing outstanding debt levels to ensure spending remained sustainable.

The Autumn Statement issued in November 2022, after Rishi Sunak's appointment as prime minister, announced increases in taxes and cuts in government expenditure to help control inflation while also contributing to reducing the national debt.

Balance between public and private sectors

Even if the size of the budget deficit limits the government's fiscal policy options, decisions must still be made about the overall balance of activity in the economy. A neutral government budget can be achieved either with high expenditure and high revenues, or with relatively small expenditure and revenues. These decisions affect the overall size of the public sector relative to the private sector.

Over the years, different UK governments have taken different positions on this issue, and different countries throughout the world have adopted varying approaches. Such decisions are often determined through elections, where political parties present their plans for taxation and spending, and voters give a mandate to the party offering a package that most closely matches their preferences.

Monetary policy

What is monetary policy?

Monetary policy involves decisions made by the government regarding monetary variables such as the money supply or the interest rate. This approach has been favoured by the UK government to stabilise the macroeconomy in recent decades. Monetary policy uses these variables to influence aggregate demand.

It is important to understand that controlling money supply and interest rates cannot be done simultaneously and independently. Firms and households choose to hold some money for transactions or as a precaution against unexpected needs. In doing so, they incur an opportunity cost – they forgo the possibility of earning interest by purchasing financial assets instead.

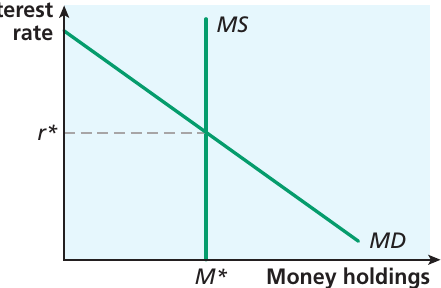

Money and the interest rate

The interest rate can be regarded as the opportunity cost of holding money. In other words, it is the price of holding money. At high interest rates, people choose to hold less money because the opportunity cost is high.

The money demand curve (MD) shown above is downward sloping, illustrating that the quantity of money people want to hold decreases as the interest rate increases. The money supply (MS) is shown as a vertical line, as it is set by the government.

Suppose the government wants to set the money supply at M* in the diagram. This can be achieved in two ways:

-

The government controls the supply of money at M*, and equilibrium is achieved when the interest rate adjusts to r*.

-

The government sets the interest rate at r* and allows the money supply to adjust to M*.

Critical Policy Choice

The government can choose one or the other approach, but it cannot set both money supply at M* and hold the interest rate at any value other than r* without causing disequilibrium.

A practical problem with attempting to control money supply directly is that the complexity of the modern financial system makes it difficult to precisely define or measure money. For this reason, the chosen instrument of monetary policy is the interest rate.

Monetary policy and aggregate demand

Through the interest rate, monetary policy affects aggregate demand. At higher interest rates:

- Firms undertake less investment expenditure

- Households undertake less consumption expenditure

This occurs partly because borrowing becomes more expensive when interest rates are high, discouraging borrowing for investment or consumption. There are also reinforcing effects through the exchange rate: if UK interest rates are high relative to elsewhere, the exchange rate rises, reducing the competitiveness of UK goods and attracting inflows of financial capital ('hot money').

This interaction between money supply, interest rates, and the exchange rate makes policy design complicated. Changes in one variable inevitably affect the others, creating both intended and unintended consequences that policymakers must carefully consider.

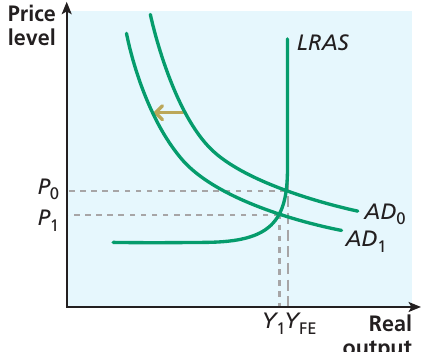

Contractionary Monetary Policy in Action

Suppose the government believes the economy is close to full employment and is in danger of overheating, potentially pushing prices up without any resulting benefit in terms of higher real output. An increase in the interest rate will reduce aggregate demand, thereby relieving pressure on prices.

Initial Position:

- Aggregate demand is relatively high at AD₀

- Real output is at the full employment level YFE

- Overall price level is at P₀

After Interest Rate Increase:

- Aggregate demand shifts leftward to AD₁

- Real output falls slightly to Y₁ (slightly below full employment)

- Equilibrium price level falls to P₁

This demonstrates how monetary policy can be used to control inflationary pressures in an economy operating near full capacity.

Monetary policy in the UK

Almost all countries have a central bank, which fulfils a range of roles, including:

- Being banker to the government

- Issuing coins and banknotes

- Acting as banker to commercial banks

- Regulating the financial system

In the UK, this role is performed by the Bank of England.

Independence and Credibility

Since 1997, responsibility for monetary policy has been devolved to the Bank of England, which was given the task of achieving the government's inflation target. This target was initially set at 2.5% for RPIX inflation, but was amended in 2004 to 2% per annum as measured by the CPI.

This independence was granted to increase the credibility of monetary policy and remove short-term political pressures from interest rate decisions.

The Monetary Policy Committee (MPC)

According to this arrangement, the Monetary Policy Committee (MPC) of the Bank of England sets interest rates in such a way as to keep inflation within 1 percentage point (either way) of the 2% target for CPI inflation. If the MPC fails to achieve this, the Bank must write an open letter to the Chancellor of the Exchequer explaining why the target has not been met. Such a letter became necessary for the first time in March 2007, when CPI inflation reached 3.1%.

Operationally, the MPC sets the interest rate it pays on commercial bank reserves. This is known as Bank Rate. Commercial banks use this rate as their base rate, from which they calculate the interest rates they charge to borrowers. When the MPC changes Bank Rate, commercial banks soon adjust the rates they charge to borrowers. These rates vary according to the riskiness of loans – for example, credit cards are charged at a higher rate than mortgages – but all rates are linked to the base rate set by commercial banks, and hence indirectly to Bank Rate set by the Bank of England.

Key Terms: UK Monetary Policy

-

Central bank: The banker to the government, performing functions including issuing currency, acting as banker to commercial banks, and regulating the financial system

-

Bank of England: The UK's central bank

-

Monetary Policy Committee (MPC): The body within the Bank of England responsible for conducting monetary policy

-

Bank Rate: The interest rate set by the MPC of the Bank of England to influence inflation

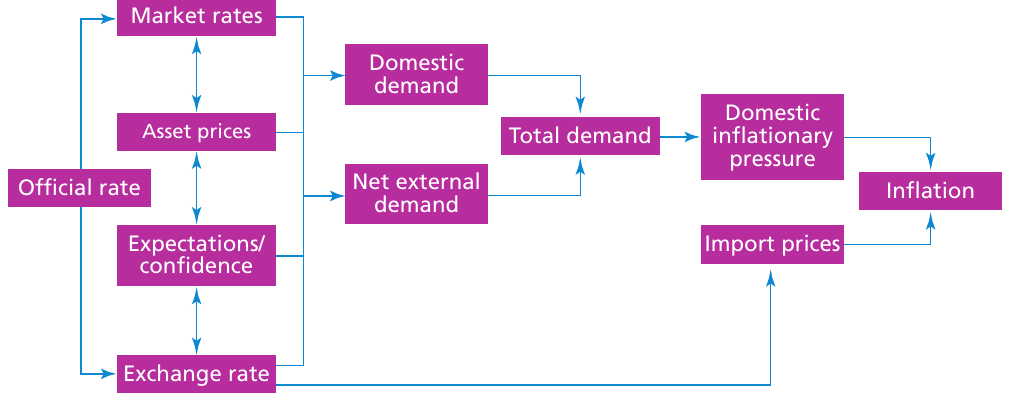

The transmission mechanism of monetary policy

The transmission mechanism of monetary policy describes the process by which a change in Bank Rate affects inflation. The Bank of England sets the official Bank Rate, which affects both market rates of interest and the exchange rate. These in turn influence other asset prices and expectations about the future, affecting the degree of confidence among economic agents.

These factors then affect both domestic demand and net external demand, which together determine total demand and hence aggregate demand. An increase (decrease) in aggregate demand puts upward (downward) pressure on prices, affecting the amount of domestic inflationary pressure. At the same time, changes in the exchange rate affect import prices, which also influence inflation.

Complexity and Time Lags

As you can see, there is a long and complicated chain of linkages that enables a change in monetary policy to affect inflation. This complexity means that the effects of a change in Bank Rate are not likely to be felt immediately.

Question to consider: Would an increase in interest rates lead to a leftward or rightward shift of the AD curve?

Answer: Leftward, as it reduces consumption and investment, thereby decreasing aggregate demand.

MPC meetings and decision-making

At typical meetings, the MPC discusses:

- Financial market developments

- The international economy

- Money, credit, demand and output

- Costs and prices

The inflation target is considered within the broad context of developments in various aspects of the economy. All these factors are discussed in detail before a decision on Bank Rate is taken. In the interests of transparency, the minutes of regular MPC meetings are published on the internet, allowing the public to check recent developments in the economy.

The underlying principle is that by influencing the level of aggregate demand, the MPC can affect the rate of inflation to keep it within the target range. However, the effects of a change in Bank Rate are not immediate. A key reason for giving the Bank of England independence was to increase the credibility of monetary policy. When firms and households realise the government is serious about controlling inflation and have confidence in its actions, they are better able to form expectations about the future path of the economy. This encourages firms to undertake more investment, which has a supply-side effect, shifting the aggregate supply curve to the right in the long run.

UK monetary policy: 2004 to 2007

Inflation remained within the 1% band around the 2% target from 1997 through until March 2007. During this period, the relationship between Bank Rate movements and inflation was not easy to distinguish, partly because this relationship is obscured by other influences. The MPC takes into account a wide range of factors when deciding whether to move Bank Rate or leave it unchanged.

When inflation began drifting towards 3% in early 2007, Bank Rate was increased in an attempt to bring inflation down. This did happen during 2007, with inflation coming back down to around 2%.

Monetary policy from 2008

From 2008 onwards, circumstances changed significantly. Inflation accelerated during 2008, but the MPC considered this was likely to be a temporary surge. The financial crisis was beginning to affect the economy, with many commercial banks finding themselves in trouble and being bailed out. The MPC was aware that credit in the economy was tight.

Instead of raising Bank Rate to curb inflation, the MPC reduced Bank Rate. By early 2009, Bank Rate had reached 0.5%, which was almost as low as it could go.

Quantitative easing

With the economy heading into recession, reducing Bank Rate to boost aggregate demand was no longer an option. The Bank of England turned to a policy that became known as quantitative easing (QE).

Quantitative easing is a process by which liquidity in the economy is increased when the Bank of England purchases assets from banks.

How Quantitative Easing Works

The Problem: Banks make their money by lending out deposits they receive from savers. During the financial crisis, the amount of money being saved in banks was increasing, but banks were reluctant to lend it to households or businesses that could become bankrupt and fail to repay loans. Instead, banks wanted to lend to the UK government by buying government bonds, knowing the government was borrowing heavily but had never defaulted on a loan.

The Solution: The government worked with the Bank of England to develop quantitative easing:

Step 1: The Bank of England created electronic money

Step 2: The Bank used this money to buy government and commercial bonds from banks

Step 3: Banks could no longer buy government bonds in the same quantities and had to consider lending to firms again

The Result: The process of QE helped to increase liquidity in the banking sector by increasing the amount of money in circulation, lowering interest rates on government and commercial bonds, which fed through to household lending. Banks were left with no alternative but to use their accumulated savings to lend to firms and households instead of the government.

By August 2022, the Bank of England held £875 billion of government debt and £20 billion of commercial debt, although it was considering reversing QE, known as 'quantitative tightening'.

The Bank of England's asset purchases work through several channels:

- Confidence: Giving economic agents confidence that action is being undertaken

- Policy signalling: Providing clear signals of policy intent

- Portfolio rebalancing: Encouraging rebalancing of portfolios and providing market liquidity

- Money: Increasing the money supply

- Market liquidity: Improving overall market functioning

- Bank lending: Encouraging banks to lend more

The QE Transmission Process

These channels affect asset prices and the exchange rate, as well as spending and income. This impacts total wealth and the cost of borrowing. The improvement in confidence affects asset prices and the exchange rate, as well as spending and income, which could also affect inflation.

The initial impact of asset purchases gives agents confidence that action is being taken and provides clear policy signals. This encourages portfolio rebalancing, provides market liquidity, and increases money supply. The improvement in confidence, asset prices, and the exchange rate affects spending and income. These effects work together to reinforce the impact on asset prices and the exchange rate, with the increase in money supply operating through bank lending. The adjustment in asset prices and the exchange rate affects total wealth and the cost of borrowing, in turn affecting spending and income.

In this way, monetary policy can be used to mitigate the effects of recession, even with Bank Rate at its lowest point. The key element is providing sufficient credit to allow the economy to function more effectively.

The late 2010s

The UK's recovery from recession was slow. Real GDP growth remained stubbornly below trend. Inflation fell below the target range in 2015 and 2016, even turning negative in some months. In August 2016, the MPC cut Bank Rate to 0.25% in an attempt to bring inflation back towards the target, recognising the weakening prospects for growth following the EU referendum result.

Inflation gradually moved back into the target range. In late 2017, the MPC brought Bank Rate back up to 0.5% as inflation hit the top of its target range. Bank Rate was raised to 0.75% in August 2018, and by 2019 inflation was again close to its 2% target.

COVID-19 and inflation

The COVID-19 pandemic hit the UK in early 2020. The country went into lockdown and many workers were furloughed. GDP fell and supply chains were disrupted. Aggregate demand fell significantly.

The leftward shift in aggregate demand put downward pressure on the overall price level, and real output fell. The effect of this was to reduce inflation, which by August 2020 had reached just 0.18%.

In March 2020, the Bank of England reduced Bank Rate to 0.1%, the lowest level ever recorded. During 2021, as the pandemic's effects began to withdraw and the economy began to recover, inflation started to accelerate, reinforced by fuel prices and transport costs. Bank Rate was increased to try to mitigate this impact, reaching 2.5% in December 2022, with little apparent impact at that stage.

Evaluation of demand-side policies

Both fiscal and monetary policy operate through the demand side of the economy, affecting the position of the AD curve to influence the economy's path. Whether intervention is needed in response to an external shock depends on whether the economy adjusts rapidly back to equilibrium at the natural rate, or whether the adjustment process can be prolonged and persistent.

Coping with the financial crisis

The financial crisis represented one of the greatest external shocks to hit developed economies since the Second World War. How effective were demand-side policies in responding to the crisis?

In both the UK and the USA, a combination of fiscal and monetary policy measures were introduced:

Fiscal policy: Governments launched fiscal stimulus packages involving increased expenditure. In the UK, the government also introduced changes to direct taxes and implemented a temporary reduction in the VAT rate. The strength of this approach is that measures take effect quickly and help safeguard employment. However, the downside is that running a budget deficit adds to public sector net debt, as expenditures need to be financed.

Monetary policy: This was also used to stimulate aggregate demand, with cuts in interest rates and quantitative easing designed to stimulate demand. The need to bail out failing banks further added to public sector debt.

Economic growth was restored in both the UK and the USA, although growth remained below the long-run trend value.

The message from AD/AS analysis is that stimulating aggregate demand is not a solution for long-run economic growth, except insofar as it involves investment expenditure that adds to a nation's productive capacity. Although demand-side policy measures during the financial crisis may have cushioned the impact in the short term, in the long run it is supply-side policies that restore economic growth.

The Great Depression of the interwar years

Some parallels can be drawn with the Great Depression between the two world wars. A stock market crash in New York in 1929 spread rapidly to the UK. World trade contracted and unemployment in the UK rose to 3 million.

Unemployment rose after the First World War, and the recovery process was slow. Unemployment throughout much of the 1920s was around 10%. However, this increased dramatically as the depression took hold, only falling below early 1920s levels as the Second World War approached.

A Lesson in Policy Mistakes

The government of the day was committed to classical economic ideas and was determined to maintain balance in the government budget. To achieve this, it cut government spending. The prevailing theory suggested that unemployment would only fall if labour costs were reduced, encouraging employers to hire labour. Wage cuts were encouraged.

The Result: These measures reduced aggregate demand, causing the economy to fall further into depression.

It was in this context that Keynes published his General Theory, which highlighted the multiplier effects of autonomous spending and suggested that a boost to aggregate demand could assist recovery. This debate was renewed in the late 2000s, when some commentators argued for cuts in public expenditure to reduce the burden of public sector debt, while others advocated a stimulus to aggregate demand to speed recovery.

In the USA, a different approach was adopted. President Roosevelt launched his 'New Deal' in 1933, a substantial fiscal expansion programme designed to improve the country's infrastructure and bring people into employment. Unemployment had peaked at 23.6% in 1932, but by 1938 it was still relatively high at 19.0%, so the extent to which the fiscal expansion had an effect is not entirely clear. Spending on the Second World War may have been the decisive factor, as unemployment in 1942 was down to 4.7%.

Question for Consideration:

How would the onset of the Second World War have affected aggregate demand?

Answer: It would have caused a significant rightward shift in AD due to increased government spending on the war effort, including military equipment, supplies, personnel, and the overall war economy.

The COVID-19 pandemic

The UK government's response to the COVID-19 pandemic made use of both fiscal and monetary policy. With the virus spreading rapidly through the population, extreme measures were needed.

Fiscal measures:

A high priority as the pandemic took hold was to protect the National Health Service (NHS) and tackle the virus. This required spending on healthcare infrastructure, such as the Nightingale Hospitals (pop-up hospitals in exhibition halls like the ExCeL in East London and the SEC in Glasgow), and on equipment and medical staff. There was also high spending on vaccine development.

To protect the economy, support for businesses was urgently needed, as restrictions imposed on their operations meant many workers were unable to work. The Coronavirus Job Retention Scheme (the furlough scheme) was launched, under which the government paid a portion of employee wages for those not able to work during the pandemic. This was intended to retain the links between employers and workers, so that enterprise could restart more easily. The fiscal impact was felt on both the expenditure and revenue sides. Tax revenues fell as the economy went into recession.

The net effect of these measures was that public sector net debt rose substantially. The unemployment rate rose, but this was cushioned by the introduction of the furlough scheme.

Monetary measures:

The fiscal measures were supported by monetary instruments, with Bank Rate being cut to an unprecedentedly low level. Quantitative easing was also implemented (by March 2022 this stood at £895 billion) to try to maintain the flow of credit in the economy.

The UK economy after COVID:

2022 was a momentous year. The UK was emerging from the pandemic and the country's economy was expected to begin a recovery process. Aggregate demand was expected to increase, and aggregate supply would also increase as firms returned to production.

In February, Russia invaded Ukraine. This had major impacts on the economic situation:

- Energy markets were disrupted

- Exports of grain from Ukraine were interrupted

- The UK imposed sanctions on Russia and provided financial support to Ukraine

Some negative effects of Brexit were beginning to show, adding to supply-side disruptions. In July, Boris Johnson resigned as prime minister, and there followed a period in which economic policy took a back seat to political pressures within the Conservative Party. This culminated in the election of Liz Truss as PM.

She pursued a traditional Conservative policy stance of cutting taxes, in spite of a sluggish economy and concerns about a sudden rise in inflation caused primarily by cost-push pressures. Her mini-budget caused turmoil in financial markets, and she was soon replaced as PM by Rishi Sunak. In November, a new approach to policy was announced, with increases in some taxes and cuts in government spending.

At this time, the economy was recovering slowly from the pandemic. Real GDP had barely reached its pre-pandemic level. The Ukraine war was continuing and trade was still adjusting to Brexit. Inflation was above 10%. The Bank of England had raised Bank Rate to 3.5% (but were expecting inflation to fall in mid-2023). The economy was being disrupted by strikes. Prospects for restarting economic growth remained uncertain.

Supply-side policies

Demand-side policies have been aimed primarily at stabilising the macroeconomy in the relatively short run, but with the hope of affecting aggregate supply in the long run by influencing firms' and households' confidence in the future path of the economy.

However, there are also policies that can be used to influence the aggregate supply curve directly. These supply-side policies can take two forms:

-

Market-based policies: The classical economists recommend these policies, based on freeing up markets, providing improved incentives for enterprise and initiative.

-

Interventionist policies: Others advocate these policies, by which the authorities intervene directly in ways that stimulate aggregate supply.

The position of the long-run aggregate supply curve depends primarily on:

- The quantity of factor inputs available in the economy

- The effectiveness with which these resources are utilised

Supply-side policies aim to affect these fundamental determinants of productive capacity.

Remember!

Key Points to Remember: Fiscal and Monetary Policy

Fiscal Policy:

- Fiscal policy involves government decisions about spending, taxation, and borrowing to influence aggregate demand in the economy

- Works through the multiplier effect, which amplifies the initial impact on aggregate demand

- Only effective in increasing real output if the economy is below full employment

- The government budget deficit/surplus is the key measure of fiscal policy stance

Monetary Policy:

- Monetary policy uses interest rates and money supply to affect aggregate demand

- In the UK, the Bank of England's MPC sets Bank Rate to achieve a 2% inflation target

- The transmission mechanism describes the complex chain of linkages through which changes in Bank Rate affect inflation via market rates, asset prices, exchange rates, and ultimately aggregate demand

- Quantitative easing is an unconventional monetary policy tool used when interest rates are already very low – the Bank of England purchases assets to increase liquidity and encourage lending

Policy Effectiveness:

- Both fiscal and monetary policies work through the demand side of the economy

- Their effectiveness depends on where the economy is positioned relative to full employment on the LRAS curve

- If the economy is at full employment, expansionary policies will cause inflation rather than growth

Historical Lessons:

- The financial crisis, Great Depression, and COVID-19 pandemic show that combining fiscal and monetary policies can help stabilise the economy during severe shocks

- However, long-run growth ultimately depends on supply-side policies that increase the economy's productive capacity

- The Great Depression demonstrated the dangers of contractionary fiscal policy during a recession

Supply-Side Policies:

- These directly affect the productive capacity of the economy by shifting LRAS

- Can be market-based (freeing up markets) or interventionist (direct government intervention)

- Essential for achieving sustainable long-term economic growth