Preparing a Budget (Junior Cert Business Studies): Revision Notes

Preparing a Budget

A household budget is an essential financial planning tool that helps families manage their money effectively. When you create a comprehensive budget, you get a complete picture of your family's financial situation over a specific period.

What is a household budget?

A household budget shows all the money coming into your home (income) and all the money going out (expenditure) during a particular time period. This allows families to plan ahead and make informed decisions about their spending.

The budget includes:

- All sources of expected income (both regular and irregular)

- All planned expenditure, organised into three main categories

- Calculations showing how much money will be left over each month

Types of expenditure in budgets

Understanding the different types of expenditure is crucial for effective budgeting. All household spending falls into three categories:

Fixed expenditure refers to expenses that stay the same each month and must be paid regularly. Examples include mortgage payments, insurance premiums, and loan repayments.

Irregular expenditure covers essential expenses that vary in amount from month to month. Examples include grocery bills, utility bills, and transport costs.

Discretionary expenditure includes non-essential spending that you choose to make. Examples include entertainment, holidays, and luxury purchases.

The key difference is that fixed and irregular expenditures are necessary expenses, whilst discretionary spending is optional and can be reduced if needed.

Step-by-step guide to preparing a budget

Follow these steps to create an effective household budget:

Step 1: Record all expected income List every source of money coming into your household, including:

- Salaries and wages from employment

- Social welfare payments (such as Child Benefit)

- Any irregular income sources

Step 2: Plan your expenditure List all your planned spending and sort it into the three categories:

- Fixed expenditure first (these are your priorities)

- Irregular expenditure second (essential but variable costs)

- Discretionary expenditure last (only plan this after covering essentials)

Step 3: Calculate total expenditure Add together the subtotals from all three expenditure categories.

Total expenditure = Fixed expenditure + Irregular expenditure + Discretionary expenditure

Step 4: Work out net cash Subtract your total planned expenditure from your total expected income. This shows whether you'll have money left over or if you're spending more than you earn.

Step 5: Include opening cash Record how much money you have at the start of the budget period in both the first month and total columns.

Step 6: Calculate closing cash Add your opening cash to your net cash to find your closing cash. This becomes the opening cash for the following month.

Understanding your budget calculations

The mathematical calculations in budgeting are straightforward but essential for accurate financial planning. Here's how to apply the formulas in practise:

Worked Example: Monthly Budget Calculation

If a family has monthly expenditure of:

- Fixed costs: €1,200 (mortgage, insurance)

- Irregular costs: €800 (groceries, bills)

- Discretionary costs: €300 (entertainment, eating out)

Step 1: Calculate total expenditure

Step 2: Calculate net cash If their monthly income is €2,800:

Result: This means they have €500 left over each month, which could go into savings or emergency funds.

Why budgeting matters

Creating a budget helps you:

- See exactly where your money goes each month

- Identify areas where you might be overspending

- Plan for large expenses like holidays or home improvements

- Build up emergency savings for unexpected costs

- Make sure you can afford your essential expenses

A well-prepared budget gives you control over your finances and helps you make informed decisions about spending and saving.

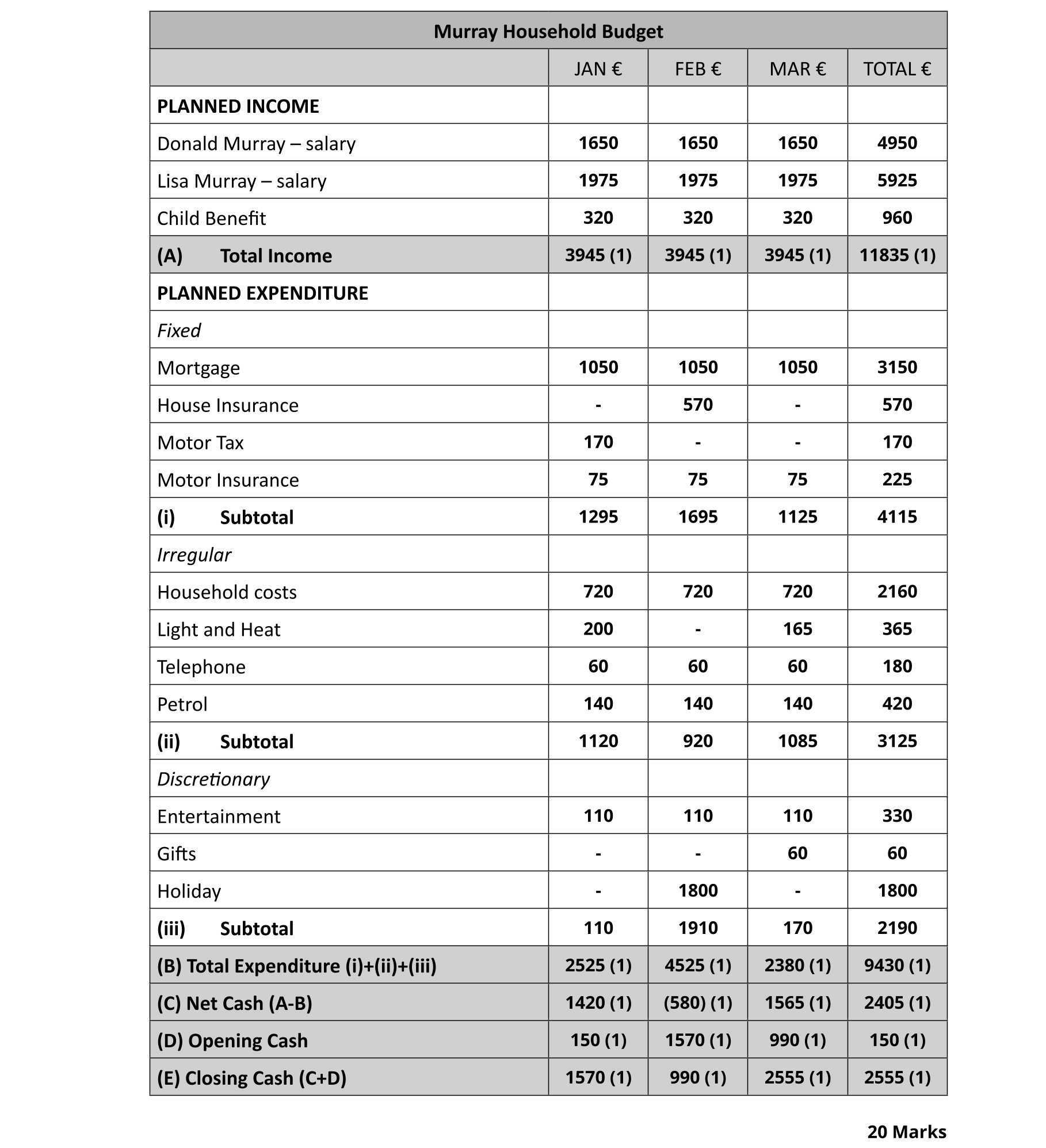

Example

Step 1: Record all expected income

Step 1: Record all expected income

The Murray family's income comes from:

- Donald Murray's salary: €1650 each month

- Lisa Murray's salary: €1975 each month

- Child Benefit: €320 each month

Total monthly income = €3945 Total income for 3 months = €11,835

Step 2: Plan your expenditure

Expenditure is divided into fixed, irregular, and discretionary spending:

- Fixed expenditure (essential, regular payments): Mortgage, House Insurance, Motor Tax, Motor Insurance

- Irregular expenditure (essential but changing amounts): Household costs, Light & Heat, Telephone, Petrol

- Discretionary expenditure (non-essentials, optional): Entertainment, Gifts, Holida

Step 3: Calculate total expenditure

- January: €2525

- February: €4525 (high due to house insurance and holiday)

- March: €2380

- Total expenditure for 3 months = €943

Step 4: Work out net cash

Net cash = Income – Expenditure

- January: €1420 surplus

- February: €580 deficit

- March: €1565 surplus

Overall, the family has €2405 left over at the end of the three months.

Step 5: Include opening cash

The family started January with €150 opening cash.

Step 6: Calculate closing cash

Closing cash = Opening Cash + Net Cash

- January: €1570

- February: €990

- March: €2555

The closing cash in March (€2555) becomes the opening cash for the next budget period.

Understanding this budget

- February highlights the importance of planning ahead: big costs (insurance, holiday) mean a cash deficit that month.

- By March, the family's savings build up again because expenditure is lower.

- This example shows how a household can use budgeting to spot when spending is high, avoid overspending, and plan for savings.

Remember!

Key Points to Remember:

- A household budget shows all income and expenditure over a specific period

- Expenditure must be categorised into fixed, irregular, and discretionary types

- Always plan fixed and irregular expenses before discretionary spending

- Total expenditure equals the sum of all three expenditure subtotals

- Net cash shows whether you're living within your means or overspending