What is the Economy? (Leaving Cert Business): Revision Notes

What is the Economy?

The economy refers to the way businesses, consumers, and the government produce, distribute, and consume goods and services in a country. It includes all activities that involve the exchange of money for goods or services.

- Ireland has a small, open economy, which means it relies heavily on international trade and is affected by global market changes.

- Being a member of the European Union (EU) and the eurozone strengthens Ireland's economy by providing access to larger markets and eliminating currency exchange costs.

Eurozone: The group of 20 EU countries that use the euro as their currency.

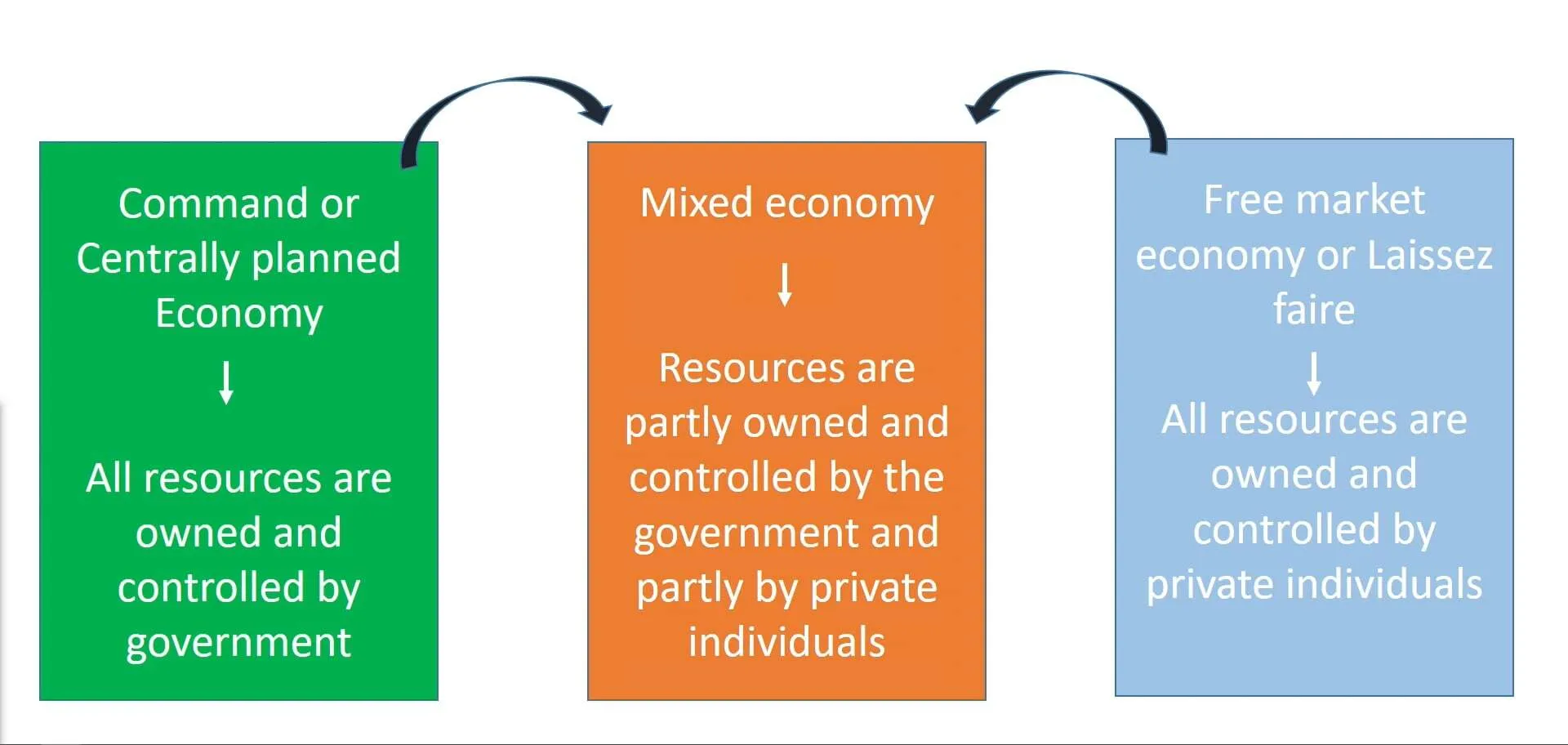

Economic Systems

An economic system is the way a country organises its factors of production (land, labour, capital, and enterprise) and how it decides:

- what goods and services to produce,

- how to produce them, and

- who gets them.

There are three main types of economic systems:

- Centrally Planned Economy

- The government controls all major decisions about production and distribution.

- Example: North Korea, Cuba.

- Free Market Economy

- Private businesses make most decisions based on supply and demand, with little government involvement.

- Example: The USA is the closest to a true free market economy.

- Mixed Economy

- Combines both government planning and private enterprise.

- Example: Ireland, most EU countries, China.

- In Ireland, hospitals, schools, and transport are partly run by the state, while most goods and services are provided by private businesses.

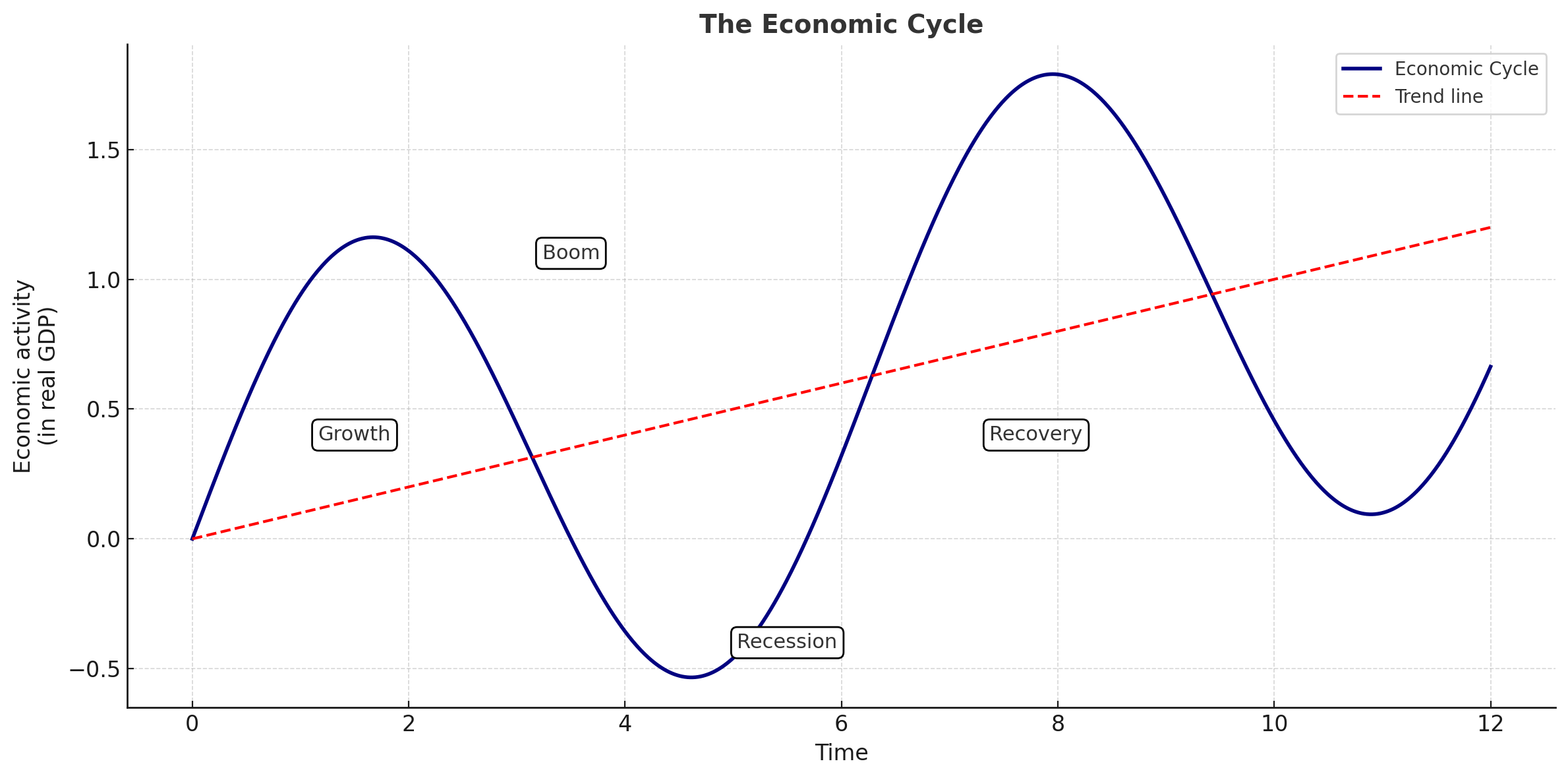

The Economic Cycle

Economic activity doesn't stay the same all the time. Instead, it moves in a repeating pattern called the economic cycle, which includes the stages of:

- Boom

- Peak

- Recession

- Recovery

Gross Domestic Product (GDP) is used to measure economic performance. It calculates the total value of goods and services produced within a country.

Stages of the Economic Cycle:

- Economic Boom:

A time of rapid economic growth, with high employment, strong consumer demand, rising wages and profits.

- Example: Ireland during the Celtic Tiger years (1995–2008).

- Economic Peak: The highest point of economic activity, just before the economy starts to slow down.

- Economic Recession:

A decline in economic activity lasting at least six months. It involves rising unemployment, lower spending, and reduced investment.

- Example: Ireland's recession after the 2008 financial crash.

- Economic Recovery: The period after a recession when the economy begins to grow again. Employment, spending, and production rise, and confidence returns.

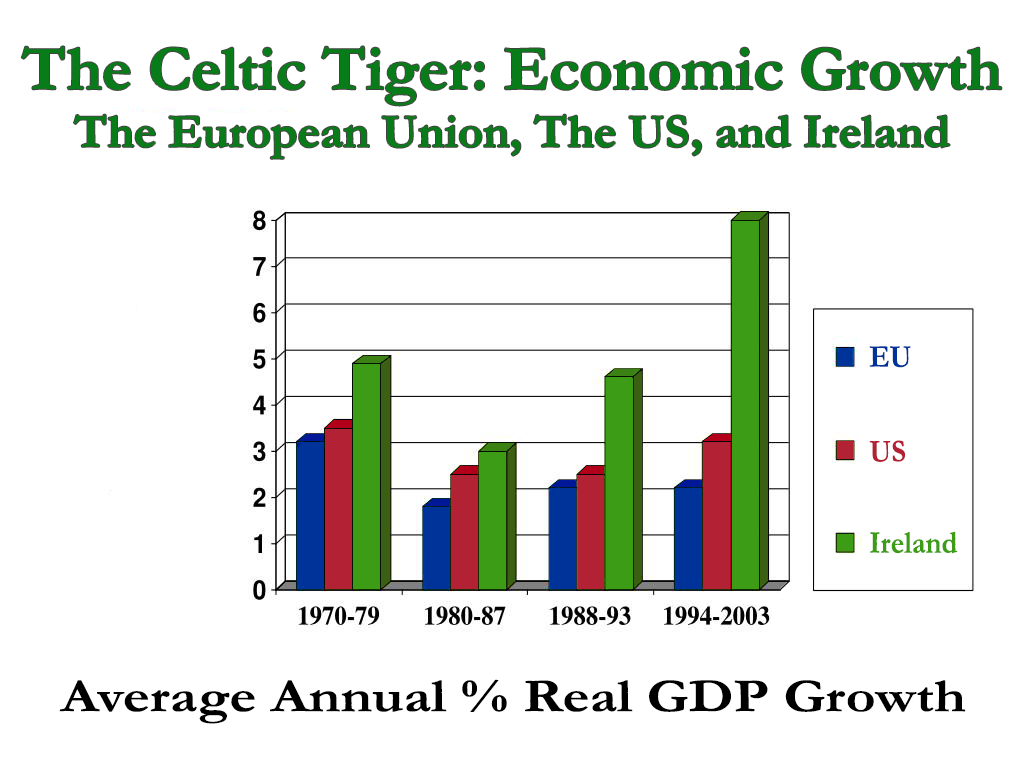

Ireland: The Celtic Tiger

Ireland's economy grew strongly during the Celtic Tiger period (1995–2008):

- Low unemployment

- High investment in housing and infrastructure

- Fast GDP growth

This was followed by a deep recession (2008–2015) due to the global financial crisis:

- Major job losses

- Collapse of the banking sector

- Government borrowing from the "Troika" (EU, ECB, IMF)

Ireland did not enter a full depression, but the effects were long-lasting. Unemployment, national debt, and consumer uncertainty remained high for years.

Recent Developments in the Irish Economy

- Ireland is showing signs of another economic boom, but challenges remain.

- National debt is over €200 billion.

- Concerns about Brexit, global instability, and inflation mean the economy is still vulnerable.

- Exports, EU membership, and the presence of large TNCs (e.g. Apple, Google, Pfizer) are key to continued growth.