Break-Even Analysis (Grade 11 NSC Matric Mathematical Literacy): Revision Notes

Break-Even Analysis

What is break-even?

Break-even point represents the exact moment when a business covers all its expenses without making a profit or loss. At this critical point, the total income from sales equals the total costs of running the business.

Understanding break-even is essential for any business because it provides crucial financial insights that determine business viability and planning strategies.

Understanding break-even is essential for any business because it shows:

- How many products must be sold to cover all costs

- The minimum income needed to avoid making a loss

- When the business will start generating profit

Beyond business contexts, break-even can also refer to situations where two options become equally valuable, such as comparing different cell phone contracts or electricity usage systems.

Break-even has two values

Break-even analysis always produces two related values that work together to show the complete break-even picture.

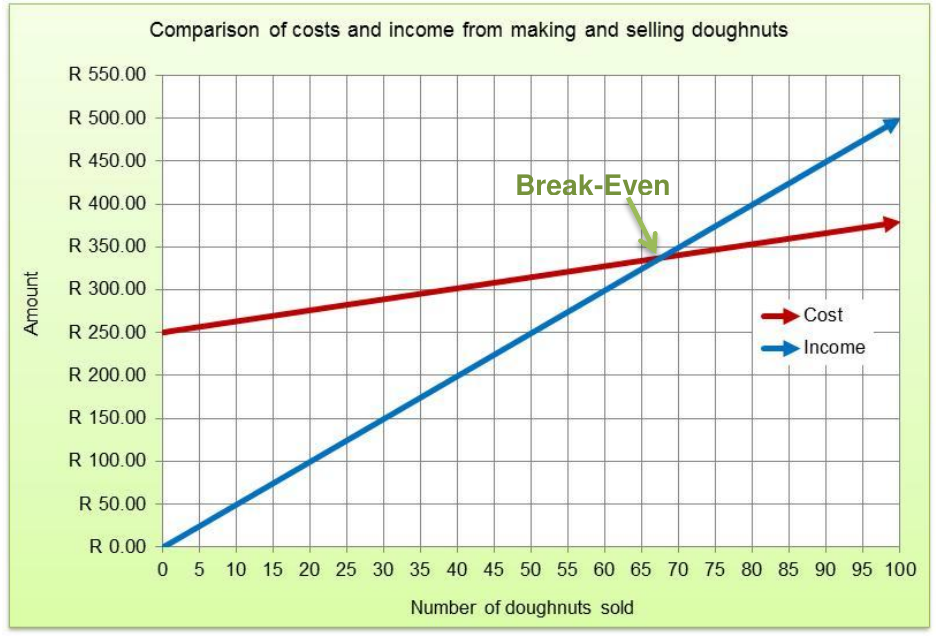

Looking at this doughnut business example, we can see how break-even works in practice:

The two break-even values are:

- Horizontal axis value: Number of doughnuts (approximately 67 doughnuts)

- Vertical axis value: Amount in Rand (approximately R340)

This means the business breaks even when:

- 67 doughnuts are sold, AND

- Both income and costs equal R340

Key insight: These two values always work as a pair. You cannot have a break-even point with just one value - you need both the quantity and the monetary amount.

Methods for determining break-even values

There are two main methods for finding break-even values:

Method 1: Graphical method

This involves:

- Drawing a graph with costs and income lines

- Finding where the two lines intersect

- Reading both values from the intersection point

The graph clearly shows the break-even point where the red cost line meets the blue income line.

Method 2: Trial and improvement

This mathematical approach uses equations and intelligent guessing with the following given information for the doughnut business:

- Income per doughnut = R5.00

- Fixed cost (stall rental) = R250.00

- Variable cost per doughnut = R1.30

Formulas:

- Income = R5.00 × number of doughnuts

- Total cost = R250.00 + (R1.30 × number of doughnuts)

Worked examples using trial and improvement

Worked Example 1: Testing 100 doughnuts

- Income = R5.00 × 100 = R500.00

- Cost = R250.00 + (R1.30 × 100) = R250.00 + R130.00 = R380.00

- Result: Income > Cost (profit situation)

Worked Example 2: Testing 50 doughnuts

- Income = R5.00 × 50 = R250.00

- Cost = R250.00 + (R1.30 × 50) = R250.00 + R65.00 = R315.00

- Result: Income < Cost (loss situation)

Worked Example 3: Refining the estimate

Since 50 doughnuts gives a loss and 100 doughnuts gives a profit, the break-even point lies between these values. Through continued testing, we find that approximately 68 doughnuts will give us the break-even point.

Verification:

- Income = R5.00 × 68 = R340.00

- Cost = R250.00 + (R1.30 × 68) = R250.00 + R88.40 = R338.40

- These values are approximately equal, confirming our break-even point.

Key formulas to remember

For any break-even analysis:

Exam tips

Critical exam strategies:

- Always express break-even as two values (quantity and amount)

- Show all working when using trial and improvement

- Read graph coordinates carefully for both axes

- Check your answer makes sense in the business context

- Remember that break-even means no profit and no loss

Summary

Key Points to Remember:

-

Break-even point occurs when total income equals total costs - the business makes neither profit nor loss

-

Break-even always has two values - one from the horizontal axis (quantity) and one from the vertical axis (monetary amount)

-

Two methods exist: graphical intersection method and trial and improvement using equations

-

Trial and improvement requires testing different quantities until income and costs are approximately equal

-

Break-even analysis helps businesses determine minimum sales targets needed to avoid losses