Future Value Annuities (Grade 12 NSC Matric Mathematics): Revision Notes

Future Value Annuities

What is an annuity?

An annuity is a series of equal payments made at regular intervals for a specific period of time. These payments are subject to a rate of interest, which means your money grows over time through compound interest.

There are two main types of annuities you need to understand:

-

Future value annuity - You make regular deposits into a savings account or investment fund to accumulate money for future use. The money earns compound interest at a certain rate.

-

Present value annuity - You make regular payments to pay back a loan or bond over a given time period. The reducing balance is usually charged compound interest at a certain rate.

For investment funds, pension funds, loan repayments, and mortgage bonds, payments are typically made monthly. When a payment is missed for a particular month, this is called "defaulting" on the payment.

Understanding future value annuities

Future value annuities work by regularly saving the same amount of money into an account that earns compound interest. This means you earn interest not only on your deposits but also on the interest already earned.

Key Principle: The earlier you deposit money, the more interest it will earn. Your first deposit earns interest for the longest time, while your last deposit earns the least interest.

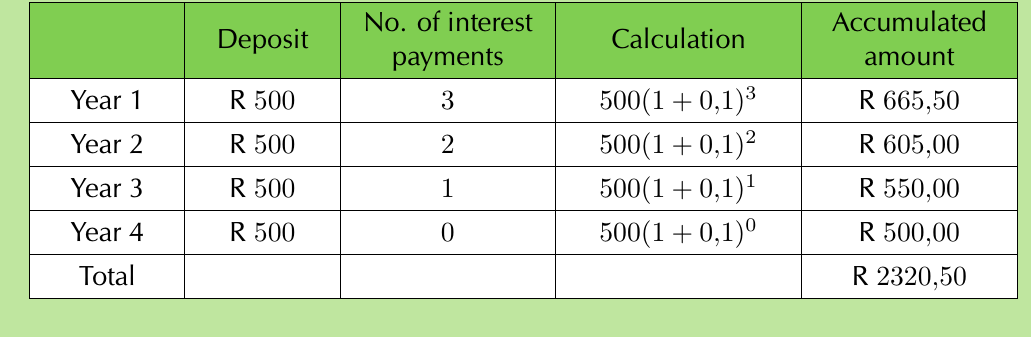

This table demonstrates how different deposits earn varying amounts of interest based on when they are made. Notice how the first deposit of R500 grows to R665.50 after earning interest for 3 periods, while the final deposit earns no interest.

The future value annuity formula

Formula derivation

The total value of a future value annuity can be calculated by recognising that the accumulated amounts form a geometric series.

For a geometric series where :

Where:

- = first term

- = common ratio

- = number of terms

In annuity problems:

- (the regular payment amount)

- (where is the interest rate)

- = number of payments

Main formulas

Future value of annuity:

Payment amount needed:

Where:

- = future value (total amount accumulated)

- = regular payment amount

- = interest rate per period

- = total number of payments

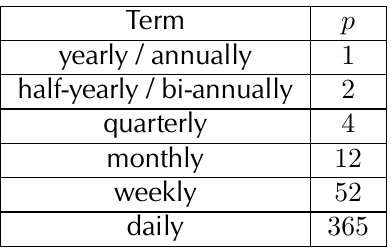

Payment frequency conversions

When payments are made more frequently than annually, you need to adjust the number of payments and interest rate accordingly.

Critical Conversion Rule: If you have a nominal interest rate , convert it to an effective interest rate using:

Worked example 1: Basic future value calculation

Worked Example: Basic Future Value Calculation

Question: Kobus deposits R500 at the end of each year for 4 years into an investment account with 10% interest per annum compounded yearly. Find the value of his investment after 4 years.

Solution:

Step 1: Write down the given information and formula

Step 2: Draw a timeline to visualise the problem

The timeline shows deposits of R500 at T₁, T₂, T₃, and T₄, with 10% compound interest.

Step 3: Apply the formula

Answer: Kobus will have R2320.50 in his account after 4 years.

Worked example 2: Monthly payments calculation

Worked Example: Monthly Payments Calculation

Question: Ciza deposits R900 at the end of each month for 29 years into an account earning 8.25% interest per annum compounded monthly. Determine her account balance after 29 years.

Solution:

Step 1: Identify the given information

- (monthly interest rate)

- (total monthly payments)

Step 2: Calculate using the formula

Answer: Ciza will have R1,289,665.06 after 29 years.

Worked example 3: Finding required payment amount

Worked Example: Finding Required Payment Amount

Question: Kosma wants to save R25,000 for a trip to Canada in 2 years. Her savings account earns 10.7% per annum compounded monthly. How much must she save each month?

Solution:

Step 1: Use the payment formula

Where:

Step 2: Calculate the monthly payment

Answer: Kosma must save R938.80 each month.

Sinking funds

A sinking fund is a special type of future value annuity used by businesses to save money for replacing equipment, vehicles, or other assets that depreciate over time.

Companies set aside regular amounts so they will have enough money accumulated when old equipment needs to be replaced. The fund earns compound interest, helping reach the target amount needed.

Worked example 4: Sinking fund calculation

Worked Example: Sinking Fund Calculation

Question: Wellington Courier Company buys a truck for R296,000. The truck depreciates at 18% per annum. The company expects new truck prices to increase by 9% annually. They want to replace the truck in 7 years and need to determine monthly sinking fund deposits if the fund earns 13% per annum compounded monthly.

Solution:

Step 1: Calculate the truck's book value after 7 years

Step 2: Calculate the expected cost of a new truck in 7 years

Step 3: Determine the sinking fund target

Step 4: Calculate required monthly deposits

-

-

Where , ,

-

Answer: The company must deposit R3,438.77 each month into the sinking fund.

Problem-solving tips:

-

Always draw a timeline - This helps visualise when deposits are made and when interest is earned.

-

Check your payment frequency - Make sure your interest rate and number of periods match the payment frequency.

-

Don't round intermediate steps - Only round your final answer to avoid accumulating errors.

-

Use the correct formula - Future value formula when finding total amount; payment formula when finding deposit amount.

Key Points to Remember:

- Future value annuities help you save money for future goals through regular deposits that earn compound interest

- The earlier you start saving, the more your money grows due to compound interest

- Use to find the future value of regular payments

- Convert payment frequencies correctly - monthly payments mean dividing annual rate by 12 and multiplying years by 12

- Sinking funds are practical applications where businesses save for future equipment replacement