Fixed Exchange Rate Systems (HSC SSCE Economics): Revision Notes

Fixed Exchange Rate Systems

Introduction

Australia currently operates a floating exchange rate system, where the value of the Australian dollar is determined by market forces. However, this has not always been the case. Before December 1983, Australia used various forms of fixed exchange rate systems to manage the value of its currency.

Understanding fixed exchange rate systems is important because:

- They provide historical context for Australia's current system

- Some major economies (like China) still use variations of fixed systems

- The principles help explain how governments can intervene in foreign exchange markets

Australia's exchange rate history

Australia's exchange rate arrangements have evolved through three distinct phases:

Before November 1976: Fixed exchange rate system

- The Australian dollar was pegged to other currencies at different times

- Currencies used as anchors included the UK pound sterling, the US dollar, and the Trade Weighted Index

November 1976 to December 1983: Managed flexible peg

- A variation of the fixed exchange rate system

- Provided more day-to-day flexibility than a purely fixed system

December 1983 onwards: Floating exchange rate

- The current system where market forces determine the currency's value

How fixed exchange rates work

Under a fixed exchange rate system, the government or central bank officially determines the exchange rate. This means the currency's value is not left to the forces of supply and demand in the foreign exchange market.

The mechanics of intervention

When a government sets an exchange rate, it must be willing and able to maintain that rate through market intervention. This involves:

Buying and selling currency: The central bank buys or sells its own currency in exchange for foreign currency to keep the exchange rate at the official level.

Using foreign reserves: To support the currency's value, the central bank must hold reserves of foreign currencies and/or gold. These reserves are used when the bank needs to purchase domestic currency from the market.

Understanding the process with a diagram

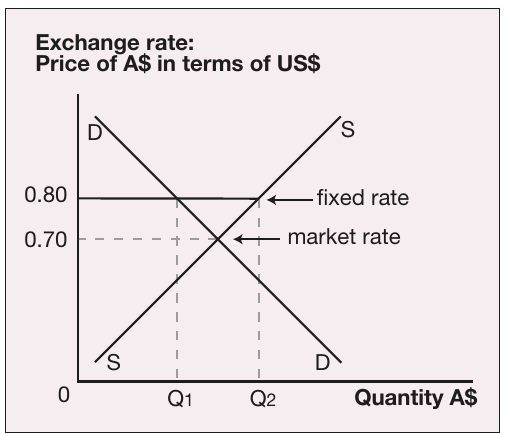

Consider a situation where the Australian government sets the exchange rate at A$1 = US$0.80, but market forces would naturally push the rate to A$1 = US$0.70. This scenario is illustrated below:

Worked Example: Maintaining a Fixed Exchange Rate

In this diagram:

- The official fixed rate is set at US$0.80 per Australian dollar

- The natural market rate would be US$0.70

- At the official rate, there is excess supply of Australian dollars (shown by the distance between Q₁ and Q₂)

- To maintain the fixed rate, the RBA must buy this excess supply of A$ using its foreign currency reserves

The challenge of maintaining fixed rates

The government faces a significant challenge: it must continuously purchase the excess supply of Australian dollars at the official price. This requires holding substantial foreign reserves.

The role of foreign reserves: When Australia operated a fixed exchange rate system, the Reserve Bank of Australia obtained foreign reserves by requiring all foreign exchange holdings to be lodged with the central bank. However, even with this mechanism, there was a serious risk.

Risk of reserve depletion: If the RBA had to repeatedly intervene to support an overvalued Australian dollar, it could exhaust its foreign reserves. This could ultimately lead to a complete collapse of confidence in the currency and breakdown of the fixed rate system.

Official adjustments: devaluation and revaluation

When market pressures became too strong, the government could adjust the official exchange rate:

Devaluation: The government officially lowers the exchange rate. This makes the domestic currency worth less in terms of foreign currencies.

Revaluation: The government officially increases the exchange rate. This makes the domestic currency worth more in terms of foreign currencies.

While these adjustments could bring the official rate closer to market reality, they often reflected a failure of the fixed rate system and could damage confidence in the currency.

Limitations of fixed exchange rates

Fixed exchange rate systems come with several important constraints:

Restricted monetary policy: Fixed rates limit the central bank's ability to use interest rates for domestic economic management. Interest rate changes affect the exchange rate, which conflicts with maintaining a fixed rate target.

Foreign reserve requirements: The system requires substantial holdings of foreign currency reserves, which represent an economic cost and may prove insufficient during periods of intense market pressure.

Potential misalignment: The official rate can drift away from the rate that would naturally emerge from market forces, leading to economic distortions.

The managed flexible peg

The managed flexible peg represents a middle ground between fully fixed and fully floating exchange rates. Australia used this system from November 1976 to December 1983.

How the system operated

Under the managed flexible peg:

Daily pegging: The Reserve Bank would set or "peg" the value of the Australian dollar at 9:00 am each day. This pegged rate would then operate throughout the entire trading day.

Limited flexibility: Each day brought the potential for a new peg level, providing more flexibility than a permanently fixed rate. However, the rate remained constant during each trading day.

Gradual adjustment: The system allowed for more frequent but smaller adjustments compared to a fully fixed system, where changes required formal devaluation or revaluation.

Advantages and disadvantages

Greater flexibility: The managed flexible peg offered more adaptability than a purely fixed exchange rate, as the daily peg could be adjusted regularly to reflect changing economic conditions.

Drift from market forces: Despite this flexibility, the official rate could still diverge from what market forces would produce. Many economists argued that Australia maintained an overvalued exchange rate under this system during the early 1980s, demonstrating that the managed peg still suffered from similar problems to fully fixed rates.

Transition system: The managed flexible peg served as a transitional arrangement between Australia's fixed exchange rate past and its floating exchange rate future, allowing gradual adjustment to market-determined currency values.

Government participation in global foreign exchange markets

While most developed economies now use floating exchange rates, some governments continue to play an active role in determining their currency's value. The most prominent example is China.

The diminishing role of central banks

In recent decades, private sector participants have become increasingly dominant in global foreign exchange markets. Currency speculators managing very large funds have reduced the power of governments to influence exchange rates.

For most currencies like the Australian dollar, Japanese yen, and British pound, central banks now play mainly a residual role. They occasionally intervene to stabilise currency values but do not attempt to set or control the exchange rate.

China's exchange rate management

China provides the most significant example of ongoing government intervention in foreign exchange markets. The People's Bank of China (PBC) actively manages the value of the yuan (also called the renminbi).

Historical approach (1994-2005): The PBC maintained a strictly fixed exchange rate at 8.27 yuan per US dollar.

Crawling peg system (2005-present): After 2005, China adopted a more flexible approach while still maintaining significant control:

- The central bank sets a daily reference rate

- The yuan is allowed to move within a trading band of 2% in either direction from this reference rate

- The PBC intervenes if the currency moves beyond these limits

- By mid-2023, the yuan was valued at approximately 7.0 per US dollar

Maintaining the crawling peg

To keep the exchange rate within its target band, Chinese authorities must:

Be willing to buy US dollars: The PBC must stand ready to purchase US dollars for 7.0 yuan.

Be willing to sell US dollars: The PBC must also be prepared to sell US dollars for 7.0 yuan.

Accumulate reserves: When there is strong demand for yuan at the target rate, the Chinese central bank sells yuan and accumulates US dollar reserves. This has led to a massive accumulation of foreign exchange reserves.

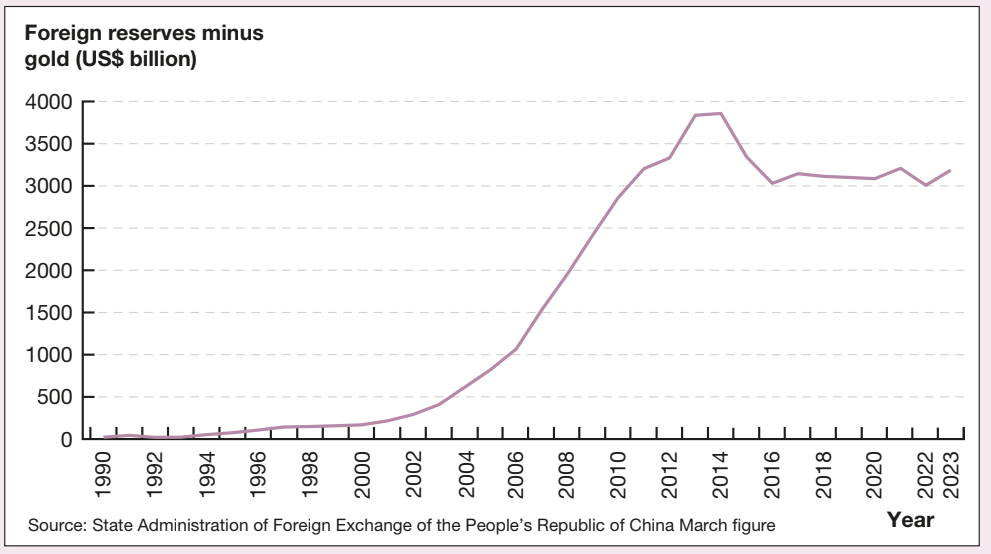

China's foreign exchange reserves

The scale of China's intervention in foreign exchange markets is reflected in its enormous foreign reserve holdings:

The graph shows that China's foreign reserves (excluding gold) grew from around US$150 billion in the early 2000s to over US$3.2 trillion at their peak. This represents a more than twenty-fold increase and makes China the world's largest holder of foreign exchange reserves.

Peak and decline: Reserves peaked around 2014 at approximately US$3.8 trillion. Since then, they have fallen moderately and stabilised around US$3-3.2 trillion, reflecting China's gradual move toward greater exchange rate flexibility.

Impact of intervention: It was estimated that in late 2022, the Chinese yuan was approximately 10% lower than it would have been without government intervention. This demonstrates the significant ongoing role of the Chinese government in the foreign exchange market.

Moving toward internationalisation

China is gradually reducing its intervention and allowing more market influence over the yuan's value. This process, known as internationalisation of the renminbi, can be seen in:

- The moderate decline in foreign reserves since 2014

- Widening of the daily trading band over time

- Greater flexibility in day-to-day currency movements

As China continues this transition, it contributes to the broader global trend of diminishing central bank involvement in foreign exchange markets.

Remember!

Key Points to Remember:

- Fixed exchange rate systems involve government or central bank setting the currency value rather than allowing market forces to determine it

- To maintain a fixed rate, the central bank must intervene by buying or selling currency, which requires holding substantial foreign reserves of foreign currency and gold

- When market pressure becomes too strong, governments may need to devalue (lower) or revalue (raise) the official exchange rate

- The managed flexible peg was a variation used in Australia (1976-1983) where the RBA set a new peg each morning, providing more flexibility than a purely fixed system

- China remains the most prominent example of active government exchange rate management, accumulating over US$3 trillion in foreign reserves to maintain its crawling peg system