Consumer Sovereignty and Decisions to Spend or Save (HSC SSCE Economics): Revision Notes

Consumer Sovereignty and Decisions to Spend or Save

What is consumer sovereignty?

Consumer sovereignty is a fundamental principle in market economies. It describes how consumers determine what gets produced by exercising their freedom to choose what they buy. When consumers purchase certain goods and services, they send demand signals to producers. Businesses respond by producing whatever is in demand.

This concept answers two key economic questions: what should be produced, and how much should be produced. The answers come directly from consumer choices. This is a major strength of market economies because production aligns with what people actually want.

How consumer sovereignty works

Consumer sovereignty operates through a simple mechanism:

The Consumer Sovereignty Cycle:

- Consumers demand certain goods and services

- When demand is high relative to supply, prices rise

- Higher prices signal greater profit opportunities to producers

- Producers shift resources into producing high-demand items

- Resources are allocated according to consumer preferences

This process determines resource allocation across the entire economy.

Consumer income levels also shape production patterns. As an economy becomes more prosperous and incomes rise, demand for luxury goods increases. During economic upturns, production of items like sports cars and designer clothing expands. Conversely, during downturns, production of these items contracts.

Limitations of consumer sovereignty

However, consumer sovereignty is not absolute. In modern market economies, several business practices can reduce consumers' true sovereignty:

Marketing influence: Advertising and direct marketing powerfully influence consumer spending patterns. While some marketing is informative, most strategies focus on understanding target consumers to manipulate their behaviour. Marketers conduct extensive research into consumer wants, interests, desires and fears, using this to drive both mass marketing (television, radio, social media) and targeted advertising (Facebook, Instagram, Google search). Manipulative or deceptive marketing diminishes consumer sovereignty.

Common Threats to Consumer Sovereignty:

-

Misleading or deceptive conduct: False or dishonest claims about products deceive consumers into paying for items they don't genuinely want. This is particularly common in claims about fresh food, weight-loss products, anti-aging treatments, investment schemes, and various health products.

-

Planned obsolescence: Some firms deliberately design goods to wear out quickly or become outdated, encouraging consumers to make repeat purchases. By emphasising the importance of having the latest products, firms manipulate people into buying more frequently than necessary. For example, motor vehicle manufacturers regularly change designs to make older models appear outdated, even when they function perfectly well.

-

Anti-competitive behaviour: Firms operating in markets with few competitors can limit consumer choice. For instance, businesses may manufacture electronic devices compatible only with their own brand of accessories (power cords, batteries), even when cheaper generic alternatives would work equally well.

The sovereignty debate

Economists debate whether these factors create a degree of business sovereignty instead of consumer sovereignty. Some critics argue that much consumer demand is generated by deceptive marketing that exploits people's fears and insecurities. Others contend these practices are natural features of market economies, and consumers still ultimately control their own purchasing decisions.

Decisions to spend or save

The fundamental relationship

After receiving income and paying tax, consumers face a basic choice: spend the remaining money (consumption) or save it. This relationship is expressed as:

Where:

- = Disposable (after-tax) income

- = Consumption expenditure

- = Savings

This equation tells us that for any given income level, an increase in consumption equals a decrease in saving, and vice versa. Any change in income level affects both consumption and savings.

Average propensities to consume and save

The proportion of income spent on consumption is the average propensity to consume (APC). The proportion saved is the average propensity to save (APS).

Since every dollar of disposable income must be either spent or saved:

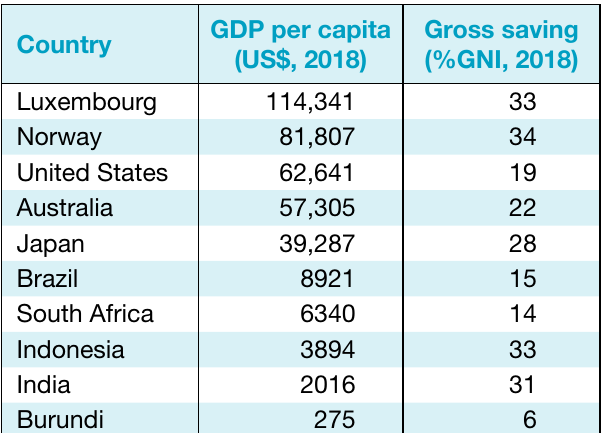

The table below shows savings levels for various high-, middle- and low-income economies. While higher per-capita income countries tend to save more, the relationship between income and savings at the economy-wide level is not straightforward.

Factors influencing spending and saving decisions

Multiple factors influence whether individuals choose to spend or save:

Cultural factors: Savings patterns vary across cultures. For example, people in some East Asian economies save more than those in other industrialised countries. Previous generations also tended to save more than people today.

Personality factors: Some individuals are naturally cautious and prefer having savings for future needs. Others are more relaxed and prefer enjoying immediate benefits.

Confidence and future expectations: When consumers worry about economic outlook, they save more. When confident about the future and expecting income growth, they consume more and save less. Interestingly, confidence changes may not always reflect actual economic conditions. Research from the Reserve Bank of Australia found that after elections, consumers who voted for the winning party felt more optimistic and increased consumption compared to those who voted for the losing party.

Future spending plans: Individuals save more when planning major expenses like holidays or car purchases.

Tax policies: Tax systems can make saving more attractive (such as lower taxes on superannuation savings) or spending more attractive (such as removing consumption taxes).

Credit availability: When credit is readily available, spending increases because it provides an additional money source. People also save less if confident they can access credit easily in the future.

While all these factors matter, the two most significant influences on spending and saving decisions are income and age.

Income as a key determinant

The income-consumption relationship

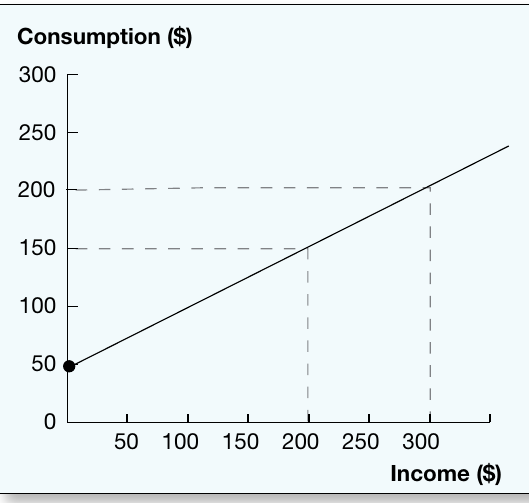

As income rises, people save a higher proportion of their income (APS rises and APC falls). Lower-income consumers must spend a larger proportion on essentials. For example, someone earning $300 per week might spend it all on basic living costs, while someone earning $3,000 per week could comfortably save 50%.

The consumption function diagram illustrates this relationship between income and consumption.

As income increases, consumption also increases. However, even at very low income levels, individuals maintain some positive consumption level (say $50 per week), financed through credit or existing savings.

Worked Example: Calculating Average Propensities

When income rises from $200 to $300, consumption rises from $150 to $200.

At income level $200:

- (or 75%)

- (or 25%)

At income level $300:

- (or 67%)

- (or 33%)

Notice that as income rises, APC falls and APS rises. Because income rises faster than consumption, people save a higher proportion of their income at higher income levels.

Marginal propensities

The marginal propensity to consume (MPC) measures the proportion of each extra dollar of income that goes to consumption. It represents the slope of the consumption function.

The marginal propensity to save (MPS) measures the proportion of each extra dollar saved.

Since each extra dollar must be either spent or saved:

Worked Example: Calculating Marginal Propensities

Using the previous example where income rises from $200 to $300:

Change in income: $300 - $200 = $100

Change in consumption: $200 - $150 = $50

Change in saving: $100 - $50 = $50

Therefore:

- (50% of extra income is consumed)

- (50% of extra income is saved)

Check: ✓

In the simple example above, both MPC and MPS remained constant (the consumption function was a straight line with gradient ). In reality, as income rises, MPC tends to fall and MPS tends to rise, making the consumption function less steep at higher income levels.

Application to the whole economy

These relationships apply economy-wide. As a country's national income rises, overall savings should increase at a faster rate. However, this doesn't always hold true. The United States, despite being one of the world's richest nations, had a relatively low savings rate of 19% of GNI in 2018.

Age as a key determinant

The life-cycle theory of consumption

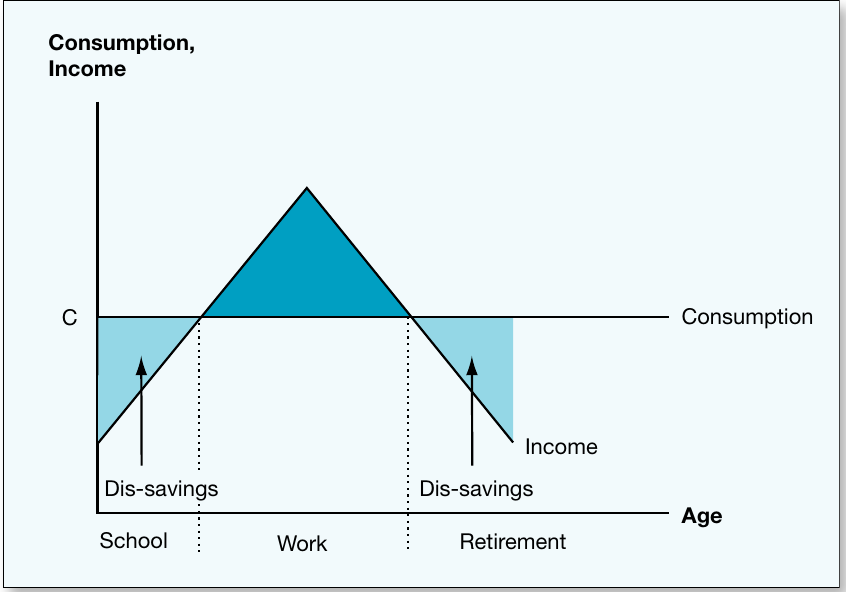

An individual's income and consumption patterns are not constant throughout life. People tend to smooth their consumption - maintaining a reasonably steady standard of living even when income fluctuates significantly across different periods.

Consumption and savings behaviour moves through several distinct patterns over a lifetime:

The Three Life Stages of Consumption:

Young people (education phase): Receive lower incomes due to lacking skills, experience and education. They spend most or all their income and often dis-save (borrow) to finance education and training.

Working-age people (middle age): Incomes rise with experience and career progression. They consume a smaller proportion of income, saving and accumulating assets for retirement.

Retired people: No longer earn income from labour. They consume from past savings and accumulated wealth, or rely on government pension benefits. This represents another dis-saving phase.

Why higher earners save more

This life-cycle approach explains why individuals on higher incomes have a lower average propensity to consume than lower-income earners. Higher-income individuals (typically middle-aged workers) save more to pay past debts and accumulate retirement assets. Lower-income earners must use a higher proportion of income on day-to-day necessities like food and housing.

As individuals age, their average propensity to consume initially falls (as income rises during working years) then subsequently rises again after retirement when they begin consuming their accumulated savings.

Key Points to Remember:

-

Consumer sovereignty means consumers determine what gets produced through their purchasing decisions, but it's limited by marketing, deceptive conduct, planned obsolescence and anti-competitive behaviour

-

The fundamental relationship is - disposable income equals consumption plus savings

-

Average propensities show the proportion of total income consumed (APC) or saved (APS), and they must sum to 1:

-

Marginal propensities show how each additional dollar is allocated between consumption (MPC) and saving (MPS), and they must also sum to 1:

-

As income rises, people tend to save a higher proportion (higher APS, lower APC)

-

The life-cycle theory explains how consumption and saving patterns change throughout life: dis-saving when young, saving during working years, and dis-saving again in retirement