Covid-19: The Impacts on the Australian Economy (HSC SSCE Economics): Revision Notes

Covid-19: The Impacts on the Australian Economy

Introduction: the COVID-19 shock

The COVID-19 pandemic delivered the most severe external shock to Australia's economy since the Great Depression of the 1930s. It brought an abrupt end to Australia's unprecedented 28-year run of continuous economic expansion in ways that seemed unimaginable before 2020.

The scale of this disruption cannot be overstated. Australia had enjoyed nearly three decades without a recession – a record among developed economies. The sudden halt to this expansion marked a dramatic turning point in the nation's economic history.

The pandemic triggered extraordinary restrictions on economic activity. State and national borders were closed, strict lockdowns confined people to their homes, and entire economic sectors were temporarily shut down. These measures created immediate and dramatic shifts in economic behaviour.

Consumer spending patterns changed drastically. Expenditure on travel, leisure and entertainment collapsed as these activities became impossible or restricted. Meanwhile, households stockpiled essential supplies from supermarkets and redirected spending toward home entertainment.

Financial markets responded with sharp volatility. Within just one month of the pandemic's onset, the share market had plunged 37%, whilst the Australian dollar depreciated to US$0.55 – its lowest value in nearly twenty years. However, both markets rebounded relatively quickly as policy responses took effect.

Policy responses to COVID-19

The Australian government and Reserve Bank mounted the largest macroeconomic policy intervention in the nation's history. The scale of support measures reflected the unprecedented nature of the crisis.

Fiscal policy interventions

The government's fiscal response totalled $291 billion in economic support by mid-2021. This massive intervention resulted in Australia's largest-ever budget deficit of $132 billion in 2020-21.

The cornerstone of the fiscal response was the JobKeeper payment scheme. This $89 billion programme provided wage subsidies to businesses whose revenue had fallen by at least 30% due to COVID-19. Initially, the subsidy was set at $1,500 per fortnight per employee. The payment rates were gradually reduced over time before the programme ended in March 2021.

The JobKeeper scheme was revolutionary in scale and design. At $89 billion, it represented the single largest government programme in Australian history, directly supporting millions of workers and helping to maintain the employment relationship between businesses and their staff during the crisis.

Additional fiscal measures included:

- Substantial increases to unemployment benefits, with fortnightly payments temporarily doubled

- Free childcare provision for several months

- Tax-free cash payments ranging from $20,000 to $100,000 for eligible small and medium businesses

- One-off COVID-19 business support grants

These measures aimed to maintain household incomes, support business survival, and preserve employment relationships during the crisis.

Monetary policy interventions

The Reserve Bank of Australia (RBA) complemented fiscal policy with aggressive monetary stimulus. The RBA implemented three cash rate cuts during 2020, reducing the rate to a historic low of 0.1% by November 2020.

This represented the lowest official interest rate in Australian history. Prior to COVID-19, the RBA had never reduced the cash rate below 0.75%, making the November 2020 rate of 0.1% a truly extraordinary policy setting.

Beyond conventional interest rate policy, the RBA undertook unconventional measures. It supported credit supply to ensure businesses could access finance during the crisis. The RBA also engaged in asset purchases – the direct buying of financial assets from the private sector – to inject liquidity into the economy and support financial market functioning.

Economic impacts of COVID-19

The COVID-19 recession created wide-ranging effects across different dimensions of the Australian economy.

Economic growth and GDP

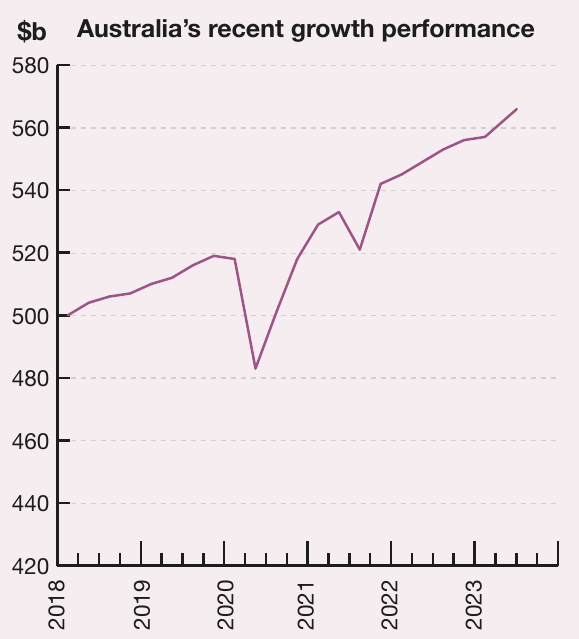

Australia experienced a technical recession in 2020, with GDP contracting in two consecutive quarters. The March quarter saw a decline of 0.2%, followed by a record 6.7% fall in the June quarter – the sharpest quarterly contraction in modern times.

The economy began recovering from September 2020. GDP increased by 3.8% in the September quarter, followed by 3.3% growth in December 2020. The recovery continued with growth of 3.9% recorded for 2021-22.

Despite the recovery, the Australian Bureau of Statistics estimated that the level of GDP suffered a cumulative loss of $158 billion compared to what would have occurred following its pre-pandemic growth trajectory. This represents the permanent output cost of the pandemic, even though growth rates returned to more normal patterns.

However, despite this recovery, the Australian Bureau of Statistics estimated that the level of GDP suffered a cumulative loss of $158 billion compared to what would have occurred following its pre-pandemic growth trajectory. This represents the permanent output cost of the pandemic, even though growth rates returned to more normal patterns.

Labour market effects

The labour market experienced severe disruption but recovered more rapidly than initially feared. Unemployment peaked at 7.5% in July 2020 – the highest rate in over two decades. Job losses were concentrated in sectors most affected by restrictions: retail workers, hospitality staff, and employees in sports and personal services.

The labour market's recovery proved remarkably swift. By 2021, unemployment had fallen below 4% for the first time since the early 1970s. This dramatic turnaround reflected both the success of policy support measures and the economy's underlying resilience.

Worked Example: The Speed of Labour Market Recovery

Consider the unemployment trajectory:

- July 2020: Unemployment peaked at 7.5%

- Time to recovery: Approximately 12 months

- 2021 outcome: Unemployment fell below 4%

This represents a decline of more than 3.5 percentage points in roughly one year – one of the fastest labour market recoveries from a major economic shock in Australian history.

Business sector impacts

COVID-19's effects varied dramatically across different industries. Some businesses benefited from changed consumer behaviour, such as food delivery services which saw demand surge. Others faced catastrophic losses.

The biggest losers were businesses dependent on physical presence and social interaction:

- Restaurants and cafes

- Tourism operators

- Accommodation providers

- Entertainment venues

The divergence in business outcomes created what economists termed a "K-shaped recovery" – where some sectors bounced back quickly (the upward arm of the K) whilst others continued to struggle (the downward arm). This contrasted with more typical recessions where most sectors decline and recover together.

Businesses relying on international tourism suffered particularly severe and prolonged impacts, as international border closures lasted far longer than domestic restrictions.

Inflation

The pandemic created unusual price movements that affected inflation measurement. The government's decision to make childcare free for several months, combined with other temporary price changes, produced the first annual decline in Consumer Price Index (CPI) inflation since the early 1960s. The quarterly decline was the largest since 1931.

However, by 2022, inflation pressures intensified dramatically. Cost pressures rose well beyond the RBA's target band of 2-3% due to:

- Demand pressures as the economy reopened

- Global supply chain disruptions

- Russia's invasion of Ukraine, which sharply increased energy prices

This shift from deflation concerns to inflation pressures demonstrated how rapidly economic conditions changed during and after the pandemic.

The Inflation Turnaround

The swing from deflation to high inflation represented one of the most dramatic macroeconomic shifts in recent Australian history. Within the space of two years, policymakers moved from worrying about prices falling to implementing aggressive measures to contain rising inflation.

Income and wealth distribution

The pandemic's long-term effects on income and wealth distribution remain uncertain. However, international evidence suggests concerning trends. Cross-country research by the International Monetary Fund examined five major pandemics of the 21st century (SARS, swine flu, MERS, Ebola and Zika virus). This research found that income inequality worsened following each pandemic outbreak.

Whilst the full distributional impacts will take years to emerge in Australian data, this international evidence suggests COVID-19 may have widened existing inequalities.

Assessing the policy response

Economists reached broad consensus that despite the enormous fiscal and monetary costs, government intervention prevented even greater economic damage.

The counterfactual question – "What would have happened without policy intervention?" – is crucial to understanding the policy response. Economic modelling suggests that without support measures, the recession would have been both deeper and longer, with unemployment potentially reaching double digits and remaining elevated for years.

Without policy support, economic harm would have been both larger and more permanent. Bankruptcies and unemployment would have risen more steeply. Household consumption and business investment would have declined much further. The economy would have taken longer to recover, with more lasting structural damage.

The cumulative GDP loss of $158 billion, whilst substantial, represents a significantly better outcome than would have occurred without intervention. The speed of recovery, particularly in the labour market, vindicated the scale of policy support.

The successful vaccination rollout in Australia and globally proved crucial in enabling economic recovery. As restrictions lifted and health measures eased, economic growth began returning to longer-term patterns, though the economy remained on a lower trajectory than its pre-pandemic path.

Key Points to Remember:

-

COVID-19 ended Australia's 28-year economic growth cycle and triggered the largest macroeconomic policy intervention in Australian history, costing $291 billion by mid-2021

-

JobKeeper was the centrepiece of fiscal policy, providing $89 billion in wage subsidies, whilst the RBA cut the cash rate to 0.1% and undertook asset purchases

-

GDP fell sharply in March and June 2020 (by 0.2% and 6.7% respectively) before recovering from September 2020, though the cumulative loss compared to pre-pandemic trajectory was $158 billion

-

Unemployment peaked at 7.5% in July 2020 but fell below 4% by 2021, the lowest rate since the early 1970s, demonstrating rapid labour market recovery

-

COVID-19's impacts varied dramatically across sectors, with tourism and hospitality suffering severe losses whilst food delivery businesses benefited from changed consumer behaviour

-

The policy response, whilst expensive, successfully prevented a deeper and more prolonged recession, with economists broadly agreeing the intervention was necessary and effective