The Stance of Monetary Policy in Australia (HSC SSCE Economics): Revision Notes

The Stance of Monetary Policy in Australia

How the RBA communicates monetary policy

The Reserve Bank of Australia (RBA) publicly announces its monetary policy position through regular statements about the cash rate target. Following each Board meeting, the RBA releases its decision at 2:30pm, with official meeting minutes published two weeks later.

From 2024 onwards, following reforms recommended by the independent review of the RBA, the communication process will change. The newly established Monetary Policy Board will meet eight times per year to determine monetary policy settings. After each announcement, the Governor will hold a press conference and the Board will release a public statement detailing the discussion and voting outcomes from the meeting.

The stance of monetary policy refers to whether policy is:

- Contractionary (tight): Higher interest rates to reduce inflation

- Expansionary (loose): Lower interest rates to stimulate growth

- Neutral: Interest rates neither stimulating nor restraining economic activity

The monetary policy transmission mechanism

The transmission mechanism describes how changes to the cash rate flow through to affect the broader economy. This process involves multiple channels and operates with significant time lags.

How a policy tightening works

When the RBA raises the cash rate target, the following sequence occurs:

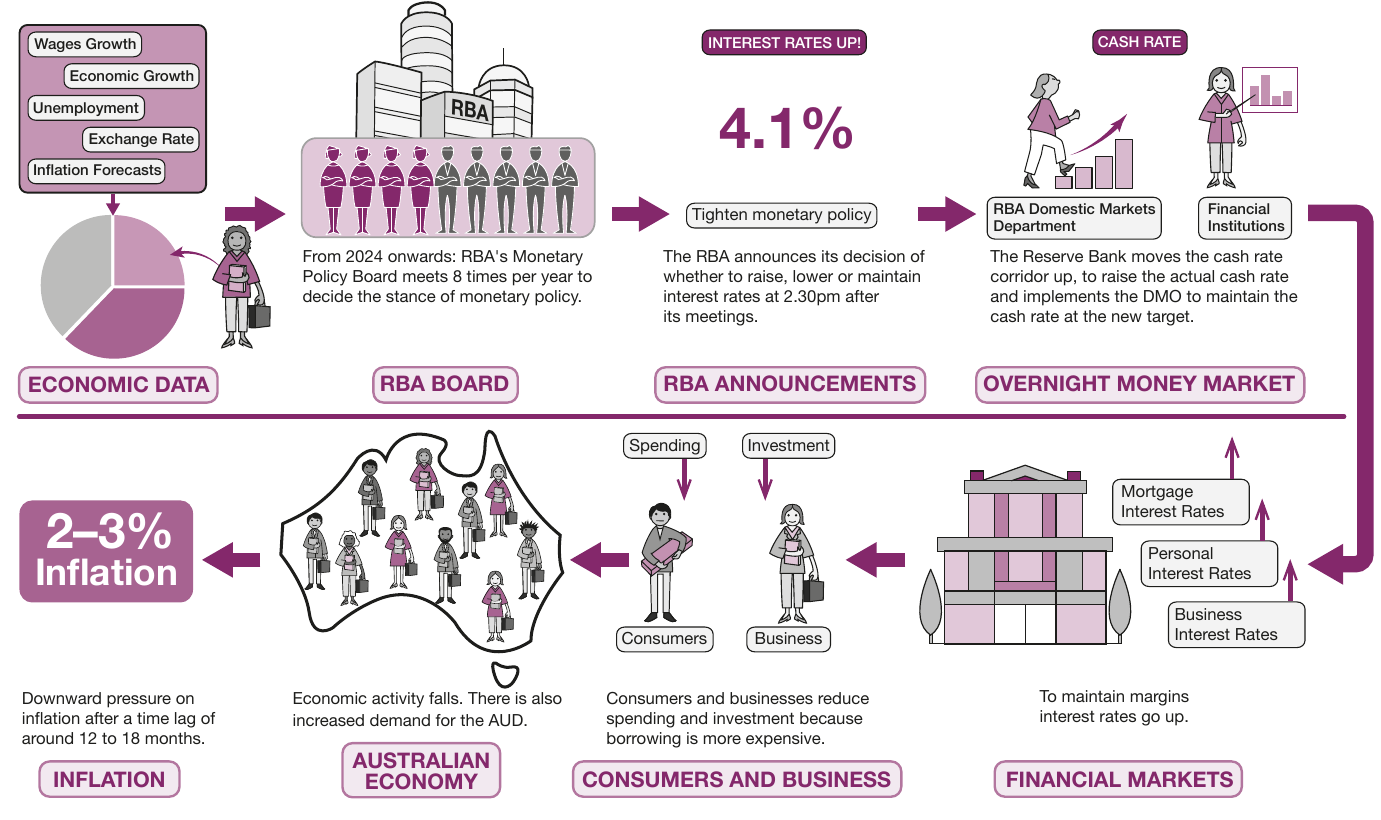

Step 1: Economic data analysis The RBA examines key economic indicators including wages growth, unemployment rates, economic growth, exchange rate movements, and inflation forecasts.

Step 2: Board decision The Monetary Policy Board meets to assess economic conditions and votes on whether to raise, lower, or maintain the cash rate target.

Step 3: Official announcement The RBA announces its decision at 2:30pm following the meeting. For example, an announcement might raise the cash rate to 4.1%.

Step 4: Overnight money market operations The RBA's Domestic Markets Department implements Domestic Market Operations (DMO) to move the actual cash rate in the overnight money market to match the new target. This involves adjusting the cash rate corridor.

Step 5: Financial institution response Banks and other financial institutions adjust their lending rates to maintain profit margins. Mortgage rates, personal loan rates, and business lending rates all increase.

Step 6: Consumer and business behaviour Higher borrowing costs reduce spending and investment by households and firms. When credit becomes more expensive, consumers reduce consumption and businesses scale back investment plans.

Step 7: Economic impact Reduced spending and investment slow economic activity. This downward pressure on aggregate demand eventually reduces inflationary pressures in the economy.

Step 8: Inflation outcome After a time lag of 12 to 18 months, inflation falls back towards the RBA's target range of 2-3%. Simultaneously, demand for the Australian dollar may increase due to higher domestic interest rates, affecting the exchange rate.

An expansionary policy (rate reduction) operates through the opposite effects, stimulating spending and economic activity.

Understanding Policy Lags

The monetary policy transmission mechanism operates with significant time delays. Changes to the cash rate take 12 to 18 months to fully affect inflation. This lag means the RBA must make decisions based on economic forecasts rather than current conditions, making monetary policy particularly challenging during periods of rapid economic change.

Historical trends in Australian interest rates

Interest rates in Australia have fluctuated significantly over the past three decades as the RBA has adjusted monetary policy to respond to changing economic conditions.

The cash rate chart reveals several distinct patterns:

Periods of rapid decline:

- Early 1990s: Rates fell sharply from approximately 18% to around 5%

- Late 2000s: Rates decreased rapidly during the Global Financial Crisis

Periods of rapid increase:

- Mid-1990s: Sharp rises in response to inflationary pressures

- Early 2020s: Aggressive rate increases to combat post-pandemic inflation

Periods of gradual change:

- 2000s: Slow increases during the commodity boom

- 2010s: Gradual decreases as inflation remained persistently low

Historic lows:

- The cash rate reached unprecedented lows during the COVID-19 pandemic, falling to 0.10% in 2020

Case study: How fast is too fast?

Case Study: The 2022-2023 Rapid Tightening Cycle

Between May 2022 and July 2023, the RBA implemented 12 interest rate increases, including 10 consecutive rises, lifting the cash rate from its pandemic low of 0.1% to above 4%. This rapid tightening cycle aimed to control inflation but generated significant debate.

The Economic Context: The increases were necessary given high inflation and low unemployment in the Australian economy. However, economists expressed concern about the pace of adjustment. AMP chief economist Shane Oliver warned in July 2023 that raising rates too aggressively could "tip [the economy] over the edge."

Impact on Households: For mortgage holders, the impact was substantial. Monthly repayments on a typical $600,000 mortgage increased by almost two-thirds, rising from $2,185 to $3,559 across the 12 increases. This placed many households into mortgage stress.

The Debate: Some economists argued the rapid increases didn't allow sufficient time for monetary policy lags to take effect. Economist Ross Garnaut suggested in May 2023 that "the responsible thing is to pause until we see those effects [of lifting interest rates]."

Treasurer Jim Chalmers acknowledged the difficulty, urging the RBA to defend its decision while warning that "there will be a lot of Australians who will find this decision difficult to understand and difficult to cop."

International Comparison: Internationally, Australia's experience was relatively moderate compared to other developed economies. The most extreme example occurred in Türkiye, where lack of central bank independence led to erratic policy. President Erdogan dismissed three central bank governors to avoid rate increases during an election campaign. After his re-election, with official inflation exceeding 40%, he appointed a new central banker who raised rates from 8.5% to 15% in a single move, causing a sharp economic downturn.

Recent monetary policy chronology

Early 2000s: Tightening cycle The RBA increased interest rates to address inflation arising from two sources: depreciation of the Australian dollar and the introduction of the Goods and Services Tax (GST).

Mid-2000s: Commodity boom Initially, the RBA loosened policy to support growth during a mild economic slowdown. As the mining boom intensified and commodity prices surged, rates were gradually raised to contain emerging inflationary pressures.

2008-2009: Global Financial Crisis response Concern about potential spillover effects from the global financial crisis prompted dramatic action. The RBA reduced the cash rate to 3%, a 50-year low at the time, to cushion the Australian economy.

2009-2011: Post-crisis normalisation As crisis risks receded, the cash rate rose to 4.75% by late 2010. With the domestic recovery gaining momentum and strong mining sector growth, the RBA's focus returned to preventing inflation.

2011-2018: Extended low-rate environment Monetary policy remained expansionary for an unusually long period. Low inflation and below-average economic growth prompted the RBA to lower the cash rate target to a historic low of 1.5% in 2016, where it remained until 2019.

2019-2021: COVID-19 pandemic Subdued economic conditions, modest employment growth, and persistently low inflation motivated further easing in 2019, with the cash rate falling to 0.75%. Following the COVID-19 outbreak, the RBA slashed the rate to 0.1% and introduced unconventional measures including quantitative easing and yield curve control to strengthen the financial system and support economic recovery.

2022 onwards: Inflation-fighting tightening Rising inflation prompted the RBA to increase interest rates earlier than expected. Twelve rate increases between mid-2022 and mid-2023 lifted the cash rate above 4%, marking one of the most aggressive tightening cycles in recent history.

Factors determining monetary policy stance

The RBA considers five main factors when determining the appropriate stance of monetary policy:

1. The low inflation objective

Both the government and the RBA are committed to maintaining price stability through the inflation target framework. The target requires average inflation to remain between 2% and 3% over the medium term. Monetary policy serves as the primary tool for achieving this objective.

When inflation rises above the target band, the RBA typically tightens policy by raising interest rates. Conversely, when inflation falls below target or threatens to remain too low, expansionary policy aims to stimulate demand and prevent deflation.

The 2-3% target range represents a compromise. It's high enough to avoid deflation risks but low enough to preserve purchasing power and avoid the costs of high inflation. This framework has been in place since the early 1990s and has helped anchor inflation expectations.

2. Inflationary expectations

Managing expectations about future inflation is crucial for monetary policy effectiveness. When households and businesses expect sustained low inflation, they incorporate these expectations into wage negotiations and pricing decisions. This creates a self-reinforcing cycle supporting price stability.

If inflationary expectations become unanchored and rise significantly, businesses plan higher price increases and unions demand larger wage rises. This makes inflation more difficult to control and may require more aggressive monetary policy tightening.

The Importance of Central Bank Credibility

The RBA will maintain high interest rates for as long as necessary to reduce elevated inflationary expectations. Credibility is essential - if the public doubts the RBA's commitment to the inflation target, expectations may drift upward even if current inflation is within the target band.

3. Labour costs

Future interest rate movements depend heavily on inflation trends, and labour costs represent one of the most significant drivers of inflation. Since wages comprise a large share of business costs, changes in wage growth flow through to prices.

The RBA closely monitors the Wage Price Index (WPI) published by the Australian Bureau of Statistics. This measure tracks changes in wage rates while controlling for changes in the composition and quality of jobs.

Productivity growth is equally important. If wages rise in line with productivity improvements, unit labour costs remain stable and inflationary pressure is contained. However, when wage growth exceeds productivity gains, unit labour costs rise and firms face pressure to increase prices.

Recent debates have focused on whether strong wage growth in tight labour markets will translate into sustained inflationary pressure or whether productivity improvements will offset higher wages.

4. Unemployment and economic growth

The RBA has a dual mandate: maintaining price stability while promoting full employment and economic prosperity. The unemployment rate and economic growth rate provide crucial information about whether the economy is operating near its capacity constraint.

When the economy operates close to full capacity - with high resource utilisation and low unemployment - continued growth in aggregate demand cannot be met by increased output. Instead, excess demand spills over into higher prices, creating inflationary pressure.

If growth is strong and unemployment is low (suggesting the economy is near capacity), the RBA may raise rates to prevent overheating. Conversely, if growth is weak and unemployment is elevated (indicating spare capacity), expansionary policy can stimulate demand without generating inflation.

The Phillips Curve and NAIRU

The relationship between unemployment and inflation, described by the Phillips Curve, guides these policy decisions. However, the RBA must estimate the Non-Accelerating Inflation Rate of Unemployment (NAIRU) - the lowest sustainable unemployment rate consistent with stable inflation.

5. External factors

Australia's deep integration with the global economy means international conditions consistently influence RBA monetary policy decisions. Several channels connect global developments to domestic policy settings.

Global growth: If international economic conditions deteriorate, Australia faces slower export growth, weaker business confidence, and higher unemployment. The RBA may reduce interest rates pre-emptively to cushion the domestic economy against external shocks.

Global financial markets: The RBA monitors international financial markets for early warning signs of economic volatility or emerging inflationary pressures. Financial contagion can spread rapidly across borders, so the RBA must respond quickly to maintain stability.

Exchange rate channel: The exchange rate forms an important component of the monetary policy transmission mechanism. When the RBA adjusts interest rates, this affects the relative attractiveness of Australian dollar assets, influencing capital flows and the exchange rate. A stronger dollar helps contain inflation by reducing import prices, while a weaker dollar has the opposite effect.

International monetary policy: Actions by major central banks, particularly the US Federal Reserve, affect global interest rates and capital flows. If other central banks tighten policy while the RBA maintains low rates, this could lead to currency depreciation and imported inflation.

Global inflation: Overseas inflation trends affect Australia through import prices and can influence domestic inflation expectations. High global inflation, such as experienced in 2022-2023, may require the RBA to tighten policy even if domestic demand is subdued.

RBA performance and criticism

Overall, the RBA has achieved considerable success in maintaining inflation within the target band over the long term. The inflation-targeting framework has provided a stable nominal anchor for the economy.

However, the RBA has faced criticism at various times. Prior to COVID-19, inflation consistently remained below the 2-3% target, averaging around 1.6% from 2016 to 2019. Some commentators argued monetary policy wasn't sufficiently expansionary during this period.

During the pandemic, criticism emerged from the opposite direction. Some argued the RBA's policy stance was too expansionary and its "forward guidance" - stating the cash rate was very unlikely to rise until 2024 - reflected poor economic judgment. When inflation surged unexpectedly, the RBA was forced to raise rates much earlier than indicated, undermining the credibility of its guidance.

These concerns, along with questions about the RBA's governance structure and decision-making processes, prompted an independent review in 2023. The review recommended significant reforms, including splitting monetary policy decisions to a separate Monetary Policy Board meeting eight times per year.

Key Points to Remember:

-

Communication: The RBA announces its monetary policy stance through cash rate target decisions, with meetings from 2024 conducted by the Monetary Policy Board eight times annually

-

Transmission mechanism: Changes to the cash rate flow through multiple channels - affecting bank lending rates, consumer and business spending, investment decisions, and ultimately inflation after a 12-18 month lag

-

Historical variation: Australian interest rates have fluctuated dramatically over the past three decades, from highs near 18% in 1990 to historic lows of 0.1% during COVID-19

-

Five key factors: The RBA's monetary policy stance reflects:

- The 2-3% inflation target

- Inflationary expectations

- Labour costs and wage growth

- Unemployment and economic growth

- External factors including global conditions

-

Recent policy: Following unprecedented expansionary measures during COVID-19, the RBA implemented rapid interest rate increases from 2022 onwards to combat rising inflation, demonstrating the challenges of balancing price stability with full employment