The Money Market (HSC SSCE Economics): Revision Notes

The Reserve Bank of Australia

The Reserve Bank of Australia (RBA) is Australia's central bank and plays a crucial role in managing the country's interest rates. This influence comes from the RBA's responsibility for directly managing the cash rate – the interest rate in the overnight money market where banks borrow and lend to each other for very short periods, often literally overnight.

Understanding how the RBA manages the cash rate is essential foundation knowledge for HSC Economics. The cash rate influences many other interest rates in the economy (such as mortgage rates) and ultimately affects the overall level of economic activity. This makes it a powerful policy tool called monetary policy.

The mechanics of how the RBA controls the cash rate can be explained through three key mechanisms: exchange settlement accounts, the policy interest rate corridor, and open market operations. Understanding each of these mechanisms is crucial for explaining how the RBA maintains control over interest rates.

Exchange settlement accounts

Banks must hold a certain proportion of their funds with the Reserve Bank in special accounts called exchange settlement (ES) accounts. These accounts are used to settle payments between different banks.

How interbank payments work

When a customer of one bank makes a payment to someone who banks with a different institution, funds need to flow between the two banks.

Payment Flow Example: Interbank Transfer

If an ANZ customer uses a debit card to buy something from a business that banks with Westpac, funds must transfer from ANZ to Westpac. These payments are made by transferring funds between the banks' ES accounts at the RBA.

This process happens automatically and instantaneously for the customer, but behind the scenes it requires the movement of ES balances between the two banks.

Every trading day, many interbank payments occur. By the end of the day, some banks will have a shortage of ES funds (they don't have enough to meet all their payment obligations), while other banks will have a surplus of ES funds (more than they need to hold).

The overnight money market

The overnight money market (also called the short-term money market) is where banks with ES fund shortages can borrow from banks with ES fund surpluses. This market ensures all banks can always meet their interbank payment obligations.

Like any financial market, the interaction of demand (from borrowers) and supply (from lenders) determines the market price – in this case, the interest rate, which is the cash rate. For example, when the supply of funds from banks with excess ES balances increases, the cash rate falls.

Unlike other financial markets, the RBA intervenes heavily in this market to ensure the actual cash rate matches a target that the RBA sets and announces publicly every month (except January). This intervention is what gives the RBA effective control over interest rates in the economy.

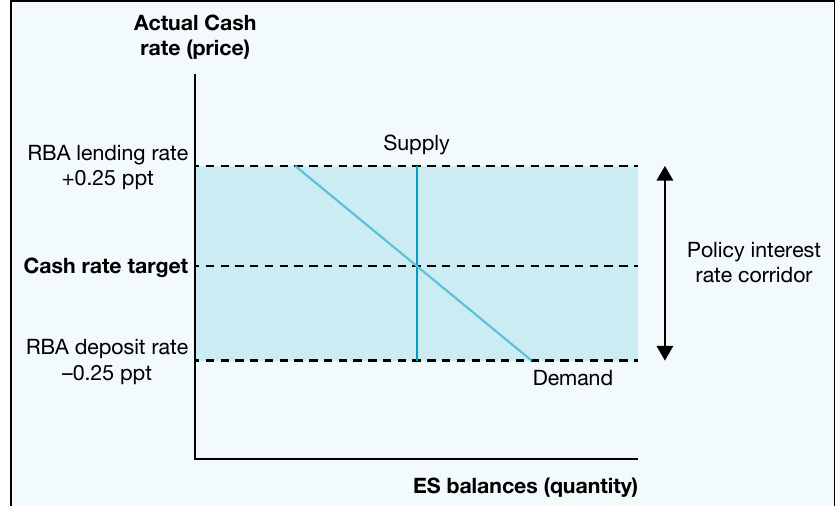

The policy interest rate corridor

The RBA cannot directly set the cash rate at its chosen target. Instead, it uses a clever mechanism called the policy interest rate corridor to ensure the actual cash rate can never stray far from the target.

The floor: RBA deposit rate

The RBA pays interest to banks on funds held in their ES accounts. This interest rate is always percentage points below the cash rate target.

Calculating the Floor Rate

If the cash rate target is , the RBA's deposit rate would be .

This creates a "floor" or minimum value for the cash rate. Banks with excess ES balances won't lend to other banks in the overnight market if the cash rate falls below this level – they would earn better returns by simply leaving their funds in their ES account with the RBA.

The ceiling: RBA lending rate

The RBA is always willing to lend ES balances directly to banks outside the overnight market. The interest rate on these loans is always percentage points above the cash rate target.

Calculating the Ceiling Rate

If the cash rate target is , the RBA's lending rate would be .

This creates a "ceiling" or maximum value for the cash rate. Banks that need to borrow ES balances won't pay more than this rate in the overnight market – they would simply borrow directly from the RBA instead.

How the corridor works

Together, the floor (deposit rate) and ceiling (lending rate) form the policy rate corridor. No rational bank would transact outside this corridor. Since the RBA's target is always exactly in the middle of the corridor, the actual cash rate closely follows the target.

The diagram above shows how supply and demand interact in the overnight money market, with the policy corridor constraining the actual cash rate to stay close to the target. The corridor creates boundaries that prevent the cash rate from deviating significantly from the RBA's intended target.

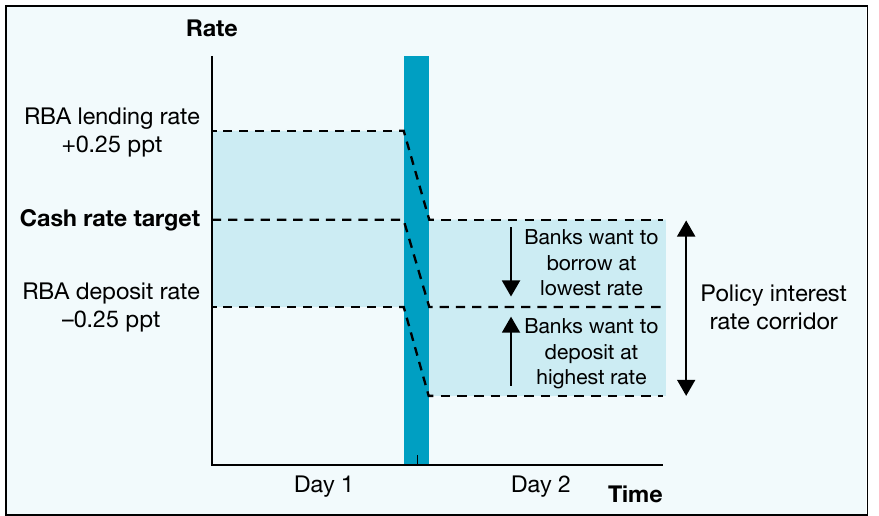

Implementing changes to the cash rate target

When the RBA announces a change to its cash rate target, the corridor automatically adjusts. The floor and ceiling shift immediately to keep the target in the middle, and banks are instantly incentivised to borrow and lend within the new range.

This means changes to the cash rate happen as soon as the RBA announces a target change – no additional action is required. The corridor mechanism ensures immediate implementation of monetary policy decisions.

The diagram above illustrates how the policy corridor narrows when the RBA decreases the cash rate target. Banks want to borrow at the lowest rate and deposit at the highest rate, so they adjust their behaviour to operate within the new corridor.

Open market operations

While the policy corridor keeps the cash rate close to target, daily fluctuations in demand for ES balances could still cause the actual cash rate to bounce around within the corridor. The RBA prevents this through open market operations (OMO).

Managing ES fund supply

OMO refers to the purchase and sale of financial securities by the RBA in exchange for ES balances. These transactions directly affect the supply of ES funds available in the overnight market.

When demand for ES funds increases:

- The RBA buys financial securities (such as government bonds) from banks

- In exchange, the RBA deposits additional funds into banks' ES accounts

- This increases the supply of ES funds to meet the higher demand

- The cash rate stays at target

When demand for ES funds decreases:

- The RBA sells financial securities to banks

- In exchange, the RBA withdraws funds from banks' ES accounts

- This decreases the supply of ES funds to match the lower demand

- The cash rate stays at target

Types of open market operations

OMO can involve:

- Outright purchases or sales: The RBA permanently buys or sells securities (e.g., second-hand Commonwealth government bonds)

- Repurchase agreements (repos): The "seller" of a security agrees to buy it back from the "buyer" at a later date

In practice, the RBA prefers using repos because they are more flexible and allow more precise management of ES supply than outright transactions. Repos can be reversed easily if market conditions change.

Summary of RBA's control mechanisms

The RBA uses two complementary tools to control the cash rate:

- The policy rate corridor implements changes to the cash rate target

- Open market operations ensure the cash rate stays at its target every day when ES fund demand changes

Together, these mechanisms give the RBA effective control over the cash rate.

Why the cash rate is important

Foundation of the interest rate structure

The cash rate provides the foundation for all interest rates in the economy. When the cash rate increases, it becomes more expensive for banks to borrow funds in the short-term money market. This increases banks' overall cost of borrowing.

To maintain their profit margins, banks pass these higher costs on to their customers by raising lending rates for mortgages and other longer-term loans. Similarly, when the cash rate falls, banks reduce their lending rates to pass on the cost savings.

Impact on economic activity

Changes in the general level of interest rates directly impact economic activity through their effects on consumption and investment spending.

When interest rates fall:

- Existing borrowers pay less on their debts

- New borrowers find it easier to obtain loans

- Consumption and investment spending increase

- Economic activity rises

When interest rates rise:

- Existing borrowers pay more on their debts

- New borrowers find it harder to obtain loans

- Consumption and investment spending decrease

- Economic activity falls

Monetary policy

The Reserve Bank's use of interest rates to affect economic activity is called monetary policy. The RBA can implement two types of monetary policy:

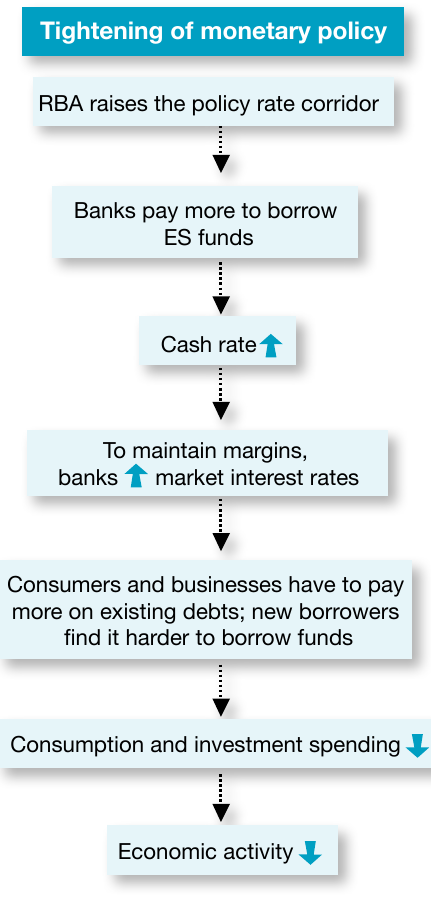

Tightening (contractionary) monetary policy: Raising interest rates to reduce economic activity

The flowchart above shows the transmission mechanism for tightening monetary policy, from the RBA raising the policy corridor through to reduced economic activity.

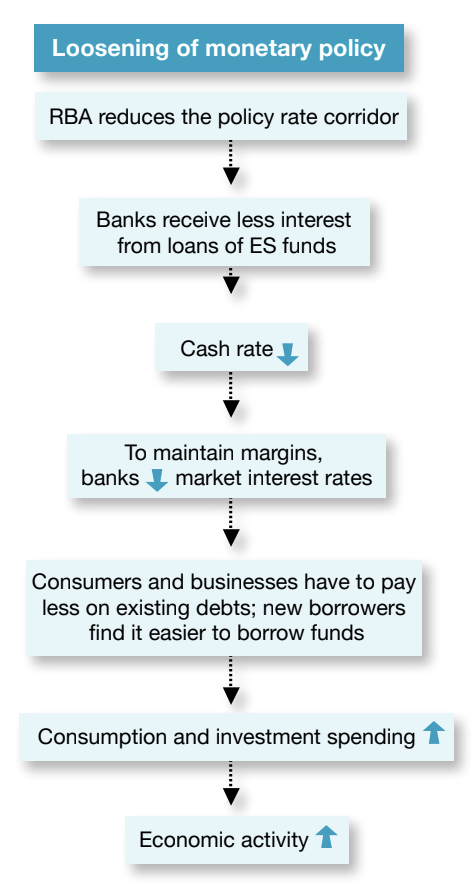

Loosening (expansionary) monetary policy: Lowering interest rates to stimulate economic activity

The flowchart above shows the transmission mechanism for loosening monetary policy, from the RBA reducing the policy corridor through to increased economic activity.

Exam guidance

Key Exam Tips:

When answering questions about the RBA and the cash rate:

- Explain the policy corridor mechanism by clearly identifying both the floor (deposit rate) and ceiling (lending rate) and how they constrain the cash rate

- Analyse the transmission mechanism by tracing the step-by-step process from RBA action through to economic outcomes

- Evaluate the effectiveness of monetary policy by considering time lags, the dependence on banks passing on rate changes, and other factors affecting economic activity

- Use precise terminology: Always distinguish between the cash rate target and the actual cash rate, and between the overnight money market and other financial markets

Key Points to Remember:

- The cash rate is the interest rate in the overnight money market where banks borrow and lend ES balances to each other

- The policy interest rate corridor constrains the cash rate to within percentage points of the RBA's target (deposit rate creates floor at target ppt; lending rate creates ceiling at target ppt)

- Open market operations involve the RBA buying or selling securities to manage the supply of ES funds and keep the cash rate at target daily

- Changes in the cash rate flow through to other interest rates in the economy, affecting consumption and investment spending, and ultimately economic activity

- Monetary policy is the RBA's use of interest rates to influence economic activity – tightening raises rates to slow the economy, loosening lowers rates to stimulate the economy