Borrowers and Lenders: The Demand for and Supply of Funds (HSC SSCE Economics): Revision Notes

Borrowers and Lenders: The Demand for and Supply of Funds

The money market is where funds are borrowed and lent. Like other markets, it has demand (borrowers), supply (lenders), and a price (interest rates). Understanding this market is essential because money underpins so many economic activities, from buying goods to saving for retirement.

Overview of the money market

The money market operates differently from typical markets. Borrowers act as "consumers" demanding funds, while lenders act as "producers" supplying funds. The price in this market is the interest rate that borrowers pay to lenders.

The price is not determined solely by market forces. The Reserve Bank of Australia plays a key role in influencing interest rates across the economy, making the money market unique in its operation.

Borrowers: the demand for funds

Three main groups borrow money in the economy: individuals, businesses, and governments. Each has different reasons for borrowing and faces different conditions.

Individual borrowers

Individuals typically borrow for personal reasons. The most common type of borrowing is a mortgage for purchasing a family home. When someone takes out a mortgage, the bank receives the home as security for the loan. This means if the borrower fails to make repayments (defaults), the bank can sell the house to recover the debt, returning any remaining funds to the borrower.

Individuals also borrow for shorter-term needs such as:

- Purchasing vehicles

- International travel

- Educational courses

- Credit card purchases for everyday items

These shorter-term loans are usually unsecured, meaning there is no asset the lender can claim if the borrower defaults. This higher risk explains why interest rates on these loans, particularly credit cards, are significantly higher than mortgage rates.

Business borrowers

The business sector accounts for the largest share of borrowing in the Australian economy. Businesses need access to funds to:

- Expand production capacity

- Invest in research and development

- Complete special projects

- Manage cash flow fluctuations

Businesses can raise funds in two main ways:

- Directly: By issuing shares (equity) or bonds (debt) to investors

- Indirectly: By borrowing from financial institutions such as banks

Even businesses that primarily raise funds through shares or bonds often need short-term loans. For example, a tourism business may experience seasonal fluctuations in revenue but has relatively constant expenses. An overdraft facility helps bridge gaps in cash flow during quieter periods.

Government borrowers

Governments participate in financial markets as borrowers for several reasons:

- Economic stimulus: When economic growth is slow, governments may borrow to increase spending or provide tax cuts to stimulate activity

- Budget deficits: Sometimes government spending grows faster than revenue unintentionally, requiring borrowing

- Infrastructure funding: For long-term assets like roads, bridges, or railways, economists often argue it is appropriate to borrow and repay over the asset's lifetime. This ensures future beneficiaries help pay for the investment.

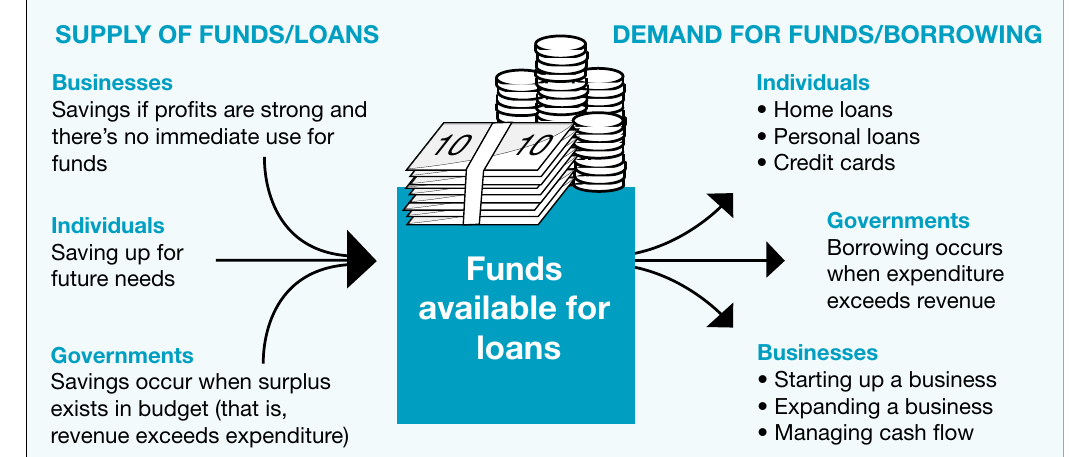

Visual summary of borrowing and lending

This diagram illustrates how funds flow from lenders to borrowers in the financial system. On the supply side, individuals save for future needs, businesses save surplus profits, and governments save when running budget surpluses. On the demand side, individuals need loans for homes and personal expenses, governments borrow when spending exceeds revenue, and businesses seek funds for starting up, expanding, and managing cash flow.

Factors affecting the demand for funds

Individuals and businesses must decide how to hold their surplus funds. The fundamental choice is between holding money (currency and bank deposits) or purchasing financial assets (such as bonds or shares).

The liquidity trade-off

Liquidity refers to how easily a financial asset can be converted into cash for use as a medium of exchange. Holding money provides maximum liquidity, allowing easy access when funds are needed. However, holding cash offers no return and its value erodes over time due to inflation.

Financial assets like shares can provide returns. For example, shareholders may receive dividend payments from company profits. But financial assets carry risks – their value can change based on market conditions, potentially resulting in capital gains or losses.

Motives for holding money

People hold money (rather than investing in financial assets) for three main reasons:

1. Transactions motive: Individuals need money for day-to-day purchases of goods and services. Regular payments require holding a certain amount of currency, as most financial assets like shares cannot be used directly to pay for everyday purchases.

2. Precautionary motive: Beyond predictable transactions, people face unpredictable circumstances and emergencies (such as illness) requiring immediate access to liquid funds.

3. Speculative motive: Financial assets can generate capital gains (when prices rise) or losses (when prices fall). If people expect asset values to decline, they will sell their financial assets and convert them into money to avoid losses.

Financial system sophistication

The sophistication of the financial system affects how much liquidity people need. In a basic system with only bank branches and passbook accounts, people must hold more cash because accessing funds is difficult.

Modern financial systems make it easier to convert financial assets into cash, reducing the demand for liquidity. When markets are "deep" (have many buyers and sellers) and function efficiently, individuals can confidently hold more savings in less liquid assets.

Changes in cash usage

Research by the Reserve Bank of Australia shows significant changes in how Australians use cash:

- Cash usage declined from 69% of transactions in 2007 to 37% in 2016

- Electronic payment technologies (contactless cards, mobile payments) have grown rapidly due to convenience

- Cash remains dominant for small-value transactions

- Some groups (elderly, lower-income households) still rely heavily on cash

- Despite reduced cash transactions, the value of banknotes in circulation continues growing, suggesting continued demand for liquidity beyond everyday transactions

Business demand factors

Business borrowing is influenced by several factors:

- Cash flow: Whether operational cash flow is sufficient to cover expenses

- Economic conditions: Businesses are more willing to take on debt during good economic times

- Interest rates: Lower interest rates encourage more business borrowing

Household debt in Australia

Australian household debt has grown dramatically. The ratio of household debt to income increased from 41% in the 1980s to approximately 190% by mid-2019, making Australian households the second most heavily indebted in the world. Housing-related debt (mortgages) accounts for over 70% of total household debt.

Key drivers of this growth include:

- Low interest rates: Interest rates are roughly one-third of their late-1980s levels, meaning households can afford larger monthly repayments

- Rising house prices: Buyers seek to profit from property value appreciation

- Strong property investment: Borrowing for investment properties (not primary residences) represents over 25% of household debt

- Financial deregulation: Increased competition has lowered borrowing costs and expanded available options

- Growing superannuation: Higher total household assets make people more comfortable with debt

While household debt has increased substantially, lower interest rates have partially offset the impact. The cost of servicing household debt has remained relatively stable in recent years despite higher debt levels.

Financial innovation

Financial innovation affects consumer demand for liquidity and reshapes financial markets. Technology has been a key driver of innovation in Australian financial services:

- ATMs: Provide 24-hour access to funds from bank accounts

- EFTPOS: Electronic funds transfer at point of sale

- Online banking: Internet-based banking and payment systems

- Internet stockbrokers: Companies like E-Trade and CommSec have reduced trading costs and made share investment accessible to small investors

- Buy now pay later: Products from companies like Afterpay allow consumers to receive goods immediately and pay in instalments without credit cards

- Mortgage brokers: Help individuals find suitable loan products and link lenders with borrowers

- Contactless payments: PayPass and similar systems reduce transaction time by 25% compared to traditional cards

- Digital currencies: Bitcoin and similar currencies allow electronic payments without intermediaries like banks, reducing transaction costs

These innovations have reduced the need for people to hold large amounts of cash for transactions.

Opportunity cost of holding liquid funds

The main opportunity cost of holding liquid funds is the forgone returns (interest) that could have been earned from financial assets. People will hold money rather than financial assets as long as the benefits of liquidity (lower transaction costs, no risk of capital losses) outweigh the costs (forgone returns).

Lenders: the supply of funds

Individuals, businesses, and governments participate in financial markets as lenders when seeking returns on their wealth.

Individual lenders

When individuals place deposits in financial institutions, they are effectively lending money to that institution in exchange for a return. People with wealth they do not wish to spend immediately have several options:

- Invest in assets like residential property

- Buy shares

- Place money in interest-bearing deposits at financial institutions (lower risk option)

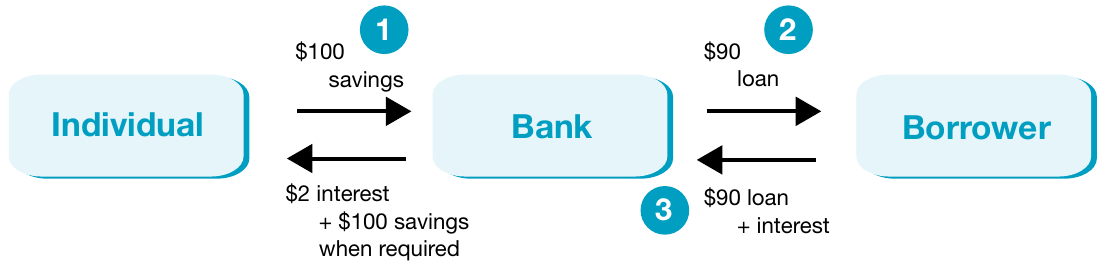

Worked Example: How Banks Intermediate Between Savers and Borrowers

This diagram shows the banking flow cycle:

Step 1: An individual deposits $100 in savings at a bank

Step 2: The bank then lends $90 to a borrower (keeping some in reserve)

Step 3: The borrower repays the $90 plus interest to the bank

Step 4: The bank returns $2 interest plus the original $100 savings to the individual when required

This illustrates how banks act as intermediaries between savers and borrowers.

Business lenders

Successful businesses may have strong cash flow and good profits but no immediate expansion plans. In such cases, they may deposit funds in a financial institution. If interest rates make deposits more lucrative than business investment, firms are more likely to supply funds to the financial system.

Government lenders

Historically, governments have participated in financial markets mainly as borrowers. However, when a government runs a budget surplus (revenue exceeds spending), it can become a lender by:

- Paying off outstanding debts from previous years

- Maintaining positive financial balances (lending money through the financial sector)

International sector

The international sector provides an important source of funds for Australian borrowers. Australia has historically had low savings rates and relied on overseas savings to finance domestic consumption and investment.

When Australians borrow from overseas, this creates a foreign liability that must be repaid. Australia's net foreign debt exceeded $1.1 trillion in 2019. The importance of international lending was highlighted during the global financial crisis, when international credit shortages forced Australian banks to raise interest rates beyond official Reserve Bank increases to attract overseas funds. The Australian Government also guaranteed overseas borrowings by Australian banks to reassure international lenders.

Remember!

Key Points to Remember:

- The money market brings together borrowers (demanding funds) and lenders (supplying funds), with interest rates as the price

- Individuals, businesses, and governments all participate as both borrowers and lenders for different reasons

- People hold money for three main motives: transactions, precautionary, and speculative purposes

- Liquidity (ease of converting assets to cash) is the key trade-off when deciding between holding money and financial assets

- Australian household debt reached 190% of income by 2019, driven mainly by low interest rates and rising house prices

- Financial innovation (ATMs, online banking, contactless payments) has reduced the need for holding large amounts of cash

- The sophistication of financial systems affects how much liquidity individuals and businesses need to hold