Interest Rates (HSC SSCE Economics): Revision Notes

Interest Rates

Interest rates represent one of the most significant prices in an economic system. They serve as the mechanism that creates balance in financial markets, ensuring the quantity of funds offered by lenders matches the quantity demanded by borrowers.

What are interest rates?

Interest rates are the cost of borrowing money, expressed as a percentage of the total amount borrowed. They can also be understood as the rate of return (or yield) that lenders receive on financial assets such as bonds.

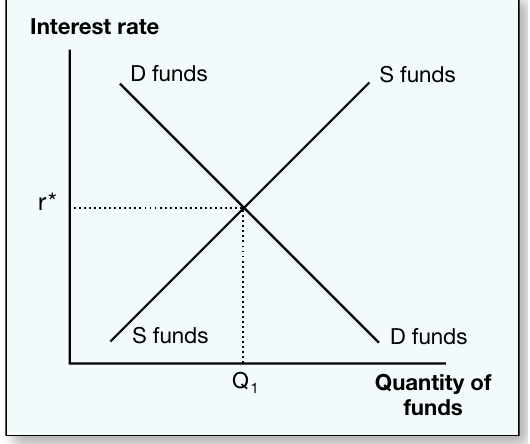

When we analyse financial markets, the demand-for-funds curve shows how much money borrowers want to borrow at different interest rates. The supply-of-funds curve shows how much money lenders are willing to provide at different rates. These two forces theoretically interact to determine the equilibrium interest rate.

Interest rate determination model

The traditional model assumes that lenders will supply more funds as interest rates rise, while borrowers will demand more funds as interest rates fall. This creates the classic supply and demand relationship shown below.

At the equilibrium point (), the quantity of funds supplied equals the quantity demanded (). Any change in the supply or demand for funds will shift these curves and alter the equilibrium interest rate.

However, this theoretical model does not fully capture how financial markets actually operate. In reality, the supply of funds (savings) tends to be very unresponsive to interest rate changes—economists describe this as being highly inelastic. More importantly, interest rates in Australia are not determined purely by market forces. Instead, the Reserve Bank of Australia indirectly controls interest rates through its monetary policy operations.

Types of interest rates

Borrowing rates vs lending rates

Financial institutions play a dual role in the money market. When they accept deposits from savers, they act as borrowers of funds and pay a borrowing rate on these deposits. When they provide loans to customers, they charge a lending rate.

Banks profit by ensuring their lending rates exceed their borrowing rates. The gap between these two rates is called the interest rate differential or net interest margin. This margin covers the bank's operating costs and provides profit.

Worked Example: Interest Rate Differential

If a bank pays 2% on savings deposits (borrowing rate) but charges 5% on personal loans (lending rate), the interest rate differential is 3 percentage points.

This 3% margin allows the bank to cover operating expenses and generate profit from its lending activities.

Short-term vs long-term interest rates

Interest rates are also classified based on the maturity period of the financial instrument:

Short-term interest rates apply to loans with a maturity of less than one year. For instance, the Commonwealth Government issues Treasury notes for just 13 or 26 weeks. These instruments allow governments and businesses to meet immediate funding needs.

Long-term interest rates apply to loans with extended maturity periods. Treasury bonds might be issued for 5, 7, or 10 years, while home mortgages can extend up to 25 years.

Long-term securities typically carry higher interest rates than short-term ones. This occurs for two reasons:

- Increased risk: More can change over a longer time period—economic conditions, inflation, or the borrower's financial situation might deteriorate

- Lower liquidity: It is more difficult to convert them quickly into cash if the lender needs money urgently

To compensate for these additional risks, lenders demand higher returns on long-term securities.

Factors affecting interest rates

Multiple factors can shift the supply or demand for funds, causing changes in equilibrium interest rates:

Demand for capital goods (investment)

When businesses want to invest in new machinery, equipment, or facilities, they typically need to borrow funds. Stronger investment demand increases the demand for borrowing, putting upward pressure on interest rates.

Two main factors drive investment demand. First, if real wages rise, capital becomes relatively cheaper compared to labour, encouraging firms to invest in machinery instead of hiring workers. Second, during periods of strong economic growth, firms need to expand their productive capacity to meet rising consumer demand, leading to more borrowing.

Level of savings

The amount households and businesses save directly affects the supply of loanable funds. When savings increase, more funds are available for lending, which puts downward pressure on interest rates. Conversely, if people save less and spend more, the reduced supply of loanable funds pushes interest rates upward.

Demand for liquid funds

Liquidity preference describes how much individuals and firms want to hold their wealth in easily accessible forms like cash or bank deposits, rather than in securities like bonds.

If people develop a stronger preference for liquid funds, they may choose to hold money in bank accounts rather than purchasing bonds or other securities. This reduces the supply of loanable funds available in financial markets, putting upward pressure on interest rates.

Inflationary expectations

Inflation erodes the purchasing power of money. If lenders expect inflation to rise, they will demand higher interest rates as compensation for the anticipated loss in value of their financial assets.

Even if the real rate of return (the return adjusted for inflation) remains constant, higher expected inflation leads to higher nominal interest rates. This ensures lenders maintain their real purchasing power.

Government budget position

The government's fiscal position significantly influences interest rates. When government spending exceeds revenue, a budget deficit emerges, forcing the government to borrow from financial markets. This additional demand for funds can push interest rates upward.

Conversely, if the government runs a budget surplus (revenue exceeds spending), it becomes a net lender in financial markets. This extra supply of funds puts downward pressure on interest rates.

International interest rates

In today's globalised economy, capital flows relatively freely across borders. This means domestic interest rates cannot deviate too far from international rates.

If Australian interest rates fall below overseas rates, domestic lenders may invest their funds abroad to capture higher returns. This outflow of capital reduces the supply of loanable funds in Australia, putting upward pressure on domestic interest rates. The opposite occurs when Australian rates exceed international rates—foreign capital flows in, increasing the supply of loanable funds and pushing domestic rates down.

Reserve Bank of Australia operations

The RBA conducts domestic market operations that affect the supply of funds in the short-term money market. These operations allow the RBA to set the cash rate (the interest rate on overnight loans between banks). Changes in the cash rate directly influence short-term interest rates and indirectly affect longer-term rates throughout the economy.

Key Points to Remember:

- Interest rates are the price that balances supply and demand in financial markets, representing both the cost of borrowing for borrowers and the return for lenders

- Financial institutions profit from the interest rate differential—the gap between the borrowing rates they pay on deposits and the lending rates they charge on loans

- Long-term interest rates are typically higher than short-term rates because longer-term securities carry more risk and are less liquid

- Seven key factors affect interest rates: investment demand, savings levels, liquidity preference, inflationary expectations, government budget position, international rates, and RBA operations

- While economic theory suggests interest rates are determined by supply and demand, the RBA actually plays the dominant role in setting interest rates through its monetary policy operations