The Market Economy and Australia's Economy (HSC SSCE Economics): Revision Notes

The Market Economy and Australia's Economy

Introduction to economic systems

A market economy is a system where economic decisions are primarily made by individuals and businesses acting in their own self-interest. In this system, the private sector owns most economic resources, and people can pursue wealth with minimal government interference. This system is also known as capitalism, free enterprise, or laissez-faire economics.

This contrasts with a centrally planned economy, where government planners control economic decisions and public ownership of resources allows government to allocate them as it chooses. Historical examples include the former Soviet Union and Eastern European countries, though no major economy follows this model today.

Pure market economies do not exist in the modern world. The closest historical example was eighteenth- and early nineteenth-century England, which followed a laissez-faire approach (meaning "let things be").

However, this system had significant weaknesses: it allowed resource owners to accumulate extreme wealth whilst the majority faced exploitation and poverty, and it created volatile economic cycles of boom and bust. These problems led to modifications, with governments taking on larger economic roles without moving to full central planning.

Characteristics of a market economy

The market system

A market is a network connecting buyers and sellers who exchange particular products at agreed prices. In a free-market economy, markets exist for all goods and services produced, as well as for the resources used to produce them.

Product markets involve the interaction between consumers (who create demand) and businesses (who create supply) for goods and services. The product market is defined as the interaction of demand for and supply of the outputs of production—that is, goods and services.

When demand and supply change in product markets, this affects the factor market. For instance, if consumers demand more of a product, businesses need additional resources (raw materials, workers) to increase production. To attract these resources from other uses, businesses must offer higher prices, including higher wages for workers.

The factor market is a market for any input into the production process, including natural resources, labour, capital and enterprise.

The price mechanism

The price mechanism is the process by which the forces of supply and demand interact to determine the market price at which goods and services are sold, as well as the quantity produced. This mechanism coordinates economic activity without direct intervention.

Prices are critical because they influence both consumer demand and business supply decisions. Consumers seek the lowest prices to satisfy more wants, whilst businesses seek the highest prices to maximise profits. The price mechanism brings these opposing forces into balance.

Example: The sunglasses market

Consider what happens when unexpectedly sunny weather increases demand for sunglasses:

Step 1: Unexpectedly sunny weather increases consumer demand for sunglasses

Step 2: As consumers compete for limited stock, prices rise

Step 3: Higher prices encourage manufacturers to produce more sunglasses, since they can now sell at better profit margins

Step 4: The price mechanism has communicated consumer preferences to producers through price movements

Conversely: If demand decreased, prices would fall, leading to reduced production.

This demonstrates how the price mechanism communicates consumer preferences to producers through price movements.

Private ownership of property

Individuals have the right to own the means of production (resources) and can use these to generate income and build wealth. Property owners can also sell their property or transfer ownership under conditions they choose. This creates incentives for efficient resource use and encourages investment.

Consumer sovereignty

Consumer sovereignty refers to the manner in which consumers, through market demand, collectively determine what is produced and the quantity of production.

Consumers play a vital role in the market economy. They freely choose how to spend their income to satisfy their wants. Through these spending decisions, consumers ultimately determine which goods and services businesses will produce. Businesses respond by producing whatever is in demand.

This means consumers effectively control the answers to "what to produce?" and "how much to produce?" in a market economy.

Freedom of enterprise

Individuals have the right to use their resources as they choose. This means:

- Entrepreneurs can establish profit-making businesses

- Business owners determine what they produce and how they produce it

- Workers choose their occupations or whether to work at all

This freedom encourages innovation and allows resources to flow to their most valued uses based on individual decisions.

Competition

Competition is the pressure on business firms in a market economy to lower prices or improve the quality of output to increase their sales of goods and services to consumers.

Competition requires large numbers of buyers and sellers in each market. This ensures no single buyer or seller can significantly influence market prices to gain unfair advantage or excessive bargaining power. In a truly competitive market, numerous producers compete in every industry.

When competition weakens and a few large businesses dominate, they may charge higher prices and earn excessive profits at consumers' expense.

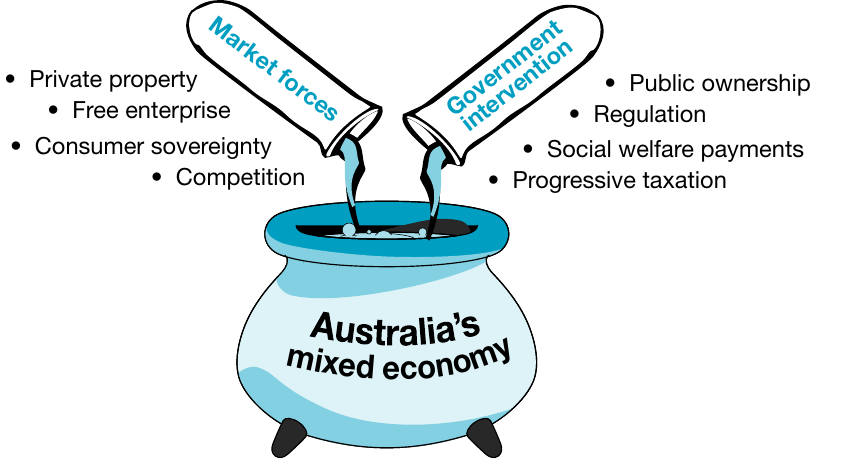

Australia's mixed economy

No economy today operates as purely market-based or completely centrally planned. Instead, all economies combine elements of both systems, creating what economists call mixed economies.

A mixed economy is an economic system where the decisions concerning production and distribution are made by a combination of market forces and government decisions. Each country seeks the optimal balance between relying on market forces and using government intervention to solve the economic problem.

Since the 1980s, mixed economies have generally moved away from government intervention towards greater reliance on market forces. However, the global financial crisis of the late 2000s prompted unprecedented government intervention in financial systems worldwide, demonstrating that the appropriate balance can shift depending on circumstances.

Australia exemplifies a mixed economy. The system combines market-based characteristics (private property, free enterprise, consumer sovereignty, competition) with strategic government intervention (public ownership, regulation, social welfare payments, progressive taxation).

Why governments intervene in the market economy

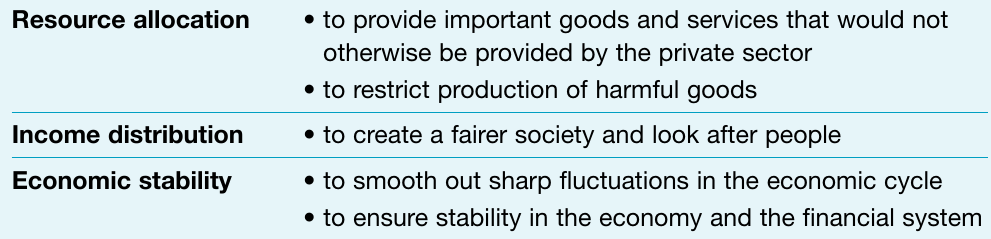

Even though market forces drive most economic activity in Australia, government intervention serves important purposes. Three main justifications exist for government involvement:

Resource allocation

Free markets do not always allocate resources efficiently for society as a whole. Government intervention addresses several issues:

Provision of necessary goods and services: Some essential goods and services won't be provided by private enterprise alone. For instance, Australia historically had government-owned railways because private firms were unwilling or unable to provide the huge capital investment and accept the risks involved. Governments also provide collective goods—such as parks, roads, and national defence—that benefit the entire community but cannot practically be charged on an individual basis.

Government provision of essential services: Certain essential services are better managed by government than private individuals. For example, maintaining a defence force under government control ensures national security and internal stability, rather than relying on private armies.

Markets don't always operate freely, competitively, or in society's best interests. Government regulations prevent producers from exploiting consumers through misleading information or price-fixing agreements with competitors.

Market regulation: Governments may also ban production of undesirable goods and services (such as illicit drugs or certain forms of gambling) and ensure adequate safety standards for all products sold.

Income distribution

Free markets won't necessarily create socially desirable or fair income distribution. Government addresses this through:

Social welfare payments: Under the price mechanism alone, people who don't contribute to production would earn no income. This would leave the elderly, unemployed, and chronically ill without support. In Australia, the government overrides market outcomes by taxing higher-income earners more heavily and providing social welfare payments to those outside the production process. Examples include disability pensions, age pensions, and unemployment benefits.

Progressive income tax: The government redistributes income to achieve more equitable sharing of produced output. Under a progressive income tax system, high-income earners face higher marginal tax rates and pay proportionately more tax than low-income earners. This creates a fairer distribution than pure market outcomes would produce.

Economic stability

Market economies experience business cycle fluctuations. Governments implement macroeconomic (counter-cyclical) policies to smooth these cycles and reduce problems from insufficient or excessive economic activity. Governments also intervene during major economic or financial threats, such as when the 2008 credit crisis brought the global financial system near collapse.

How the mixed economy solves the economic problem

In mixed economies like Australia, markets primarily answer the four fundamental economic questions (what to produce, how much to produce, how to produce, and how production will be shared). However, governments intervene selectively to modify certain market outcomes.

What to produce?

Government influences production in several ways:

- Direct production: Government acts as a producer itself, providing collective goods and services such as schools, roads, bridges, and defence forces. It also competes directly with private enterprise in some areas (for example, ABC television and radio services).

- Production incentives: Government encourages certain production through subsidies, tax incentives, or start-up funding.

- Production restrictions: Government limits or prohibits production of undesirable goods, such as illicit drugs.

How much to produce?

Governments influence the scale of production through various mechanisms:

- Production limits: Government can restrict production of some goods or services. For example, state governments historically regulated the number of taxi licences issued to ensure safe, reliable transport and business viability (though ride-sharing companies like Uber, Ola, and Bolt now challenge this model).

Merit goods are goods and services that are not produced in sufficient quantity by the private sector because individuals do not place sufficient value on them. Governments encourage greater provision of these desirable but under-provided goods and services through subsidies for the arts (theatre, opera, film, fine arts), education, and renewable energy.

- Trade protection: Government can help Australian producers competing with foreign firms increase output through protectionist trade policies, including import restrictions, taxes on goods entering Australia, or subsidies (cash payments or tax reductions) to Australian producers.

How to produce?

Government influences factor costs and their use in production:

- Industrial relations laws: These provide frameworks for setting minimum wage levels and working conditions across different industries, affecting labour costs.

- Production regulations: Laws regulating firm behaviour—including safety rules, environmental controls, and prohibition of child labour—mean firms cannot always choose the cheapest production method.

How to distribute production?

Many government policies affect how production is distributed throughout society:

- Progressive taxation and welfare: Higher-income earners pay proportionately more tax, and this money redistributes to lower-income earners through welfare payments. This changes the distribution that would result from pure market forces and the price mechanism alone.

- Factor market intervention: Government may intervene in factor markets for redistributive purposes, such as imposing minimum wages in the labour market.

Key Points to Remember:

-

A market economy operates through private ownership, consumer sovereignty, freedom of enterprise, and competition, with the price mechanism coordinating supply and demand through price signals.

-

No pure market economies exist today—all modern economies are mixed economies combining market forces with government intervention.

-

Australia's mixed economy balances market characteristics (private property, free enterprise, consumer sovereignty, competition) with government intervention (public ownership, regulation, social welfare, progressive taxation).

-

Governments intervene for three main reasons: ensuring efficient resource allocation (providing public goods, regulating markets), achieving fair income distribution (through social welfare and progressive taxation), and maintaining economic stability (smoothing business cycles, protecting financial systems).

-

In mixed economies, markets primarily answer the four economic questions (what, how much, how to produce, and distribution), but governments selectively modify outcomes to address market failures and achieve social objectives.