Production, Distribution, and Exchange of Goods and Services (HSC SSCE Economics): Revision Notes

Production, Distribution, and Exchange of Goods and Services

Understanding goods and services

The economy exists to produce goods and services that satisfy human wants and needs. Goods are physical, tangible items you can touch and own—such as food, vehicles, or electronic devices. Services, on the other hand, are intangible activities performed for our benefit—like medical treatment, entertainment, or education.

Production transforms resources into these goods and services through various processes. The quality and quantity of resources available to an economy significantly affects its wealth and the living standards of its population. Countries with abundant, high-quality resources can better satisfy wants and achieve higher quality of life.

The distinction between tangible and intangible is key to understanding economics. While goods can be stored, inventoried, and physically transported, services are consumed at the moment they're produced. This fundamental difference affects how these products are priced, distributed, and traded in markets.

Factors of production

Critical Concept: Factors of Production

A factor of production is any resource used in creating goods and services. Economists identify four main categories, each with a corresponding financial reward for its owners. Understanding these four factors and their rewards is fundamental to all economic analysis.

Natural resources (land)

Natural resources encompass all materials occurring naturally in the environment that can be used for production. This includes soil, water, forests, mineral deposits, fishing grounds, and land itself. The term "land" is often used as shorthand for all natural resources.

Owners of natural resources receive rent as their income. In economics, rent refers to all income earned from the productive use of natural resources—not just property rental payments. For example, income from mining rights or timber harvesting would fall under this category.

Understanding "Rent" in Economics

The economic definition of rent is broader than everyday usage. It includes:

- Traditional property rental payments

- Mining royalties from extracting minerals

- Income from timber harvesting rights

- Payments for fishing rights

- Revenue from oil and gas extraction

Any income derived from allowing others to use natural resources counts as rent in economic terms.

Scarcity consideration: Natural resources are finite. There are physical limits to available land, fossil fuels, minerals, and even clean air and water.

Labour

Labour represents all human effort—both physical and mental—applied to production. The availability of labour depends on several factors:

- Population size, influenced by birth rates, death rates, and immigration

- School leaving age and retirement age

- Social attitudes toward workforce participation

- Availability of childcare

- Educational standards

- On-the-job training opportunities

Workers receive wages as their reward. Economists use this term broadly to include:

- Regular weekly or monthly payments

- Executive salaries

- Professional fees

- Commissions

- Self-employment earnings

Wage levels vary significantly between workers based on hours worked, skill level, expertise, qualifications, and bargaining power during negotiations.

The economic concept of wages encompasses all forms of payment for labour effort. Whether you're paid hourly, receive a fixed salary, earn commission, or work for yourself, economists classify all these payments as wages because they represent rewards for your labour contribution to production.

Scarcity consideration: Labour supply is limited by population size, available skills, and willingness to work.

Capital

Capital refers to the "produced means of production"—goods created not for immediate consumption but to produce other goods and services. Capital goods include machinery, tools, factories, and computers. These assets are typically owned privately by individuals or firms.

Infrastructure (or social overhead capital) represents another form of capital, usually owned collectively. This includes roads, railways, bridges, telecommunications networks, and schools. Although businesses don't own most infrastructure, it is essential for operations—good transport networks enable goods distribution, while reliable power supplies run machinery.

Capital vs. Consumer Goods: A Critical Distinction

Capital goods are produced means of production—they're made to create other goods, not for immediate consumption. A factory machine is capital; a home computer for entertainment is a consumer good. The same physical item might be capital or a consumer good depending on its use.

Note that economists' definition of capital excludes financial assets like money, shares, stocks, and bonds. When economists say "capital," they mean physical productive assets, not financial capital.

Capital equipment dramatically increases productivity—the output generated per unit of input per unit of time. Using capital goods allows existing workers and natural resources to produce more, satisfying more wants than would otherwise be possible. The amount of available capital significantly affects an economy's future productive capacity.

Capital funding comes from savings. When consumers save rather than spend money, entrepreneurs can borrow these funds to invest in capital goods. This effectively shifts resources from consumer goods to capital goods production.

Capital owners earn interest. Entrepreneurs pay interest on borrowed funds, making interest the price of capital. For those investing their own surplus funds in capital equipment, the interest they could have earned in a bank account represents the opportunity cost of capital investment.

Scarcity consideration: Capital supplies are limited by government and private sector willingness to invest, plus the level of domestic and overseas savings available for investment.

Enterprise

Enterprise involves organizing the other three factors of production to create goods and services. This is the vital ingredient bringing the production process together. The entrepreneur makes all management decisions about production and bears the risk that decisions may be incorrect. Right decisions create successful businesses; wrong ones may lead to failure.

Profit is the return to enterprise. This isn't simply revenue minus expenses. Entrepreneurs are entitled to receive rent for any land they own used in production, wages for their work effort, and interest on capital invested in the business. Profit is income received over and above these other rewards, earned because the entrepreneur successfully establishes and runs a business despite considerable failure risk.

What Profit Really Means

Many students confuse profit with total business revenue. Economic profit is what remains after the entrepreneur has paid:

- Rent for any natural resources used

- Wages for all labour (including their own work effort)

- Interest on capital invested in the business

Only the amount left over after these payments represents true profit—the reward for taking on entrepreneurial risk and successfully organizing production.

Scarcity consideration: Entrepreneurial skills are limited by population size and various cultural and economic factors, particularly individuals' ability and willingness to innovate and take risks.

Remember the Four Factors and Their Rewards

- Natural Resources (Land) → earns Rent

- Labour → earns Wages

- Capital → earns Interest

- Enterprise → earns Profit

Memory aid: "Natural workers Labour to build Capital Enterprises" corresponds to "Rent, Wages, Interest, Profit"

All four factors face scarcity—they are limited in supply, creating the fundamental economic problem of resource allocation.

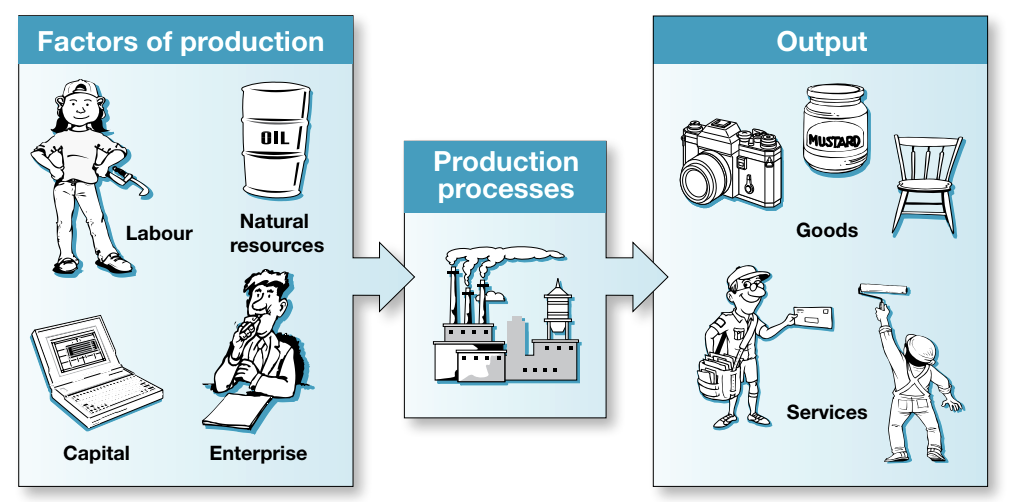

The production process

The diagram below illustrates how the four factors of production combine through production processes to create output in the form of goods and services.

All four resources face scarcity limitations, reflecting the fundamental economic problem. In market economies, resource allocation decisions are largely determined by consumer spending patterns. Firms respond to consumer demand by acquiring necessary resources to produce wanted items. Motivated by profit, firms pay for resources and labour skills needed to produce goods and services in demand.

In market economies, the price mechanism coordinates resource allocation. When consumers demand more of a product, its price rises, making it more profitable to produce. This attracts more resources to that industry. Conversely, falling demand and prices signal firms to move resources elsewhere. This process happens automatically through millions of individual buying and selling decisions.

Efficient industries facing growing consumer demand and higher prices can attract more resources. Resources that are relatively cheaper will be more attractive to profit-maximizing firms.

Production methods

Businesses can often combine resources in different ways during production. They must decide which combination to use. Depending on which factor is used in greater proportion, the production method may be:

- Labour-intensive: More labour used relative to other factors

- Capital-intensive: More capital used relative to other factors

The choice between methods depends on relative resource costs, availability, and the nature of the product being produced.

Comparing Production Methods

Consider two approaches to harvesting wheat:

Labour-intensive approach:

- Many workers harvest by hand with simple tools

- High labour costs, low capital investment

- Common in developing economies where labour is abundant and cheap

Capital-intensive approach:

- Combine harvesters operated by few workers

- High capital investment, low labour costs

- Common in developed economies where capital is relatively cheaper than labour

The same output can be achieved, but the optimal method depends on factor prices in that economy.

Distribution of goods and services

Measuring total output

The total goods and services produced in an economy during one year is called Gross Domestic Product (GDP). GDP also measures society's total income received from production. A key function of economic systems is determining how to distribute and exchange this output. This typically involves assigning individuals income levels that command a certain proportion of total output, which they can then exchange for goods and services.

How market economies distribute output

Market economies don't distribute output equally. Instead, they provide income as a reward for contributions to production. Owners of natural resources, capital, or entrepreneurial skill receive income based on their input's value. Workers are paid according to their labour's value.

The price paid for inputs determines each individual's share of total output. This generally depends on how scarce or highly demanded their resources are. City centre land rent or highly skilled managers' labour commands higher prices because these resources are in high demand with scarce supply.

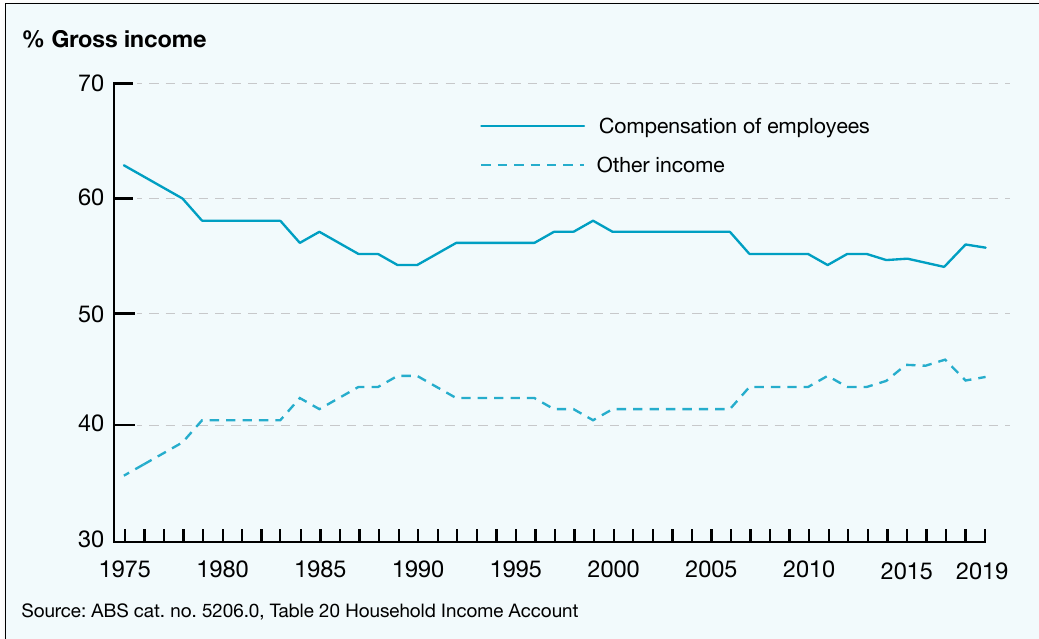

The graph above shows the proportion of total Australian household income from labour (compensation of employees) compared with other factor incomes. Over recent decades, distribution has remained relatively stable, with wage income share higher than the 1980s but lower than the 1970s.

Benefits and problems of market distribution

Benefits:

- Provides incentives for people to acquire better skills and work harder

- Encourages entrepreneurship and business creation

- Improves the resource base

- Stimulates innovation and technological advancement

Problems:

- Can be unfair to those unable to contribute due to illness, age, or disability

- Those with less bargaining power may not secure fair returns for their labour

- Creates significant income inequality

The Inequality Trade-off

Market distribution creates a fundamental tension in economics. While income inequality provides incentives for innovation and hard work, it also means some people receive very low incomes through no fault of their own. Those unable to work due to disability, age, or illness may receive no income at all in a pure market system.

This is why virtually all modern economies are mixed economies—they combine market mechanisms with government intervention to balance efficiency and equity.

Government intervention

Governments can intervene to correct inequitable market outcomes, helping those who wouldn't otherwise receive adequate income. This involves taking money from higher-income earners through taxation and redistributing it to lower-income earners through social security payments. In this way, governments influence goods and services distribution.

Exchange of goods and services

Money as medium of exchange

Individuals and businesses generally use money for exchanging goods and services. This facilitates transactions when only one party is interested in what the other offers. Money as the basis of exchange allows individuals to specialise in their production contributions. Even local services like babysitting, cleaning, and home repairs are typically paid in cash rather than through direct exchange.

Money solves the "double coincidence of wants" problem that exists in barter systems. You don't need to find someone who both has what you want AND wants what you have. Instead, money acts as a universal medium of exchange—everyone accepts it because they know others will accept it from them. This dramatically reduces transaction costs and enables economic specialisation.

Barter

The non-cash exchange of goods and services is known as barter. Bartering was common in earlier societies but is rare in advanced economies with stable currencies. However, there has been a small resurgence through bartering cooperative groups in recent years.

The Australian Tax Office treats barter transactions under the same tax assessment rules as cash or credit transactions. You may still be liable for GST or income tax on bartered goods or services. New forms of currency like Bitcoin have also created new non-cash exchange methods.

While barter seems simple, it faces significant limitations:

- Requires a double coincidence of wants (each party must want what the other offers)

- Difficult to determine fair exchange rates between different goods

- No way to store value for future use

- Cannot easily divide high-value items for small transactions

These limitations explain why money-based exchange dominates modern economies.

Exam tips

Exam Success Strategies

When answering questions on this topic:

- Define key terms clearly: Always define factors of production and their rewards precisely

- Use examples: Support explanations with relevant examples of each factor

- Link scarcity to factors: Explain how limited resources create economic problems

- Evaluate distribution: Consider both benefits (incentives) and problems (inequality) of market distribution

- Explain government role: Show understanding of how intervention addresses market failures

Remember to show both sides of economic issues—for instance, discuss both advantages and disadvantages of market-based income distribution.

Remember!

Key Points to Remember:

Core Concepts:

- Goods are tangible products; services are intangible actions

- Four factors of production: natural resources, labour, capital, and enterprise

- Each factor receives a corresponding reward: rent, wages, interest, and profit

- All factors are scarce, creating resource allocation challenges

- Market economies distribute income based on contribution to production, not equally

- Money serves as the primary medium of exchange, though barter still exists

Essential Terms:

- Factors of production: Resources used to produce goods and services

- GDP: Total goods and services produced in an economy in one year

- Capital: Produced means of production (not for immediate consumption)

- Infrastructure: Community-owned capital like roads and schools

- Productivity: Output produced per unit of input per unit of time

- Barter: Non-cash exchange of goods and services

Critical Framework—The Production-Distribution-Exchange Cycle:

- Resources (factors) are combined

- Goods and services are produced

- Output is distributed via income rewards

- Goods and services are exchanged using money (or barter)