Analysing and Modelling Reducing Balance Loans and Annuities (VCE SSCE General Mathematics): Revision Notes

Analysing and Modelling Reducing Balance Loans and Annuities

Introduction

When you borrow money or invest in certain financial products, you need mathematical tools to track how the balance changes over time. This note explains how to use recurrence relations to model and analyse two important financial situations: reducing balance loans and annuities.

Understanding these mathematical models is essential for making informed financial decisions. Whether you're taking out a loan or planning for retirement with an annuity, these tools help you predict future balances and plan your finances effectively.

Reducing balance loans

What is a reducing balance loan?

A reducing balance loan is a type of loan where you make regular payments to reduce the amount you owe, rather than waiting until the end of the loan term to repay everything at once. Most bank loans work this way, such as car loans, personal loans, and mortgages.

With each payment you make:

- Part of the payment covers the interest charged

- The rest reduces the principal (the amount you borrowed)

- The balance decreases over time

Modelling reducing balance loans with recurrence relations

We can model reducing balance loans using a mathematical tool called a recurrence relation. This gives us a formula that shows how the loan balance changes after each payment.

The recurrence relation formula:

What each variable represents:

- = the balance of the loan after payments have been made

- = the principal (the initial amount borrowed)

- = the balance after the next payment

- = the regular payment amount

- = the growth multiplier

The growth multiplier formula:

Where:

- = the annual interest rate (as a percentage)

- = the number of compounding periods per year

Understanding the compounding periods:

- For annual compounding:

- For monthly compounding:

- For quarterly compounding:

- For daily compounding:

The more frequently interest compounds, the larger becomes, making closer to 1.

Worked example: Constructing a recurrence relation (annual compounding)

Worked Example: Flora's Loan (Annual Compounding)

Problem: Flora borrows $8000 at an interest rate of 13% per annum, compounding annually. She makes yearly payments of $2100. Construct a recurrence relation to model this loan.

Solution:

Step 1: Identify the principal and payment amount

- (the amount borrowed)

- (the yearly payment)

Step 2: Calculate the growth multiplier

Using the formula where and (annual compounding):

Step 3: Write the recurrence relation

This formula tells us that each year, the balance is multiplied by 1.13 (adding 13% interest), then $2100 is subtracted (the payment).

Worked example: Constructing a recurrence relation (monthly compounding)

Worked Example: Alyssa's Loan (Monthly Compounding)

Problem: Alyssa borrows $1000 at an interest rate of 15% per annum, compounding monthly. She makes monthly payments of $250. Construct a recurrence relation to model this loan.

Solution:

Step 1: Identify the principal and payment amount

Step 2: Calculate the growth multiplier

Using the formula where and (monthly compounding):

Step 3: Write the recurrence relation

When interest compounds monthly, the growth multiplier is much closer to 1 than with annual compounding, because the interest rate is divided across 12 periods. This is a crucial difference when calculating !

Using a recurrence relation to analyse a reducing balance loan

Once you have established a recurrence relation, you can use it to find the loan balance after any number of payments. A calculator is very helpful for this.

Worked example: Finding loan balance after payments

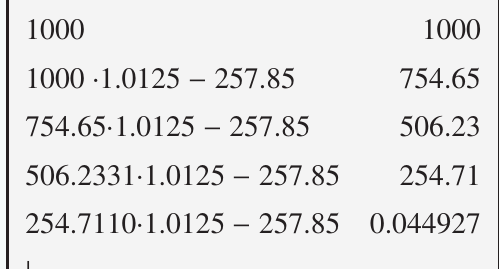

Worked Example: Analysing Alyssa's Loan Balance

Problem: Alyssa's loan can be modelled by the recurrence relation:

a) Use your calculator to find the balance of the loan after four payments.

b) Find the balance of the loan after two payments have been made. Round your answer to the nearest cent.

Solution:

Part a: Finding the balance after four payments

Step 1: Enter the initial value

- Type

1000and press ENTER or EXE

Step 2: Set up the iteration

- Type

× 1.0125 - 257.85and press ENTER (or EXE)

Step 3: Continue pressing ENTER four times

Each press calculates the next value in the sequence:

Answer: The balance after four payments is $0.04 (to the nearest cent).

This shows that four payments are almost enough to pay off the loan completely!

Part b: Finding the balance after two payments

Look at the third line of the calculator output (remember: the first line shows , the second shows , and the third shows ).

Answer: $506.23 (to the nearest cent)

Exam tip: When using your calculator for iterations:

- The first value you see is

- After one ENTER press, you see

- After two ENTER presses, you see

- And so on...

Common mistake: Students often count the initial value as instead of . Always remember that the starting value is !

Annuities

What is an annuity?

An annuity is a type of investment where:

- You invest a lump sum of money

- The investment earns compound interest

- You receive regular payments (withdrawals) from the investment

The value of the annuity represents how much money remains in the investment after accounting for the interest earned and payments withdrawn.

Key difference from loans: With a loan, you owe money and make payments to reduce your debt. With an annuity, you have invested money and receive payments while the investment continues to earn interest.

Despite this difference, the mathematics for modelling annuities is identical to that for reducing balance loans!

Modelling annuities with recurrence relations

The recurrence relation formula for annuities:

What each variable represents:

- = the value of the annuity after payments have been received

- = the principal (the initial investment amount)

- = the value after the next payment

- = the regular payment received

- = the growth multiplier (calculated the same way as for loans)

Worked example: Modelling an annuity

Worked Example: Reza's Annuity Investment

Problem: Reza invests $12,000 in an annuity that earns interest at the rate of 6% per annum, compounding monthly, providing him with a monthly income of $2035.

a) Model this annuity using a recurrence relation.

b) Use your calculator to find the value of the annuity after the first four months. Round your answer to the nearest cent.

Solution:

Part a: Constructing the recurrence relation

Step 1: Identify the principal and payment amount

- (the initial investment)

- (the monthly payment received)

Step 2: Calculate the growth multiplier

Using the formula where and :

Step 3: Write the recurrence relation

Part b: Finding the value after four months

Step 1: Enter the initial value

- Type

12000and press ENTER or EXE

Step 2: Set up and perform the iteration

- Type

× 1.005 - 2035and press ENTER (or EXE) four times

Calculator output:

| Iteration | Calculation | Value |

|---|---|---|

| 12000 | 12000.00 | |

| 10025.00 | ||

| 8040.13 | ||

| 6045.33 | ||

| 4040.55 |

Answer: The value of the annuity after four months is $4040.55 (to the nearest cent).

Interpretation: Even though Reza has withdrawn $8140 (4 × $2035) over four months, he still has $4040.55 remaining in his annuity because his investment has been earning interest.

Key similarities between loans and annuities

Both reducing balance loans and annuities:

- Use the same recurrence relation formula:

- Involve compound interest

- Have regular payments

- Can be analysed using the same calculator techniques

The main difference is:

- Loans: You owe money and make payments to reduce your debt

- Annuities: You have invested money and receive payments while earning interest

The mathematical model is identical, but the financial context is opposite!

Remember!

Key Points to Remember:

-

Reducing balance loans involve making regular payments to pay off money you have borrowed. The loan balance decreases over time.

-

Annuities involve receiving regular payments from an investment that earns compound interest. The investment value decreases over time.

-

The recurrence relation for both is: , , where is the balance/value after payments, is the payment amount, and is the growth multiplier.

-

The growth multiplier is calculated as: , where is the annual interest rate and is the number of compounding periods per year.

-

Use your calculator to iterate through the recurrence relation to find the balance or value after any number of payments. Remember that the first value shown is , and each subsequent press gives you the next term in the sequence.

-

Memory aids:

- "V for Value" - represents the value/balance after payments

- "R for Rate growth" - is always greater than 1 for positive interest

- "D for Deduction" - is what gets subtracted (payment or withdrawal)

- "Next = Rate × Current - Payment" summarizes the formula