Using a Finance Solver to Find Interest Rates, Time Taken, and Regular Payments (VCE SSCE General Mathematics): Revision Notes

Using a Finance Solver to Find Interest Rates, Time Taken, and Regular Payments

Introduction to finance solver calculations

A finance solver is a powerful tool that allows us to calculate unknown variables in financial problems involving loans, investments, and annuities. Instead of just finding the future value, we can also determine:

- The interest rate needed to reach a financial goal

- The time required for an investment to grow to a target amount

- The regular payment amount needed for a loan or investment

This note will guide you through using a finance solver for three key financial situations: investments with additional payments, reducing balance loans, and annuities.

The finance solver uses the Time Value of Money (TVM) principle, which recognizes that money available today is worth more than the same amount in the future due to its potential earning capacity. This makes it an essential tool for making informed financial decisions.

Understanding sign conventions

When using a finance solver, it is crucial to understand that money flows have specific signs (positive or negative) depending on the direction of the transaction. Think of it from your perspective: money you give away is negative, and money you receive is positive.

Sign conventions for investments with additional payments

When you invest money with regular additional payments:

- PV (Present Value): Negative - you give the bank your initial investment

- PMT (Payment): Negative - you make regular deposits into the account

- FV (Future Value): Positive - the bank returns your money with interest when the investment matures

Sign conventions for reducing balance loans

When you take out a loan:

- PV (Present Value): Positive - the bank gives you money through the loan

- PMT (Payment): Negative - you make regular repayments to the bank

- FV (Future Value): Usually zero or negative - this represents the balance remaining after your payments

Sign conventions for annuities

When you purchase an annuity:

- PV (Present Value): Negative - you give the bank money to buy the annuity

- PMT (Payment): Positive - you receive regular payments from the bank

- FV (Future Value): Zero or positive - this represents the remaining balance after payments

Master the Sign Convention Rule:

The key principle is simple: money flowing OUT of your pocket is negative, money flowing INTO your pocket is positive. This applies consistently across all financial calculations:

- Investments: You give money (PV negative, PMT negative), you receive the matured amount (FV positive)

- Loans: Bank gives you money (PV positive), you repay (PMT negative)

- Annuities: You give money upfront (PV negative), you receive regular payments (PMT positive)

Getting the signs wrong is one of the most common mistakes that leads to incorrect answers!

Finding values for investments with additional payments

When working with investments that involve both an initial deposit and regular additional payments, the finance solver can determine any unknown variable if all others are provided.

Finding the required interest rate

Let's explore how to determine what interest rate is needed to achieve a specific investment goal.

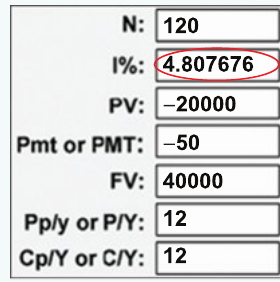

Worked Example: Finding the Interest Rate for an Investment

Mingjia invests $20,000 into a compound interest account where interest compounds monthly. She adds $50 per month to her investment. She wants her investment to reach $40,000 in 10 years. What annual interest rate does she need?

Solution:

Step 1: Set up the finance solver with the known values:

- (10 years with monthly compounding means periods)

- (initial investment, negative because Mingjia gives this money to the bank)

- (monthly additions, negative because she gives this money)

- (target amount, positive because she will receive this)

- (monthly payments means 12 payments per year)

- (interest compounds monthly, so 12 times per year)

Step 2: Solve for using the finance solver.

Step 3: Read the result and round appropriately.

The calculator shows

Rounded to two decimal places: Mingjia requires an interest rate of 4.81% per annum.

Finding the regular payment amount

Sometimes we know the interest rate and time period, but need to determine how much to deposit regularly.

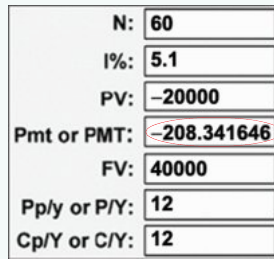

Worked Example: Finding the Minimum Monthly Payment

Winston puts $20,000 into an investment account paying 5.1% interest per annum, compounding monthly. If Winston wants his investment to be worth at least $40,000 in 5 years, what is the minimum he needs to add each month?

Solution:

Step 1: Enter the known values into the finance solver:

- (5 years with monthly payments: )

- (annual interest rate)

- (initial investment)

- (target amount)

- (monthly payments)

- (monthly compounding)

Step 2: Solve for .

Step 3: Interpret and adjust the result.

The calculator shows

However, we need to check this carefully. If Winston pays $208.34 per month, the final value will be $39,999.89, which is less than $40,000.

Therefore, Winston must add $208.35 each month to ensure his investment reaches at least $40,000.

Critical Rounding Consideration:

Always verify your rounded answer, especially when dealing with minimum or maximum values. The general rule is:

- Round UP if you need to meet or exceed a target (minimum payment, minimum future value)

- Round DOWN if you need to stay below a limit (maximum payment, maximum time)

Failing to verify can result in missing your financial target by a small but significant amount!

Finding the time required

We can also determine how long it will take for an investment to reach a specific value.

Worked Example: Finding the Time for an Investment to Triple

Using the same scenario as above, if Winston invests $1,000 each month immediately after interest is calculated, what is the minimum number of months required for his investment to at least triple in value (reach $60,000)?

Solution:

Step 1: Adjust the finance solver values:

- (changed from previous example)

- (triple the initial $20,000)

- Keep other values the same: , , ,

Step 2: Solve for .

The calculator shows

Step 3: Round appropriately.

After 34 months, the future value is approximately $59,598.15, which is less than $60,000.

Therefore, the investment will take 35 months to triple in value.

When finding time periods, always check whether to round up or down. If you need to reach a minimum target, round up to ensure the goal is met. The fractional part of means the target will be reached partway through that period, so you need to complete the full period.

Finding values for reducing balance loans

A reducing balance loan is one where the principal gradually decreases as regular payments are made, with interest calculated on the outstanding balance. This is the most common type of loan for personal loans, car loans, and mortgages.

Finding the regular loan payment

For a reducing balance loan, we often need to calculate the regular payment amount required to fully repay the loan over a specified period.

Worked Example: Determining Loan Payments and Total Interest

Sipho borrows $10,000 to be repaid in 59 equal monthly payments followed by a 60th payment slightly larger than the regular payment. Interest is charged at 8% per annum, compounding monthly.

Part a: Find the regular monthly payment amount

Solution:

Step 1: Enter the loan details into the finance solver:

- (assuming 60 equal payments initially)

- (annual interest rate)

- (loan amount, positive because Sipho receives this money)

- (the loan will be fully repaid)

- (monthly payments)

- (interest compounds monthly)

Step 2: Solve for .

The calculator displays

Step 3: Round to the nearest cent.

The regular monthly payment is $202.76.

Note that the negative sign indicates money Sipho pays back to the lender.

Calculating the final payment and total interest

When working with loans, the final payment is often slightly different from the regular payment due to rounding. Let's see how to calculate this and determine the total cost of the loan.

Worked Example Continued: Final Payment and Total Interest

Part b: Find the final payment

When we make 59 payments of $202.76, there will be a small remaining balance.

Solution:

Step 1: Calculate the future value after 60 payments of $202.76.

Enter (the rounded value) and solve for after 60 periods.

The calculator shows (approximately -$0.29)

Step 2: Calculate the final payment.

The final payment is $203.05.

Part c: Find the total of the repayments

Solution:

The total repayment is $12,165.89.

Part d: Find the total amount of interest paid

Solution:

The total interest paid is $2,165.89.

This means Sipho pays more than 20% of the original loan amount in interest over the 5-year period.

The formula for calculating the final payment when you have a remaining balance is:

Final payment = Regular payment + Remaining balance

The remaining balance is found by calculating using the rounded regular payment amount. This accounts for the small discrepancies introduced by rounding.

Finding values for annuities

An annuity is a financial product where you invest a lump sum and receive regular payments over time. The finance solver can help determine various aspects of annuity arrangements. Think of it as the opposite of a loan: you give the bank money upfront, and they pay you back in installments.

Finding the required interest rate for an annuity

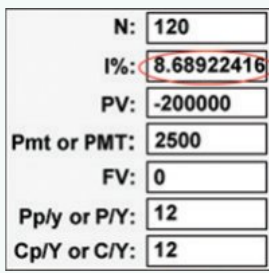

Worked Example: Interest Rate Needed for Desired Annuity Payments

Joe invests $200,000 into an annuity with interest compounding monthly. What interest rate would allow Joe to withdraw $2,500 each month for 10 years?

Solution:

Step 1: Set up the finance solver:

- (10 years with monthly payments: )

- (Joe gives this money to buy the annuity)

- (Joe receives this amount monthly, so it's positive)

- (the annuity is fully exhausted after 10 years)

- (monthly payments)

- (interest compounds monthly)

Step 2: Solve for .

The calculator shows

Joe would require an interest rate of 8.7% per annum (rounded to one decimal place).

Finding the duration of annuity payments

Worked Example: How Long Will Annuity Payments Last?

If the interest rate is 5% per annum and Joe receives regular monthly payments of $3,000, for how many months will Joe receive a regular payment?

Solution:

Step 1: Adjust the finance solver values:

- Keep , , ,

Step 2: Solve for .

The calculator shows

Step 3: Round down to count complete regular payments.

Joe will receive a regular payment for 78 months.

We round down because after 78 complete months, there will be a final smaller payment in month 79.

When calculating the duration of annuity payments, always round down to find the number of complete regular payments. The fractional part indicates that the last payment will be smaller than the regular payment amount.

This is the opposite of rounding for investments where you typically round up!

Finding the regular annuity payment amount

Worked Example: Calculating Monthly Annuity Income

If the interest rate is 5% per annum and Joe wishes to receive monthly payments for 10 years, how much will he receive each month?

Solution:

Step 1: Enter the values into the finance solver:

- (10 years)

- (annual interest rate)

- (initial investment)

- (annuity exhausted after 10 years)

- (monthly payments)

- (interest compounds monthly)

Step 2: Solve for .

The calculator displays

Joe will receive $2,121.31 each month from the annuity.

The positive sign indicates this is money Joe receives.

Calculating the final annuity payment

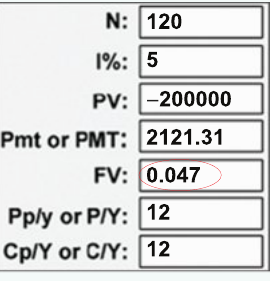

Worked Example: Finding the Final Payment Amount

If Joe receives the regular monthly payment of $2,121.31 for 119 months, what will his final payment be?

Solution:

Step 1: Find the future value after 119 payments.

Enter:

- (the calculated regular payment)

Solve for , which gives

Step 2: Calculate the final payment.

The final payment is $2,121.36 (rounded to the nearest cent).

Key Points to Remember:

-

Sign conventions are critical: Money you give is negative, money you receive is positive

- Investments: and are negative, is positive

- Loans: is positive, is negative, is usually zero

- Annuities: is negative, is positive, is usually zero

-

Always verify your rounding: When finding minimum payments or time periods, check that your rounded answer actually meets the required goal

- Round up for minimum payments needed

- Round up for minimum time periods to reach a target

- Round down for the number of complete regular payments in an annuity

-

The five key finance solver variables are:

- (number of periods)

- (annual interest rate as a percentage)

- (present value or initial amount)

- (regular payment amount)

- (future value or final amount)

-

Final payments often differ: The last payment is usually slightly different from the regular payment amount due to rounding. Calculate this by finding after the regular payments and adjusting accordingly using: Final payment = Regular payment + Remaining balance

-

Total interest for loans: Total interest paid = Total repayments - Principal borrowed. This reveals the true cost of borrowing money over time.

-

Set and correctly: is the number of payments per year, and is the number of compounding periods per year. For monthly compounding and monthly payments, both equal 12.