Using a Finance Solver to Find the Balance and Final Payment (VCE SSCE General Mathematics): Revision Notes

Using a Finance Solver to Find the Balance and Final Payment

What is a finance solver?

A Finance Solver is a built-in calculator function that makes financial calculations much easier and faster. While you can work out loan repayments, investment values and annuity balances manually, this becomes very time-consuming when dealing with long time periods. For example, a typical home loan might involve monthly payments over 30 years - that's 360 separate calculations! The Finance Solver can handle these complex scenarios in seconds.

Your CAS calculator has this powerful tool ready to use whenever you need to solve problems involving:

- Loans that are repaid over time

- Investments that grow with regular deposits

- Annuities that pay out regular amounts

Accessing the finance solver

On the TI-Nspire CAS

To open the Finance Solver on your TI-Nspire CAS calculator:

- Press ctrl + N to create a new document

- Select "Add Calculator"

- Press the menu button, then navigate to Finance > Finance Solver

On the Casio ClassPad

To open the Finance Solver on your Casio ClassPad:

- Tap "Financial" from the main menu screen

- Select "Compound Interest" from the solver screen

Understanding the finance solver variables

When you open the Finance Solver, you'll see several entry fields. Each one represents a different aspect of your financial calculation. Here's what each variable means:

N (Number of payments)

This is the total number of payments you'll make or receive over the entire period. For monthly payments over 5 years, N would be (because ).

I% (Interest rate)

This is the annual interest rate expressed as a percentage. If you're earning 6% per annum, you'd enter (not ).

Notice that you enter the interest rate as a percentage (6 for 6%), not as a decimal (0.06). The calculator automatically handles the conversion.

PV (Present value)

This is the starting amount - either the initial loan amount or the initial investment. It represents the value at the beginning, right now.

Pmt or PMT (Payment)

This is the amount you pay or receive each period. It's usually the same amount each time (unless there's a final payment that differs).

FV (Future value)

This is the value at the end of all the payments. For a loan that's fully repaired, FV would be zero. For an investment, FV shows how much you'll have accumulated.

PpY or P/Y (Payments per year)

This tells the calculator how often payments are made. Use for monthly payments, for quarterly, for half-yearly, or for annual payments.

CpY or C/Y (Compounding periods per year)

This indicates how often interest is calculated and added. In most problems, this equals PpY. Use for monthly compounding, for quarterly, and so on.

PmtAt (Payment timing)

This setting determines whether interest compounds at the end or beginning of each period. For SSCE problems, ensure this is always set to END.

The sign convention: positive and negative values

Understanding Sign Convention is Critical

The Finance Solver needs to understand which direction money is flowing. It does this using a sign convention:

- Positive (+): Money you receive or money someone owes you

- Negative (−): Money you pay out or money you owe someone

Think of it from your perspective:

- When you deposit money into an account, you're giving it away (for now) → negative

- When the bank gives you a loan, you're receiving money → positive

- When you make loan repayments, you're paying out money → negative

- When an investment pays you back, you're receiving money → positive

Getting the signs right is crucial! The calculator won't give you the correct answer if you mix up positive and negative values.

Compound interest investments with regular additions

A compound interest investment with regular additions is when you:

- Invest an initial lump sum (the present value)

- Make regular additional deposits (the payment)

- Earn interest that compounds over time

Your investment grows both from the interest earned and from your additional deposits.

Sign conventions for investments

When using Finance Solver for this type of investment:

- PV: Negative - You give the initial investment to the bank

- PMT: Negative - You give regular deposits to the bank

- FV: Positive - The bank will give you the final amount when the investment matures

For investments, think of it as "giving money now to get more money later". Both PV and PMT are negative because you're giving money away. The FV is positive because you'll receive the accumulated amount.

Worked example: finding the future value of an investment

Worked Example: Lars' Investment

Question: Lars invests $500,000 at 5.5% per annum, compounding monthly. He makes regular monthly deposits of $500 into the account. What is the value of his investment after 5 years? Round your answer to the nearest cent.

Solution:

Step 1: Identify the known values

- Initial investment: $500,000 (PV)

- Interest rate: 5.5% per annum (I%)

- Regular deposits: $500 per month (PMT)

- Time period: 5 years, which is months (N)

- Compounding: Monthly (both PpY and CpY are 12)

Step 2: Enter values into Finance Solver

Step 3: Solve for FV

Move the cursor to the FV field and press enter (or tap Solve on ClassPad).

The calculator returns:

Step 4: Interpret and write the answer

The FV is positive, which means the bank will give this amount to Lars. Rounding to the nearest cent:

After 5 years, Lars' investment will be worth $692,292.30

Reducing balance loans

A reducing balance loan is when you:

- Borrow money from a bank (the present value)

- Make regular repayments (the payment)

- Pay interest on the remaining balance

As you make repayments, the amount you owe (the balance) decreases over time.

Sign conventions for loans

When using Finance Solver for a reducing balance loan:

- PV: Positive - The bank gives you money through the loan

- PMT: Negative - You repay the loan by making regular payments to the bank

- FV: Can be negative, zero, or positive depending on the situation:

- Negative FV: You still owe the bank money

- Zero FV: The loan is completely repaid

- Positive FV: You've overpaid and the bank owes you money

For loans, think of it as "receiving money now to pay it back later". PV is positive because you receive the loan. PMT is negative because you're making repayments to the bank.

Worked example: finding loan balance and final payment

Worked Example: Andrew's Loan

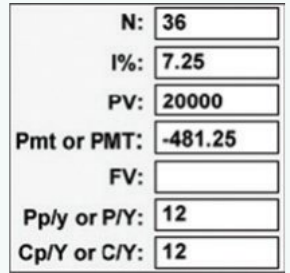

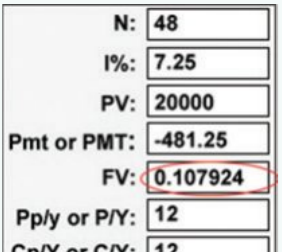

Question: Andrew borrows $20,000 at an interest rate of 7.25% per annum, compounding monthly. This loan will be repaid over 4 years with regular payments of $481.25 each month for 47 months, followed by a final payment to fully repay the loan.

a) How much does Andrew owe after 3 years? Round your answer to the nearest cent.

b) What is the final payment amount that Andrew must make to fully repay the loan within 4 years (48 months)? Round your answer to the nearest cent.

Solution to part a:

Step 1: Identify the known values for the first 3 years

- Loan amount: $20,000 (PV)

- Interest rate: 7.25% per annum (I%)

- Regular payments: $481.25 per month (PMT)

- Time period: 3 years = months (N)

- Compounding: Monthly (both PpY and CpY are 12)

Step 2: Enter values into Finance Solver

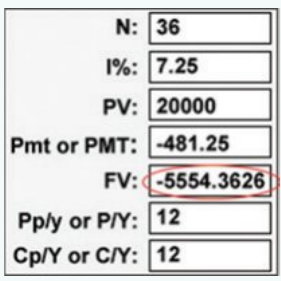

Step 3: Solve for FV

Move the cursor to the FV field and press enter (or tap Solve).

The calculator returns:

Step 4: Interpret and write the answer

The FV is negative, which means Andrew still owes this amount to the bank after 3 years (36 payments).

Andrew owes $5,554.36 after 3 years

Solution to part b:

Step 1: Enter values for the full 4 years

Step 2: Solve for FV

The calculator returns:

This is approximately $0.11 (11 cents)

Step 3: Interpret the result

The FV is positive (11 cents), which means after 47 regular payments of $481.25, Andrew will have slightly overpaid. The bank owes Andrew 11 cents.

To find the final payment, we need to reduce the regular payment by this 11 cents:

Andrew's final payment will be $481.14

Annuities

An annuity is when you:

- Invest a lump sum with a financial institution (the present value)

- Receive regular payments from that institution (the payment)

- Eventually, the annuity is fully paid out

Think of it as the opposite of a loan - you give the bank money upfront, and they pay you back in instalments with interest.

Sign conventions for annuities

When using Finance Solver for an annuity:

- PV: Negative - You buy the annuity by giving money to the bank

- PMT: Positive - You receive regular payments from the bank

- FV: Positive or zero:

- Positive FV: The bank still owes you money

- Zero FV: The annuity is completely paid out

Important: An annuity should never have a negative FV because a bank would never overpay you.

For annuities, think of it as "giving money now to receive regular payments later". PV is negative because you purchase the annuity. PMT is positive because you receive regular income from it.

Worked example: finding annuity balance and final payment

Worked Example: Charlie's Annuity

Question: Charlie invests $300,000 into an annuity paying 5% interest per annum, compounding monthly. Over the next ten years, Charlie receives a payment of $3,182 per month from the annuity for each month except the final month.

a) Find the value of the annuity after five years. Round your answer to the nearest cent.

b) Find the final payment from the annuity. Round your answer to the nearest cent.

Solution to part a:

Step 1: Identify the known values for the first 5 years

- Initial investment: $300,000 (PV)

- Interest rate: 5% per annum (I%)

- Regular payments received: $3,182 per month (PMT)

- Time period: 5 years = months (N)

- Compounding: Monthly (both PpY and CpY are 12)

Step 2: Enter values into Finance Solver

Step 3: Solve for FV

The calculator returns:

Step 4: Interpret and write the answer

The FV is positive, which means the bank still owes Charlie this amount after 5 years.

The balance of the annuity after 5 years is $168,612.25

Solution to part b:

Step 1: Enter values for the full 10 years

Step 2: Solve for FV

The calculator returns:

This is approximately $5.36

Step 3: Interpret the result

The FV is negative ($5.36), which means Charlie owes the annuity $5.36. This happens because the regular payments of $3,182 are slightly too large.

To find the final payment, we reduce the regular payment by $5.36:

Charlie's final payment will be $3,176.64

Remember!

Key Points to Remember:

-

Finance Solver saves time: Use it for calculations involving many periods, such as 30-year home loans or long-term investments.

-

Get the signs right: Money you receive or are owed is positive (+). Money you pay out or owe is negative (−). This is the sign convention that makes Finance Solver work correctly.

-

Different scenarios need different signs:

- For investments with deposits: PV and PMT are negative, FV is positive

- For reducing balance loans: PV is positive, PMT is negative, FV can be negative (still owe money), zero (fully repaid), or positive (overpaid)

- For annuities: PV is negative, PMT is positive, FV is positive or zero

-

Interpreting FV tells you the outcome: A negative FV means money is still owed, zero means fully paid/received, and positive means money is owed to you.

-

Final payments adjust for small differences: When FV is close to zero (a few cents), calculate the final payment by adjusting the regular payment amount.