Taxation and Government Expenditure (Edexcel A-Level Business): Revision Notes

Taxation and Government Expenditure

Understanding fiscal policy

Governments use fiscal policy to influence business decisions and overall economic activity. This policy tool involves adjusting taxation levels and government spending to manage the economy. Fiscal policy is a key macroeconomic instrument that can either stimulate growth during downturns or cool down an overheating economy.

Fiscal policy operates through two main levers: taxation (which affects how much money businesses and consumers have to spend) and government spending (which directly injects money into the economy or withdraws it).

When the government changes taxes or spending, it directly affects businesses and consumers. These changes ripple through the economy, influencing demand, costs, investment decisions, and overall business performance.

Taxation in the UK

The UK tax system consists of various taxes paid by both businesses and individuals. These taxes can be classified into two main categories: direct taxes and indirect taxes.

Direct taxes (taxes on income)

Direct taxes are charged on income and profits. The main direct taxes include:

Income tax is paid on personal income from employment and self-employment. Changes in income tax rates or personal allowances directly affect how much disposable income consumers have available to spend on goods and services.

National Insurance contributions are paid by both businesses and individuals based on employee earnings. Employers pay National Insurance on their employees' wages, which increases their labour costs.

Corporation tax is paid by companies on their profits. This tax directly reduces business profits and can influence investment decisions and dividend payments to shareholders.

Capital gains tax is charged on the profit made when selling assets such as property or shares. This tax can affect investment behaviour and shareholder decisions.

Inheritance tax is paid when money or assets are transferred to another individual, typically after death. Changes in inheritance tax can affect consumer spending patterns, particularly among older, wealthier demographics.

Direct taxes reduce the income available to consumers and businesses before they make spending decisions. This makes them particularly powerful tools for influencing economic behaviour, as they affect spending power at the source.

Indirect taxes (taxes on spending)

Indirect taxes are charged on spending and consumption. The main indirect taxes include:

Value Added Tax (VAT) is paid on most goods and services, with some exceptions like basic food items. VAT increases the final price paid by consumers and adds to business costs when they purchase supplies.

Excise duties are charged on specific goods including petrol, alcohol, and tobacco products. These taxes are often used to discourage consumption of particular products while raising government revenue.

Customs duties are paid when importing certain goods from abroad. These taxes can make imported products more expensive compared to domestic alternatives.

Council tax is paid by residents to local councils to fund local services. Changes in council tax affect household disposable income and therefore consumer spending power.

Business rates are paid by businesses to local councils based on property values. These represent a fixed cost for businesses that must be paid regardless of trading conditions.

Unlike direct taxes, indirect taxes are charged at the point of purchase. This means consumers can potentially avoid them by choosing not to buy certain products, giving them more flexibility in managing their spending.

How taxation changes affect businesses

Changes in taxation can affect businesses in multiple ways. Understanding these impacts helps businesses plan for policy changes and adjust their strategies accordingly.

Impact on consumer spending

Reductions in income tax, increases in personal tax allowances, or cuts to inheritance tax rates leave consumers with more disposable income. This increased purchasing power typically leads to higher consumer spending, which benefits businesses selling goods and services. Conversely, increases in income tax, National Insurance contributions, or council tax reduce disposable income and can lead to lower consumer demand.

Businesses selling luxury items or non-essential goods are particularly sensitive to changes in consumer disposable income. When taxes rise and spending power falls, consumers typically cut back on discretionary purchases first.

Effects on prices

Increases in VAT or excise duties raise business costs. Most businesses respond by passing these costs onto customers through higher prices. However, this strategy carries risks – higher prices may reduce sales volume, particularly in competitive markets where consumers can switch to cheaper alternatives.

Customs duty increases make imported goods more expensive. This affects both businesses that rely on imported supplies and consumers purchasing imported products.

Business costs, revenue and profits

Tax increases can significantly impact business profitability. VAT increases raise costs across the supply chain. Businesses may attempt to maintain profit margins by raising prices, but this can reduce sales volume if demand is price elastic.

Price elasticity of demand determines how much sales volume falls when prices rise. In highly competitive markets with many substitutes, demand tends to be more elastic, making it difficult for businesses to pass tax increases onto customers without losing significant sales.

Corporation tax increases directly reduce after-tax profits. Higher business rates represent increased fixed costs that must be paid regardless of business performance. Employers' National Insurance contribution increases raise the cost of employing workers, making labour more expensive.

Tax reductions have the opposite effect, potentially increasing business profitability. Lower corporation tax rates leave businesses with more retained profit for reinvestment or dividend payments.

Business spending and investment

Higher taxes reduce retained profits, affecting a business's ability to meet its financial obligations and invest in growth. Reduced retained profit can limit a business's capacity to pay suppliers, purchase stock, invest in new equipment, or expand facilities.

Investment decisions are particularly sensitive to taxation changes. If businesses face higher taxes and lower profits, they may delay or cancel investment projects. This can affect long-term productivity and competitiveness.

Impact on shareholding

Changes in capital gains tax and stamp duty affect investor behaviour. An increase in capital gains tax may discourage investors from selling shares or delay sales to avoid higher tax bills. This can reduce market liquidity and affect share prices.

These tax changes can influence how attractive equity investment appears compared to other asset classes.

Importing and exporting considerations

Customs duty increases can create both winners and losers. UK businesses competing against imported products may benefit if higher customs duties make imports more expensive, improving their competitive position.

However, UK businesses that rely on imported raw materials or components face higher input costs when customs duties rise. This reduces their competitiveness and profit margins unless they can pass costs onto customers.

Worked Example: Impact of Customs Duty Increase

A UK furniture manufacturer competes with imported furniture from Europe. When customs duties increase by 10%:

Winners: The UK manufacturer gains competitive advantage as imported furniture becomes more expensive, potentially increasing their market share.

Losers: A UK car manufacturer importing steel from Europe faces 10% higher input costs, reducing profit margins unless they can increase car prices to compensate.

Effects on business operations and employees

Increases in employers' National Insurance contributions make hiring additional workers more expensive. This may deter businesses from recruiting, potentially slowing employment growth or encouraging substitution of labour with capital equipment.

Changes in company car taxation or mileage allowance rates affect how businesses structure employee benefits packages. Higher taxes on these benefits may lead businesses to restructure compensation packages or reduce such benefits.

Sector-specific effects

Certain taxes target specific business activities or sectors. Landfill tax increases encourage businesses to recycle waste rather than disposing of it in landfills. Passenger duty changes affect airlines and tourism businesses by influencing travel costs and demand for holidays.

These targeted taxes can significantly affect business models and operational decisions in affected industries.

Tax avoidance and evasion

When taxes increase, some businesses attempt to minimise their tax liability through avoidance (legal) or evasion (illegal) strategies. Tax avoidance might involve restructuring operations, such as not hiring workers to avoid higher National Insurance payments, or switching from imported to domestic supplies to avoid customs duties.

Tax evasion involves illegal activities such as underreporting income or, in extreme cases, dumping waste illegally to avoid landfill taxes. Evasion carries serious legal penalties including fines and potential imprisonment.

Always remember: tax avoidance is legal (though often ethically questionable), while tax evasion is illegal and prosecutable.

Government expenditure

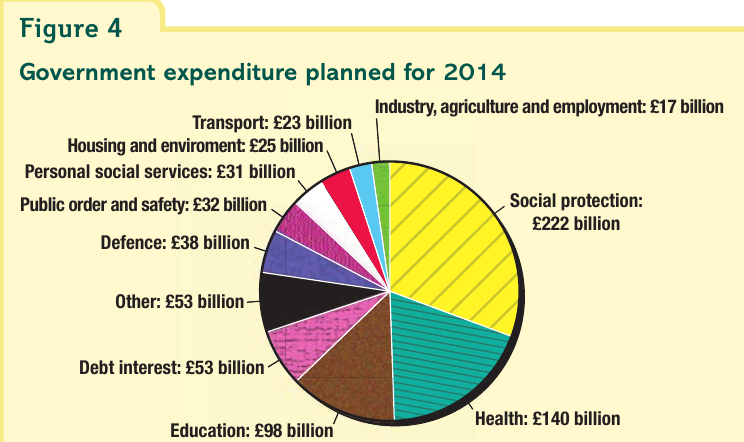

The government manages spending across the public sector, providing essential services including education, healthcare, defence, welfare benefits, and transport infrastructure. In 2014, the UK government spent £732 billion across these various services.

The largest category of government spending is social protection (including welfare benefits and pensions) at £222 billion, followed by health at £140 billion and education at £98 billion. Other significant spending areas include defence, transport, and debt interest payments. The debt interest alone represents £53 billion – money that could potentially be redirected to public services if government debt were eliminated.

Government spending patterns reflect policy priorities and demographic pressures. The large social protection budget reflects an aging population requiring pensions and healthcare, while debt interest payments represent the cost of past government borrowing.

How government expenditure changes affect businesses

Government spending levels significantly influence business activity across the economy. When government increases spending beyond its tax revenues, total spending in the economy rises. This increased aggregate demand typically benefits many businesses through higher sales and revenue.

However, the relationship is complex. Excessive government spending can create economic problems including inflation and pressure for higher interest rates, which can offset the benefits of increased demand.

Recent UK government spending policy

In recent years, the UK government has attempted to reduce spending in various departments to cut government borrowing. The government has worked to reduce the annual deficit – the gap between government spending and tax revenue. This has proved challenging, and deficit reduction has taken longer than initially planned.

Spending cuts have included freezing most public sector pay since 2010. These measures, combined with other austerity policies, have reduced disposable income for many households. This has affected businesses adversely in some sectors, particularly retail. Some retailers have experienced falling demand, and several have collapsed during this period.

The impact of government spending changes varies significantly by industry. Businesses in sectors directly affected by government contracts (such as construction, healthcare suppliers, and defence contractors) are particularly sensitive to spending changes. When government reduces infrastructure spending, construction firms may lose major contracts. Conversely, when government announces major projects, these businesses benefit substantially.

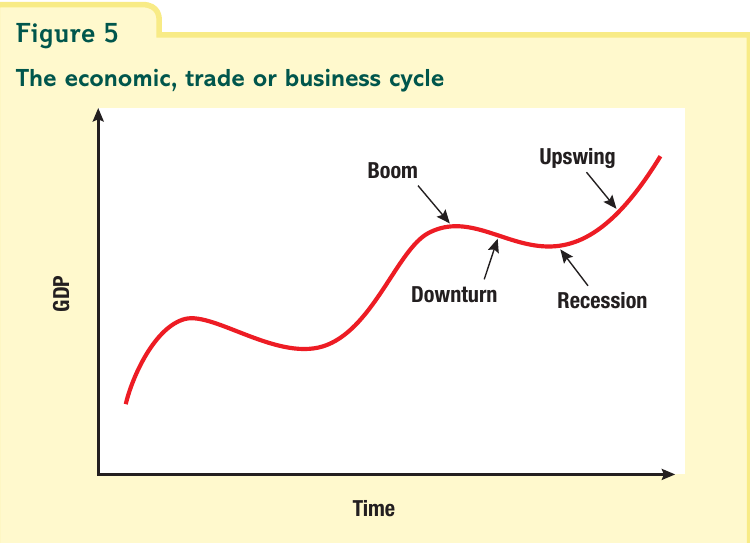

The business cycle

Over time, economies typically grow as measured by Gross Domestic Product (GDP) – the total value of output in the economy. However, this growth is rarely smooth or consistent. Instead, economic growth fluctuates in a pattern known as the business cycle, economic cycle, or trade cycle.

The business cycle describes the recurring pattern of economic expansion and contraction over time. Understanding these phases helps businesses anticipate changes in demand and adjust their strategies accordingly.

Boom

The boom represents the peak of the business cycle when GDP is growing rapidly and the economy is performing strongly. During boom periods, several characteristics emerge:

- Existing businesses expand their operations and new firms enter markets

- Consumer and business demand rises significantly

- Employment grows as businesses recruit to meet increased demand

- Wages typically rise as competition for workers intensifies

- Business profits generally increase due to higher sales volumes

However, boom periods also bring challenges. Prices often rise sharply due to high demand, potentially creating inflation. Asset prices, particularly property, can increase dramatically. In the UK, house prices rose sharply during the boom periods of the 1990s and 2000s when GDP was growing rapidly.

While boom periods seem positive, businesses must be careful not to overextend themselves. Excessive optimism can lead to unsustainable expansion, excessive borrowing, or poor investment decisions that become problematic when the cycle turns.

Downturn

Following a boom, the economy enters a downturn phase. The economy continues growing, but at a declining rate. Key features of a downturn include:

- Demand for goods and services begins to flatten or fall

- Unemployment starts to rise as businesses become more cautious about hiring

- Wage growth slows down as labour market conditions ease

- Many businesses halt expansion plans

- Profits may decline even as revenue continues to grow

- Price inflation slows as demand pressures ease

The downturn phase signals that the economy is losing momentum and may be heading toward recession if conditions continue to deteriorate.

Recession or depression

At the bottom of the business cycle, GDP may become flat or even fall. When GDP declines for two consecutive quarters, economists define this as a recession. A more severe and prolonged decline is called a depression or slump.

Understanding Recession

A recession is officially defined as two consecutive quarters (six months) of negative GDP growth. This technical definition helps economists and policymakers identify when the economy has moved from a slowdown into a more serious contraction requiring policy intervention.

Recession periods are associated with economic hardship. Key characteristics include:

- Demand falls significantly, particularly for non-essential goods and services

- Unemployment rises sharply as businesses cut jobs to reduce costs

- Business confidence collapses, affecting investment decisions

- Bankruptcy rates increase as businesses struggle with falling revenue and existing debts

- Prices may remain flat, and some prices may actually fall (deflation)

During recessions, businesses face severe challenges including reduced revenue, difficulty accessing finance, and pressure to cut costs drastically. Consumer spending falls as unemployment rises and job security concerns increase.

Recovery or upswing

When GDP begins rising again following a recession, the economy enters a recovery or upswing phase. During this phase:

- Business and consumer confidence gradually returns

- Economic activity increases across most sectors

- Demand begins rising for goods and services

- Unemployment starts falling as businesses begin hiring again

- Prices begin rising as demand recovers

- Investment increases as businesses become more optimistic about future growth

Recovery phases can be rapid or gradual depending on economic conditions and policy responses. Government fiscal policy and monetary policy often play important roles in supporting recovery by stimulating demand and maintaining business confidence.

Impact of the business cycle on businesses

The business cycle's fluctuating pattern significantly affects business performance, though the magnitude of impact varies by sector and business type. Businesses must understand these patterns to plan effectively and manage risks.

During boom periods, most businesses benefit from rising demand and can expand operations. However, they must be careful not to overextend themselves, as boom periods eventually end. Businesses need to manage cash flow carefully and avoid taking on excessive debt that could become problematic when conditions deteriorate.

Strategic Planning Across the Cycle

Successful businesses plan for the entire business cycle, not just current conditions. This means:

- Building cash reserves during boom periods to survive downturns

- Maintaining financial flexibility to invest when opportunities arise during recessions

- Avoiding excessive fixed costs that become burdensome when demand falls

- Diversifying products and markets to reduce cyclical exposure

During downturns and recessions, businesses face falling demand and must focus on cost control and efficiency. Some businesses may need to restructure operations, reduce workforce, or exit unprofitable markets. However, recessions can also create opportunities for well-positioned businesses to gain market share or acquire struggling competitors.

Different industries experience different impacts. Luxury goods and services typically suffer more during downturns as consumers prioritise essential spending. In contrast, discount retailers or budget service providers may actually benefit as consumers trade down to cheaper alternatives.

Businesses selling essential goods and services tend to be more resilient during economic downturns, as demand for necessities remains relatively stable. However, even these businesses may face pressure on profit margins as consumers become more price-sensitive.

Worked Example: Sector Impact During Recession

During the 2008-2009 recession:

Luxury car manufacturers experienced sharp sales declines of 30-40% as consumers postponed expensive purchases and switched to cheaper alternatives.

Discount supermarkets (like Aldi and Lidl) saw sales increase by 20-30% as consumers traded down from premium supermarkets to save money.

Healthcare providers maintained relatively stable demand, as people still needed medical services regardless of economic conditions, though some elective procedures were postponed.

Understanding the business cycle helps businesses make informed decisions about timing investments, managing inventory levels, adjusting pricing strategies, and planning workforce requirements.

Exam focus: evaluation skills

When evaluating the impact of taxation or government expenditure changes on businesses, consider:

Critical Evaluation Factors

Context matters: The effect depends on the type of business, its target market, and competitive position. A tax increase affecting luxury goods hits premium brands harder than budget alternatives.

Time horizons: Short-term impacts may differ from long-term effects. Initially, tax increases reduce consumer spending, but over time consumers may adjust and spending patterns normalise.

Magnitude of change: Small tax adjustments have modest impacts, while major changes significantly affect business planning and consumer behaviour.

Stakeholder perspectives: Changes affect different stakeholders differently. Corporation tax increases may benefit government finances but reduce shareholder returns.

Alternative actions: Businesses have choices in responding to tax or spending changes, and their strategic responses affect outcomes.

External factors: Taxation changes don't occur in isolation. Consider interactions with other economic conditions, such as interest rates, exchange rates, and global economic trends.

Remember!

Key points:

- Fiscal policy involves government using taxation and spending to influence the economy and business activity

- Direct taxes (on income) and indirect taxes (on spending) affect businesses and consumers differently through various mechanisms

- Tax increases typically reduce consumer spending power and business profitability, while tax cuts have the opposite effect

- Government expenditure changes affect aggregate demand and impact businesses differently depending on their sector

- The business cycle consists of four phases: boom, downturn, recession, and recovery, each creating different opportunities and challenges for businesses

Key terms:

- Fiscal policy: Government policy using taxation and spending to influence economic activity

- Direct taxes: Taxes charged on income and profits (income tax, corporation tax, National Insurance)

- Indirect taxes: Taxes charged on spending (VAT, excise duties, customs duties)

- GDP (Gross Domestic Product): The total value of output produced in an economy

- Business cycle: The recurring pattern of economic expansion and contraction over time

- Deficit: The difference between government spending and tax revenue

- Boom: Period of rapid economic growth and high GDP

- Recession: Period when GDP falls for two consecutive quarters

- Tax avoidance: Legal methods of minimising tax liability

- Tax evasion: Illegal methods of avoiding tax payment

Critical frameworks:

- Taxation affects businesses through multiple channels: consumer spending, prices, costs, profits, investment, and employment decisions

- The business cycle creates predictable patterns of demand fluctuation that businesses must anticipate and plan for

- Government spending changes have multiplier effects throughout the economy, affecting both direct suppliers and businesses more broadly through changes in aggregate demand