Financial Planning (Edexcel A-Level Business): Revision Notes

Budgets

What is a budget?

A budget is a quantified financial plan prepared and agreed in advance. It differs from a forecast in an important way: a forecast predicts what might happen, whereas a budget sets out what the business intends to achieve. Budgets show planned spending and how it will be financed, based on business objectives.

Most budgets cover twelve months to align with the accounting period, though exceptions exist. Both large and small businesses use budgets as a method of financial control.

Budget vs Forecast: While both involve financial planning, a budget is a commitment to targets the business aims to achieve, whereas a forecast is simply a prediction of what may occur based on current trends.

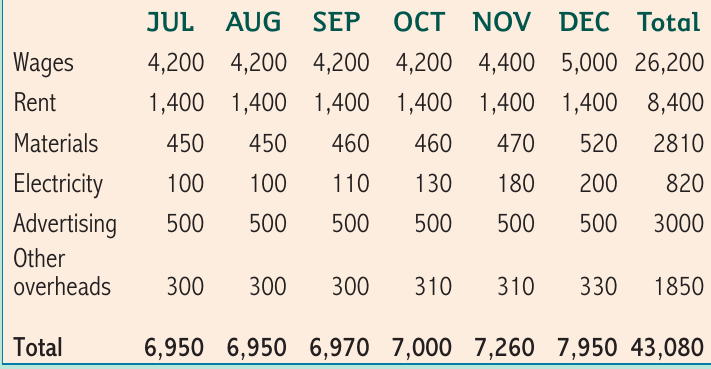

The example above shows a six-month cost budget for a hair salon. Total planned costs for the period are £43,080, with costs rising from £6,950 in July to £7,950 in December. The December spike likely reflects seasonal factors such as increased customer demand before Christmas.

Purpose of budgets

Budgets fulfil six key purposes in business management:

Control and monitoring: Budgets allow managers to control operations by setting specific targets. Actual performance can be measured against these targets, variances identified, and corrective action taken. Many businesses produce weekly budgets for rapid intervention when problems arise.

Planning: Budgeting forces managers to think ahead rather than reacting to events day-by-day. It encourages anticipation of future problems and development of solutions in advance.

Proactive vs Reactive Management: The planning function of budgets transforms management from reactive firefighting to proactive strategic thinking, enabling businesses to prepare for challenges before they arise.

Co-ordination: In larger businesses with multiple departments and sites, budgets help co-ordinate activities across different areas. This is particularly important for multinational companies with operations spread globally.

Communication: Budgets communicate business objectives to the workforce. They provide a clear framework for decision-making and remove uncertainty. They also highlight priorities and identify costs requiring close control.

Efficiency: Budgets enable delegation of financial decision-making to lower management levels. Senior managers cannot efficiently make every decision across a medium or large business, so budgets empower those closest to operational activities.

Motivation: Budgets provide workers with targets and standards to achieve. Meeting or exceeding budget targets indicates success and can motivate departments and teams. The desire to avoid budget shortfalls can also incentivise performance.

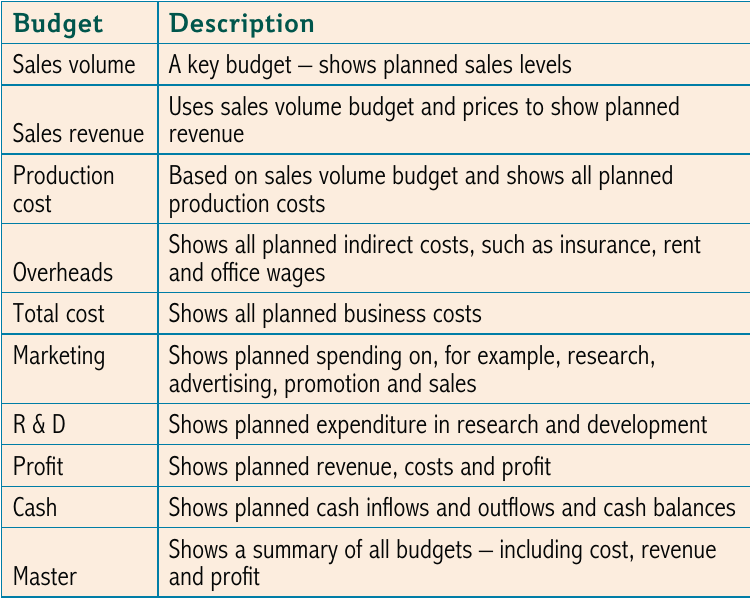

Types of budget

Businesses use various budget types depending on their needs. The table below shows common examples:

Historical figures approach

Most budgets use historical figures – data from past trading periods. Businesses adjust these figures for known future events such as planned production changes, cost increases, or price adjustments. Two key budgets are the sales budget and production cost budget.

Sales volume budget

This shows planned sales levels for each product over the budget period.

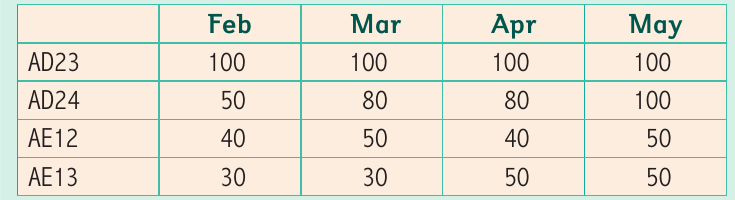

Worked Example: Sales Volume Budget

The example shows Emerald Artwork planning to sell four products (AD23, AD24, AE12, AE13) with volumes varying by product and month:

- Product AD23 maintains consistent sales of 100 units monthly

- Product AD24 shows growth from 50 to 100 units

This demonstrates how sales volume budgets track planned unit sales across different products and time periods.

Sales revenue budget

This budget combines sales volume with product prices to calculate expected revenue.

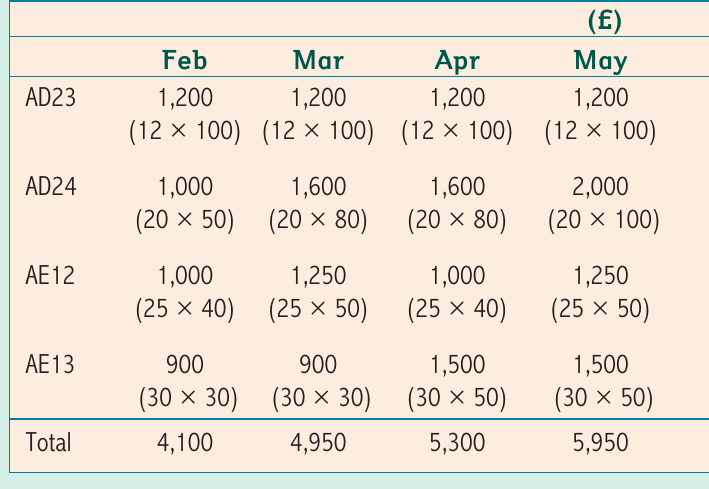

Worked Example: Calculating Sales Revenue

For Emerald Artwork, if product AD23 sells for £12 per unit and 100 units are sold:

Total monthly revenue ranges from £4,100 in February to £5,950 in May, showing growth over the period.

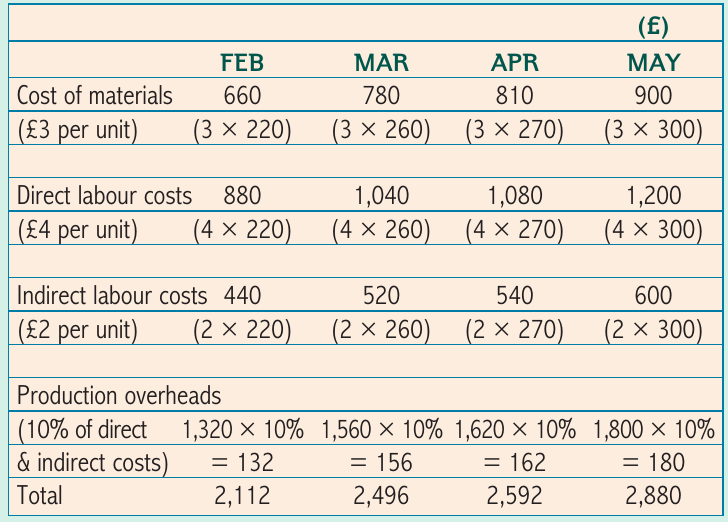

Production cost budget

This details all planned production costs including materials, labour, and overheads.

Worked Example: Production Cost Budget

For Emerald Artwork, production costs include:

- Materials at £3 per unit

- Direct labour at £4 per unit

- Indirect labour at £2 per unit

- Production overheads at 10% of combined direct and indirect labour costs

Calculation for one unit:

Total production costs rise from £2,112 in February to £2,880 in May as output increases.

Zero-based budgeting (ZBB)

Unlike historical budgeting, zero-based budgeting allocates no money unless spending can be justified. Managers must demonstrate that each cost generates adequate benefits relative to business objectives. This differs from simply adjusting past costs by a percentage.

ZBB links to opportunity cost – the value of the next best alternative foregone. Both concepts emphasise value for money.

Advantages of ZBB:

- Improves resource allocation

- Develops a questioning attitude that reduces unnecessary costs

- May improve staff motivation through skill development and better business understanding

- Encourages managers to consider alternatives

Disadvantages of ZBB:

- Time-consuming due to detailed information collection and analysis

- Requires skilled decision-making that may not be available

- Threatens existing practices, potentially affecting motivation adversely

- Managers may avoid justifying costs that could benefit the business

Hybrid Approach: To address ZBB's disadvantages, businesses sometimes provide departments with a base budget (e.g. 50% of previous spending) then invite bids for additional funding on a ZBB basis. This balances efficiency with practicality.

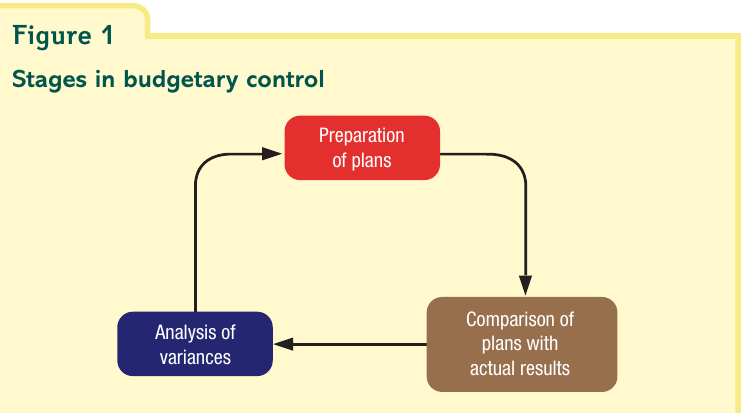

Using budgets: budgetary control

Budgetary control involves using budgets to plan future activities, compare actual results with plans, and investigate differences. The process follows three stages in a continuous cycle:

1. Preparation of plans: Businesses set objectives and translate these into specific, measurable targets within budgets. This establishes benchmarks for comparison.

2. Comparison of plans with actual results: Once the budget period ends, managers compare actual financial outcomes with budgeted figures. Modern information technology enables rapid data availability. Most businesses divide the year into control periods (typically four weeks or one calendar month) for timely monitoring.

3. Analysis of variances: This critical stage identifies reasons for differences between planned and actual outcomes. Variances may result from external factors requiring business plan adjustments or internal issues needing corrective action.

Variances

A variance is the difference between budgeted and actual figures. Variances are calculated at the end of each budget period when actual data becomes available.

Favourable vs adverse variances

Favourable variances (F) occur when actual figures are better than budget:

- Actual sales revenue exceeds planned revenue

- Actual costs are lower than planned costs

Example: Favourable Sales Variance

If budgeted sales revenue is £25,000 but actual revenue is £29,000:

This positive variance of £4,000 indicates the business performed better than planned.

Adverse variances (A) occur when actual figures are worse than budget:

- Actual sales revenue falls below planned revenue

- Actual costs exceed planned costs

Example: Adverse Cost Variance

If budgeted costs are £20,000 but actual costs are £22,000:

This adverse variance of £2,000 indicates costs exceeded the budget.

Types of variance

Variances can be calculated for any budgeted item including:

- Sales revenue

- Sales volume

- Wages

- Materials

- Overheads

- Labour hours

Profit Variance: The profit variance is particularly important as it reflects all other variances – any change in cost or revenue affects profit. A business may have multiple favourable variances but still show an adverse profit variance if costs increased more than revenue.

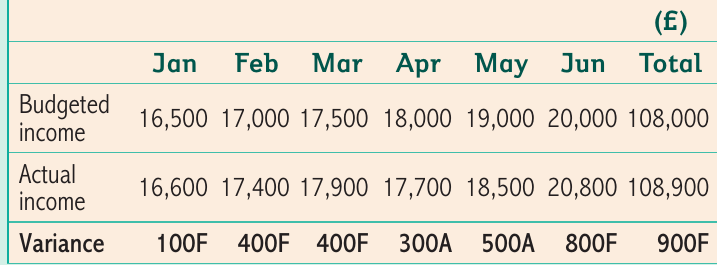

Worked examples: income variances

This table shows Wishart Ltd's income variances over six months. Most variances are favourable, suggesting:

- Ability to charge higher prices

- Increased demand from successful marketing

- Quality improvements

- Rising consumer incomes

- Changing consumer preferences

The total favourable income variance is £900 over the period.

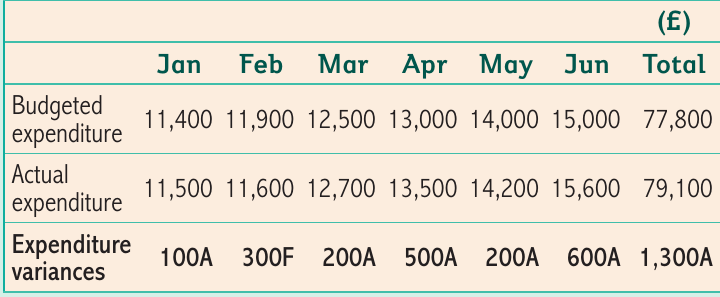

Worked examples: expenditure variances

Wishart Ltd's expenditure variances are mostly adverse, possibly due to:

- Higher production volumes increasing costs

- Supplier price increases

- Production inefficiencies

- Wage increases from worker demands

The total adverse expenditure variance is £1,300.

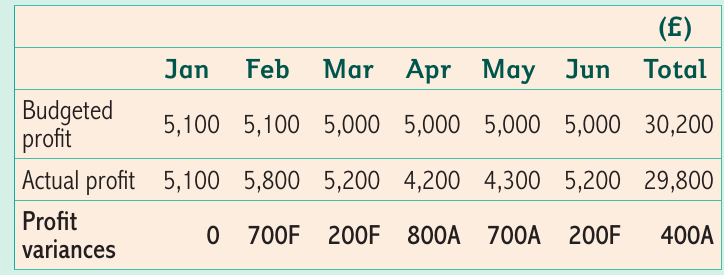

Worked examples: profit variances

Worked Example: Net Profit Variance

Wishart Ltd's profit variances show an overall adverse variance of £400 for the six-month period.

Analysis:

The adverse profit variance occurs primarily because costs exceeded budget more than revenue increased. Despite favourable income variances, the larger adverse cost variances resulted in an overall negative impact on profitability.

Combined Impact: A profit variance reflects the net effect of all income and cost variances. Businesses must investigate both favourable and adverse variances to understand their combined impact on profitability.

Using variances for decision-making

Variance analysis – calculating variances and identifying their causes – provides crucial information for business decisions.

Example: Responding to Variances

Scenario 1: Adverse cost variance from supplier price increases

- Action: Search for alternative suppliers or negotiate better terms

Scenario 2: Favourable sales variance from effective advertising

- Action: Increase use of similar campaigns to maintain momentum

Scenario 3: Adverse profit variance from production inefficiencies

- Action: Review production processes and implement improvements

Understanding variance causes enables managers to:

- Take corrective action to avoid adverse variances

- Replicate factors that created favourable variances

- Make informed decisions about resource allocation

- Improve future budget accuracy

Difficulties of budgeting

Despite their benefits, budgets present several challenges:

Setting budgets

Inaccurate estimates: Budget figures represent plans, not certainties. They rely on historical data, forecasts, and judgement. Simply taking last year's figures and adding a percentage may produce unreliable budgets.

Dependency on Sales Data: Most budgets depend on sales forecasts. If sales data are inaccurate, all related budgets (production, cash flow, etc.) will be flawed. This creates a domino effect where one error undermines the entire budgeting system.

Departmental conflict: Limited funds create competition between departments. Marketing may seek promotion budgets while R&D needs new equipment, forcing difficult choices.

Opportunity cost: Time spent budgeting cannot be spent on other activities. Sales managers preparing budgets could instead be securing customers and generating revenue.

Over-ambitious Objectives: Setting unrealistic targets makes budgets meaningless as benchmarks. If objectives are unachievable, comparing actual results to budget becomes pointless and can severely demotivate staff.

Motivation issues

When workers are excluded from budget planning, using budgets as motivational tools becomes difficult. Unrealistic budgets can demotivate rather than inspire staff.

Manipulation

Managers may manipulate budgets for personal or departmental benefit. A manager with influence over budget-setting might establish easily achievable targets that make their department appear successful without genuinely contributing to business objectives.

Rigidity

Budgets can constrain business flexibility. For example, departments may disagree about vehicle replacement timing. Keeping older vehicles reduces immediate costs but increases maintenance expenses and delivery unreliability, potentially causing customer dissatisfaction and lost sales. Rigid budget constraints may prevent optimal decisions.

Short-termism

Long-term vs Short-term Trade-offs: Managers focused excessively on current budgets may undermine long-term performance. For instance, reducing customer service staffing to meet labour cost budgets may save money now but drive customers away through poor service, damaging future performance.

Key Points to Remember:

-

A budget is a financial plan agreed in advance – it sets targets the business aims to achieve, unlike a forecast which merely predicts possibilities

-

Budgets serve six purposes: control and monitoring, planning, co-ordination, communication, efficiency, and motivation

-

Variance analysis compares actual results with budgets – favourable variances (F) exceed expectations positively, while adverse variances (A) indicate underperformance

-

Zero-based budgeting (ZBB) requires justification for all spending rather than basing budgets on historical figures, encouraging cost efficiency but requiring significant time and skill

-

Businesses face several budgeting difficulties including inaccurate estimates, departmental conflicts, manipulation, rigidity, and short-term thinking that may compromise long-term success

Key terms: budget, budgetary control, variance, variance analysis, historical figures, zero-based budgeting, favourable variance, adverse variance, sales budget, production cost budget, master budget