Managing Finance (Edexcel A-Level Business): Revision Notes

Causes of business failure

Introduction

Business failure is a significant reality in the UK economy. While thousands of new businesses launch each year, a similar number collapse. Historical data shows business failures peaked around 26,000 annually in 2009 following the financial crisis, and have remained around 24,000 per year since then. More concerning is that over 90% of business start-ups cease trading within five years.

Understanding why businesses fail is crucial for entrepreneurs, managers and stakeholders. Causes can be classified as either internal (within the business's control) or external (beyond the business's control), and as either financial or non-financial factors. However, most non-financial problems eventually manifest as financial difficulties if left unresolved.

Internal causes of business failure

Internal factors originate from within the business itself and often result from poor management decisions or inadequate planning. These are theoretically controllable, making them particularly important to understand and avoid.

Lack of planning

Insufficient planning is a major cause of business failure, particularly among start-ups. Entrepreneurs often underestimate the importance of developing a comprehensive business plan, eager to begin trading without taking time for thorough preparation.

A robust business plan provides:

- Clear vision and direction for business development

- Identification of potential problems before they occur

- A roadmap showing how the business will evolve

- Essential financial projections linking operating costs, pricing and profit expectations

- Evidence to attract potential investors and lenders

Financial planning is particularly critical. Entrepreneurs must ensure adequate funding to survive weak cash flow during early trading periods. Without proper planning, businesses lack the foresight to navigate challenges and often run out of money before becoming established.

Successful entrepreneurs seek advice from experienced business people, attend relevant training courses, and consult specialists during the planning phase. This preparation significantly reduces failure risk.

Cash-flow problems

Cash-flow difficulties are the single most common reason for business failure. Many entrepreneurs focus excessively on profit while neglecting liquidity. A business can be profitable on paper but still collapse if it cannot meet immediate payment obligations.

Overtrading

Overtrading occurs when a business attempts to fund a large volume of production with inadequate working capital. This is particularly common among rapidly growing businesses that expand faster than their cash resources can support.

Case Study: Astec Building Contractor

Astec, a specialist building contractor, grew from $30 million to $45 million sales in one year. Despite being profitable, the company couldn't fund the additional working capital requirements. This rapid expansion strained resources, caused catastrophic cash-flow problems, and led to collapse with debts of $12 million.

Key lesson: Growth without adequate cash resources can destroy even profitable businesses.

Investing too much in fixed assets

New businesses have limited initial funds. Spending heavily on equipment, vehicles and other capital assets drains precious cash reserves. A better strategy is often to lease fixed assets, preserving cash for day-to-day operations. This provides flexibility and maintains liquidity during vulnerable early periods.

Allowing too much credit

While business-to-business trading commonly involves credit terms, allowing customers excessive payment periods creates problems. Businesses must pay their own suppliers while waiting for customer payments, potentially forcing them to borrow to cover the gap.

Poor credit control (management of customer debts) leads to:

- Extended periods without cash inflows

- Increased borrowing costs during waiting periods

- Bad debts when customers fail to pay

- Strained relationships with own suppliers

Over-borrowing

Businesses often borrow to finance growth, but excessive borrowing creates multiple problems:

- Rising interest payments reduce available cash

- Debt obligations continue regardless of trading performance

- Lenders may demand repayment or impose restrictions

- Overall business control becomes compromised

A balanced funding approach combining loans with equity finance (share capital) reduces these risks. The 2008 credit crunch demonstrated how withdrawal of lending support causes business failures.

Seasonal factors

Some industries experience predictable fluctuations in cash flow:

- Agriculture: Large inflows at harvest, expenses throughout the year

- Tourism: Summer peaks, winter troughs

- Retail: Christmas trading surge, quieter periods

While seasonal patterns are foreseeable and can be planned for using cash-flow forecasts, businesses must maintain sufficient reserves to survive low-income periods.

Unforeseen expenditure

Unexpected costs can devastate businesses unprepared for emergencies:

- Equipment breakdowns requiring immediate replacement

- Unexpected tax demands

- Legal costs from disputes

- Bad debts from customer failures

- Strike action disrupting operations

Inexperienced entrepreneurs are particularly vulnerable to unforeseen expenditure because they lack awareness of potential problems and haven't built contingency reserves.

Poor financial management

Inadequate understanding of cash-flow dynamics causes many failures. Common mistakes include:

- Spending anticipated income before it actually arrives

- Failing to produce regular cash-flow forecasts

- Not maintaining up-to-date financial records

- Operating without effective credit control systems

- Confusing profit with cash

Exam insight: Remember that profitable businesses can still collapse if they run out of cash. Examiners frequently test understanding of this counterintuitive concept. Overtrading is the classic scenario where strong sales growth exhausts cash resources faster than profits can replenish them.

Lack of funds

Many businesses fail because they cannot attract sufficient funding. This affects both new and established businesses, though for different reasons:

Established businesses may struggle to secure funding because:

- Poor trading history makes them too risky for investors

- Previous losses or problems damage credibility

- Lenders doubt their ability to repay

New businesses face funding challenges because:

- No trading history exists to demonstrate viability

- Uncertainty about market acceptance

- Perceived high risk deters investors and lenders

Some entrepreneurs believe they can succeed with minimal capital by operating cautiously. However, undercapitalised businesses almost inevitably fail. Insufficient funding means they cannot:

- Purchase adequate stock

- Invest in necessary equipment

- Market effectively

- Weather initial trading difficulties

- Take advantage of growth opportunities

The 2008 financial crisis demonstrated how funding shortages destroy businesses. Even viable companies collapsed when lenders became risk-averse and withdrew credit facilities.

Relying on a narrow customer base

Businesses depending heavily on a small number of large customers face significant vulnerability. Losing even one major customer can cause sales to plummet, making survival difficult.

Case Study: UK Farmers and Supermarket Contracts

Many UK farmers have collapsed after losing contracts with major supermarket chains. When contract terms couldn't be agreed, these farmers were left without sufficient alternative customers, forcing them out of business despite having productive capacity.

Key lesson: Diversify your customer base to ensure that losing any single customer doesn't threaten survival.

Marketing problems

Various marketing failures can cause business collapse:

Product problems: Launching products that fail to meet customer needs results in poor sales and wasted investment. Insufficient market research often underlies this failure.

Pricing problems:

- Prices set too high reduce demand and sales volume

- Prices set too low fail to cover costs or suggest poor quality

- Inappropriate pricing strategies for target market positioning

Promotional problems: Excessive spending on advertising or choosing ineffective promotional channels wastes resources without generating corresponding sales increases.

Positioning problems: Businesses must position themselves clearly in the market. Being "stuck in the middle" – neither clearly cheap nor premium – confuses customers and weakens competitive advantage.

Case Study: Jane Norman Fashion Chain

Jane Norman, a women's fashion chain, went into administration in 2014. The brand was positioned between budget and premium sectors, appealing to neither market segment. In competitive retail conditions, this unclear positioning made the business unviable, and its owner could no longer fund continuing losses.

Key lesson: Clear market positioning is essential – avoid being stuck in the middle.

Failure to innovate

Businesses that resist change and fail to innovate often become obsolete. Common reasons include:

- Reluctance to adopt new technology

- Complacency about established market positions

- Failure to recognise changing market dynamics

- Attachment to traditional methods

Case Study: Kodak's Digital Photography Failure

Kodak's collapse illustrates innovation failure perfectly. Despite inventing digital camera technology, Kodak's management failed to recognise its importance. They believed consumers would always prefer physical photographs for their quality.

This misjudgement was catastrophic – digital photography came to dominate because consumers valued convenience over traditional print quality. Kodak's inability to adapt to the world changing around them led directly to collapse.

Key lesson: Innovation and adaptation are essential for survival, even when you invented the disrupting technology.

Lack of business skills

Running a business requires diverse competencies. Entrepreneurs need skills in:

- Financial management and accounting

- Marketing and sales

- Communication and negotiation

- IT and technology

- Leadership and motivation

- Strategic decision-making

It's unsurprising that some business owners lack all these skills. However, skill gaps create serious problems:

- Poor decisions result from incomplete understanding

- Opportunities are missed

- Threats aren't recognised early enough

- Resources are mismanaged

Example: A Variety Shopping Ltd store owner admitted having limited retail experience when starting. He described the venture as "not a very nice experience" and said he "wouldn't do it again," having lost considerable money. This honest reflection highlights how lack of relevant business skills contributes to failure.

Successful entrepreneurs either develop necessary skills through training and experience, or recruit team members who complement their skill gaps.

Poor leadership

Senior management failures can single-handedly destroy businesses. Leadership problems include:

- Poor strategic decision-making

- Failure to implement necessary changes

- Not recognising or responding to market shifts

- Disastrous merger or acquisition decisions

Examples of leadership failures:

- Kodak: Management failed to implement crucial strategies needed to adapt to digital photography

- Blockbuster: Leadership didn't respond effectively to streaming technology and changing consumer viewing habits

- Nokia: Senior managers failed to compete effectively against smartphones

- Co-operative Bank: Blamed for poor decision to take over Britannia Building Society

- RBS: Fred Goodwin's leadership and ABN Amro takeover decision contributed to near-collapse

Strong leadership is crucial for business survival. Leaders must recognise market changes, make timely decisions, and drive necessary organisational changes even when uncomfortable.

External causes of business failure

External factors are circumstances beyond the business's direct control. While business owners sometimes blame external factors to deflect personal responsibility, only about 20% of business failures result primarily from external forces. However, these external pressures are real and can overwhelm even well-managed businesses.

Competition

Competitive pressure can force businesses to exit markets. Rivals may succeed by:

- Developing superior products or services

- Better understanding market conditions and customer needs

- Operating with lower cost structures enabling cheaper pricing

- Using predatory tactics like destroyer pricing (pricing below cost to eliminate competitors)

Global competition has intensified pressure on UK manufacturers. Many have been outcompeted by low-cost producers from China and other emerging economies. These international competitors often have significant cost advantages from cheaper labour, lower regulatory costs, or economies of scale.

Businesses must constantly monitor competition and adapt to maintain competitive advantage. Those unable to differentiate themselves or match competitive offerings risk failure.

Changes in legislation

Government legislation can make existing business models unviable. When laws change, businesses must either adapt or exit markets.

Examples of Legislation Impact:

-

Smoking ban: Pubs and bars blamed legislation prohibiting smoking in public places for declining trade and subsequent failures

-

Payday loan regulation: Government controls on short-term lending forced several lenders to withdraw from the market entirely

-

"Pasty tax": West Cornwall Pasty Company cited new tax rules on hot takeaway food as contributing to administration (though the business was subsequently rescued)

Key lesson: Monitor proposed legislation and lobby where appropriate, but ultimately must comply with new laws or cease affected operations.

Changes in consumer tastes

Consumer preferences evolve over time. Businesses unable to adapt face declining demand and eventual failure.

Fashion, technology and food industries experience particularly rapid taste changes. What's popular today may be obsolete tomorrow. Businesses must invest in market research, monitor trends, and demonstrate flexibility to evolve with changing preferences.

Case Study: Northern Ireland Fashion Chains

Two Northern Ireland fashion chains (NV and All Gino Casuals) closed 15 stores when their parent company entered liquidation. Retail analysts attributed failure to inability to adapt to "changing patterns and trends in consumer behaviour in the fashion industry."

Key lesson: Continuously innovate and refresh offerings to maintain relevance with target customers.

Economic conditions

The overall state of domestic and global economies significantly impacts business survival. Economic downturns create multiple challenges:

Recession effects:

- Reduced consumer spending as incomes fall

- Increased unemployment reducing demand

- Business customers cutting orders

- Difficulty obtaining credit

The 2008 financial crisis demonstrated this dramatically. Business failures increased significantly as recession gripped the UK economy. Thousands of businesses collapsed as demand evaporated and credit became unavailable.

Government economic policies also affect businesses:

- Public sector cuts reduce government purchasing and employment

- Wage freezes limit disposable income growth

- Tax increases reduce consumer spending power

- Reduced demand particularly affects non-essential products and services

Interest rates influence borrowing costs and consumer spending:

- Low rates (like post-2008) make borrowing cheaper, supporting business investment and consumer purchases on credit

- Sharp rate increases threaten heavily indebted businesses and reduce credit-based consumer spending

Exchange rates impact import and export businesses:

- Rising exchange rates make UK exports more expensive to foreign buyers, reducing demand and threatening export-dependent businesses

- Falling exchange rates increase import costs, squeezing margins for businesses dependent on imported materials

Changes in market prices

Some businesses are price takers – they must accept prevailing market prices rather than setting their own. When market prices fall below break-even levels, marginal producers cannot survive.

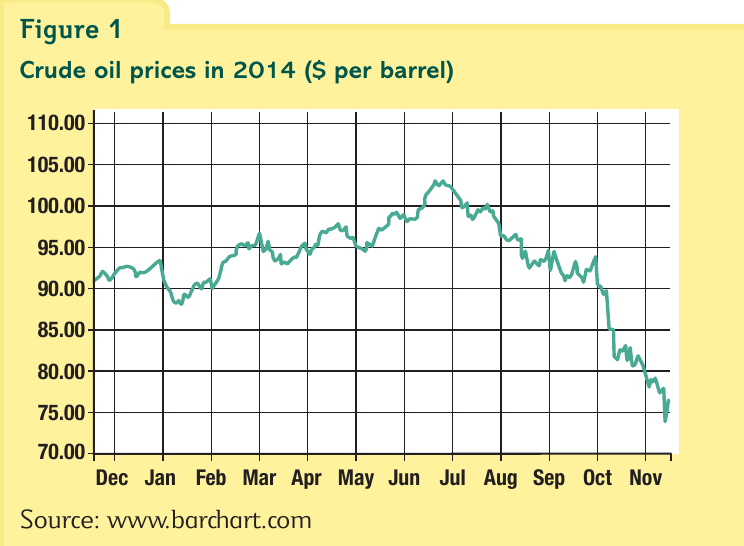

Example: Oil Producers

The global oil price determines oil producers' revenue. When prices collapsed in late 2014 (shown in the chart below), many producers faced losses. Oil falling from $103 per barrel in June to $74 in November threatened any producer with break-even costs above $73.

Example: UK Dairy Farmers

In 2014, dairy farmers' livelihoods were threatened when milk prices fell to 27p per litre – below the 30p break-even price for many producers. Without control over prices, these farmers faced losses and potential business failure.

Key lesson: Price takers must focus on cost control and efficiency to survive when market prices fall. However, when prices drop below production costs for extended periods, even efficient producers may be forced to exit.

Financial and non-financial causes of business failure

The causes of business failure can be classified into two broad categories:

Financial causes

Financial failure means a business becomes either:

- Bankrupt (taken to court by creditors unable to secure payment)

- Insolvent (voluntarily ceasing trading because unable to pay debts)

The most common financial cause is cash shortage – inability to pay immediate debts as they fall due. Multiple factors can cause cash shortages:

- Overtrading (growing too fast)

- Poor credit control (customers paying too slowly)

- Excessive investment in fixed assets

- Over-borrowing creating high interest costs

- Seasonal fluctuations

- Unforeseen emergency expenditure

- Bad debts from customer failures

Effective cash-flow management is absolutely crucial. Many profitable businesses have collapsed purely because they ran out of cash at critical moments. Understanding the difference between profit and cash is essential for business survival.

Non-financial causes

Non-financial factors don't directly relate to money issues but create conditions leading to failure:

- Inadequate planning

- Insufficient business skills

- Inability to compete effectively

- Failure to meet customer needs

- Reluctance to change or innovate

- Poor leadership decisions

- Adverse economic conditions

However, even these non-financial causes ultimately result in financial failure if unaddressed. For example:

- Poor planning → inadequate funding → cash shortage

- Lack of innovation → declining sales → falling revenue → losses

- Weak leadership → poor decisions → competitive disadvantage → reduced profits

The distinction between financial and non-financial causes helps identify root problems. A business experiencing cash-flow difficulties might treat symptoms (arranging emergency loans) without addressing underlying causes (inadequate planning or poor marketing). Sustainable solutions require identifying and resolving root causes.

Remember!

Key Points to Remember:

-

Most business failures result from internal factors (poor management, inadequate planning, weak cash-flow management) rather than external forces. These are controllable and preventable.

-

Cash-flow problems are the number one cause of business collapse, more important than profitability. Profitable businesses can still fail if they run out of cash. Overtrading (growing too fast without adequate working capital) is a classic example.

-

Overtrading means attempting to fund large production volumes with inadequate cash resources. It particularly affects rapidly growing businesses that expand faster than their cash position can support.

-

External factors (competition, legislation changes, economic conditions, market price changes, shifting consumer tastes) account for only about 20% of failures but can overwhelm even well-managed businesses.

-

All causes eventually become financial causes if left unresolved. Non-financial problems (poor planning, weak leadership, inadequate skills) ultimately manifest as cash shortages, insolvency or bankruptcy. Early identification and resolution of root causes is essential for business survival.