Liquidity (Edexcel A-Level Business): Revision Notes

Liquidity

Liquidity measures a business's ability to meet its short-term debts and financial obligations. It is crucial for survival - without sufficient liquid resources, a business cannot pay wages, suppliers, or other immediate bills, which can lead to financial collapse.

Poor liquidity management is one of the most common causes of business failure, even when a company appears profitable on paper. Cash flow problems can force otherwise successful businesses into administration.

What is liquidity?

Liquidity refers to how easily an asset can be converted into cash. Cash itself is the most liquid asset. A business with good liquidity has enough resources available to pay its immediate debts as they fall due.

Working capital (also called circulating capital) is the money available to pay for day-to-day trading operations. This includes wages, utility bills, raw materials, and other immediate expenses. Without adequate working capital, businesses struggle to function effectively.

Think of liquidity like having money in your wallet versus having money tied up in a house. Your wallet money is immediately available (highly liquid), but selling a house takes time and effort (less liquid). Businesses face the same challenge - they need enough readily available resources to meet immediate needs.

Statement of financial position (balance sheet)

A statement of financial position (also called a balance sheet) is a financial document that shows the financial position of a business at a specific point in time - like a snapshot. It summarises what the business owns (assets), what it owes (liabilities), and the capital invested by owners.

The fundamental accounting equation

The balance sheet is built on a fundamental relationship:

This equation must always balance because every asset owned by the business has been financed either by the owners (capital) or by borrowing (liabilities).

Worked Example: Understanding the Accounting Equation

If a business has capital of $5 million and liabilities of $2.6 million, its total assets must equal:

The business owns $7.6 million in total assets, financed by $5 million from owners and $2.6 million from borrowing.

Key components defined

Assets are resources owned by the business that provide economic value. Examples include:

- Buildings and land

- Machinery and equipment

- Vehicles

- Inventory (stock)

- Cash in the bank

- Money owed by customers

Liabilities are the debts of the business - money owed to external parties. Examples include:

- Bank loans

- Overdrafts

- Money owed to suppliers

- Tax owed to the government

- Mortgages

Capital (or equity) represents the money put into the business by its owners. It includes:

- Share capital (for limited companies)

- Retained earnings (accumulated profits kept in the business)

Structure of the statement of financial position

Businesses present their balance sheets in a vertical format, with assets at the top and liabilities and equity at the bottom. Here is a typical structure:

Non-current assets

Non-current assets (also called fixed assets) are long-term resources used repeatedly by the business over time. They are not intended for immediate sale. Examples include:

- Property and equipment: Buildings, land, machinery, tools, vehicles, fixtures and fittings

- Intangible assets: Non-physical assets such as brand names, patents, trademarks, customer lists, and franchising agreements

These assets provide value over many years and are essential for business operations.

Current assets

Current assets are assets expected to be converted into cash within 12 months. They are liquid assets. The three main categories are:

- Inventories: Stocks of raw materials, components, work-in-progress, and finished goods ready for sale

- Trade and other receivables: Money owed to the business, including:

- Debtors (customers who bought on credit)

- Prepayments (payments made in advance, such as insurance premiums)

- Cash and cash equivalents: Physical cash on premises and money held in bank accounts

Current assets represent the most liquid resources available to meet short-term obligations. The order above generally reflects their liquidity - cash is most liquid, while inventories are least liquid as they must first be sold.

Current liabilities

Current liabilities are debts that must be repaid within one year. They represent immediate financial obligations. Examples include:

- Loans and other borrowings: Short-term bank loans and overdrafts

- Trade and other payables: Money owed to suppliers for goods, services, and utilities (also called trade creditors)

- Current tax liabilities: Tax owed to authorities, including income tax, VAT, and corporation tax

Non-current liabilities

Non-current liabilities (also called long-term liabilities) are debts that do not need to be repaid for at least one year. Examples include:

- Long-term bank loans

- Mortgages

- Company pension fund obligations

Net assets and shareholders' equity

Net assets are calculated by subtracting total liabilities from total assets:

Shareholders' equity represents what the business owes to its owners. It appears at the bottom of the balance sheet and includes:

- Share capital (money invested by shareholders)

- Retained earnings (profits kept in the business rather than distributed as dividends)

Net assets will always equal shareholders' equity because of the fundamental accounting equation. This provides a built-in check that the balance sheet is correctly prepared.

Measuring liquidity

The balance sheet provides information to calculate two important liquidity ratios. These ratios help assess whether a business can meet its short-term debts.

Current ratio

The current ratio measures whether a business has enough current assets to cover its current liabilities. It is calculated as:

Interpretation:

- A healthy current ratio is generally between 1.5:1 and 2:1

- A ratio below 1.5:1 suggests the business may lack sufficient working capital and could be over-borrowing or overtrading

- A ratio above 2:1 may indicate too much money is tied up unproductively in assets like stock

- Exception: Retailers often operate successfully with lower ratios (around 1:1 or below) because they hold fast-selling stock and generate cash quickly from sales

Common Mistake to Avoid:

Don't assume that a low current ratio always means poor financial health. The acceptable ratio varies significantly by industry. Retailers and supermarkets can operate successfully with ratios around 1:1 or even lower because they turn inventory into cash very quickly. Always consider the business context when interpreting ratios.

Acid test ratio

The acid test ratio (also called the quick ratio) is a more stringent test of liquidity. It excludes inventories from current assets because stock cannot be guaranteed to sell quickly - it may become obsolete or deteriorate. The formula is:

Interpretation:

- A ratio of at least 1:1 is generally considered acceptable

- A ratio below 1:1 means current assets (excluding stock) do not cover current liabilities, which could indicate potential liquidity problems

- However, as with the current ratio, retailers with strong cash flows may operate comfortably with an acid test ratio below 1:1

- The acid test ratio provides a more conservative view of liquidity than the current ratio

The acid test ratio is sometimes called the "quick ratio" because it only includes assets that can be "quickly" converted to cash. By removing inventories, it tests whether a business could pay its debts immediately if necessary, without relying on selling stock.

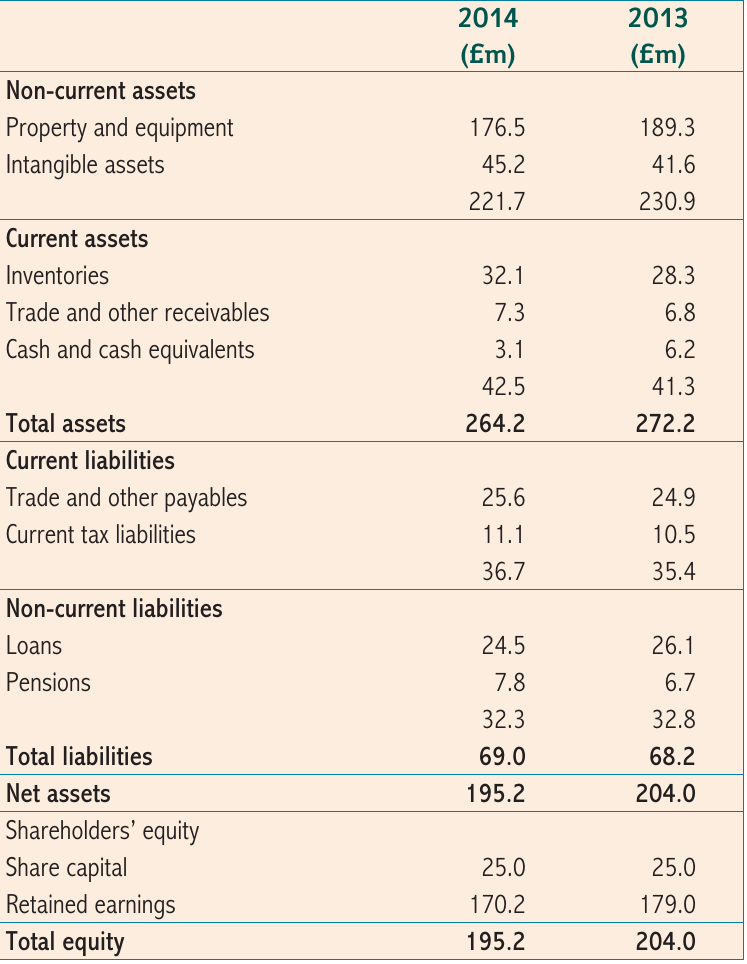

Worked example: Kingham plc

Worked Example: Calculating Liquidity Ratios for Kingham plc

Using the balance sheet data for Kingham plc (a clothing retailer):

Current ratio (2014):

- Current assets: $42.5m

- Current liabilities: $36.7m

Acid test ratio (2014):

- Current assets: $42.5m

- Inventories: $32.1m

- Current liabilities: $36.7m

Analysis: Both ratios appear low - the current ratio is below the ideal 1.5:1 and the acid test ratio is well below 1:1. This suggests Kingham plc may be short of liquid resources. However, as a retailer, the company generates cash quickly from sales, so it may be able to operate successfully with lower ratios than manufacturing businesses.

Working capital

Working capital represents the funds available for day-to-day business operations. It is calculated as:

This formula shows the liquid assets remaining after all short-term debts have been paid.

Why working capital matters

Working capital is essential because:

- It pays for immediate operating expenses (wages, utility bills, raw materials)

- Low working capital can signal financial distress - struggling businesses often show inadequate working capital on their balance sheet

- Insufficient working capital can lead to business failure, even if the company is making profits

- Too much working capital can indicate inefficiency - money tied up in stock or debtors could be used more productively

Critical Warning: Working Capital and Business Failure

Insufficient working capital is one of the leading causes of business failure. A company can be profitable on paper but still fail if it cannot generate enough cash to pay its bills. This is why liquidity analysis is just as important as profitability analysis.

Managing working capital

Effective working capital management involves balancing liquid resources against immediate obligations. Businesses must ensure they have enough cash flow to meet short-term debts while avoiding holding excessive unproductive assets.

Real-World Example: Tyneside Autobuy Ltd

The case of Tyneside Autobuy Ltd demonstrates the dangers of poor working capital management. Despite nearly $23 million in revenue, the company failed due to inadequate working capital caused by poor cost controls and excessive overheads. The business could not raise sufficient funds to continue operations and entered administration.

This illustrates that revenue alone does not guarantee survival - effective working capital management is essential.

Ways to improve liquidity

Businesses can improve their liquidity position through several strategies:

Increasing current assets:

- Negotiating shorter credit terms with customers (reducing receivables)

- Selling excess or slow-moving inventory

- Improving inventory management to reduce stock levels

- Injecting additional capital from owners or shareholders

Reducing current liabilities:

- Negotiating longer credit terms with suppliers

- Paying off short-term loans or reducing overdraft usage

- Converting short-term debt to long-term financing

- Delaying non-essential capital expenditure

Improving cash flow:

- Encouraging cash sales rather than credit sales

- Offering discounts for prompt payment

- Implementing better credit control procedures

- Reducing operating expenses

The most effective approach often involves a combination of these strategies. For example, a business might simultaneously negotiate better payment terms with suppliers (reducing pressure on current liabilities) while improving its debt collection procedures (increasing current assets).

Exam application

When analysing liquidity in exam questions:

- Calculate both ratios - the current ratio and acid test ratio provide different insights

- Compare with industry norms - what is acceptable varies by sector

- Look at trends over time - is liquidity improving or deteriorating?

- Consider the business context - retailers can operate with lower ratios than manufacturers

- Link to consequences - poor liquidity can lead to inability to pay suppliers, loss of supplier relationships, or business failure

- Evaluate using stakeholder perspectives - creditors, investors, and managers all care about liquidity for different reasons

Exam Success Tip:

Always provide context and justification when evaluating liquidity ratios. Don't just state whether a ratio is "good" or "bad" - explain why it matters for that specific business, considering factors like industry norms, business model, and trends over time. Higher marks go to students who demonstrate analytical thinking rather than just mechanical calculation.

Remember!

Key Concepts:

- Liquidity measures a business's ability to meet short-term debts and is essential for survival

- The statement of financial position shows assets, liabilities, and capital at a point in time

- Working capital = Current assets - Current liabilities

Critical Formulas:

(Healthy range: 1.5:1 to 2:1)

(Healthy range: at least 1:1)

Key Distinctions:

- Current assets convert to cash within 12 months; non-current assets are long-term resources

- Current liabilities must be paid within 12 months; non-current liabilities are due after more than one year

- The acid test ratio is stricter than the current ratio because it excludes inventories

Essential Understanding:

- Poor liquidity is a common cause of business failure, even for profitable companies

- Different industries have different acceptable liquidity levels - retailers typically operate with lower ratios

- Both excessive and insufficient liquidity can indicate problems with financial management